Why Haven’t Loan Officers Been Told These Facts?

I have two borrowers on the same application, and one of the borrowers will not work out. Can I delete them from the file, or do I have to decline that borrower even though the other borrower will be approved? Should I decline them both and then create a separate app for the borrower that can be approved?

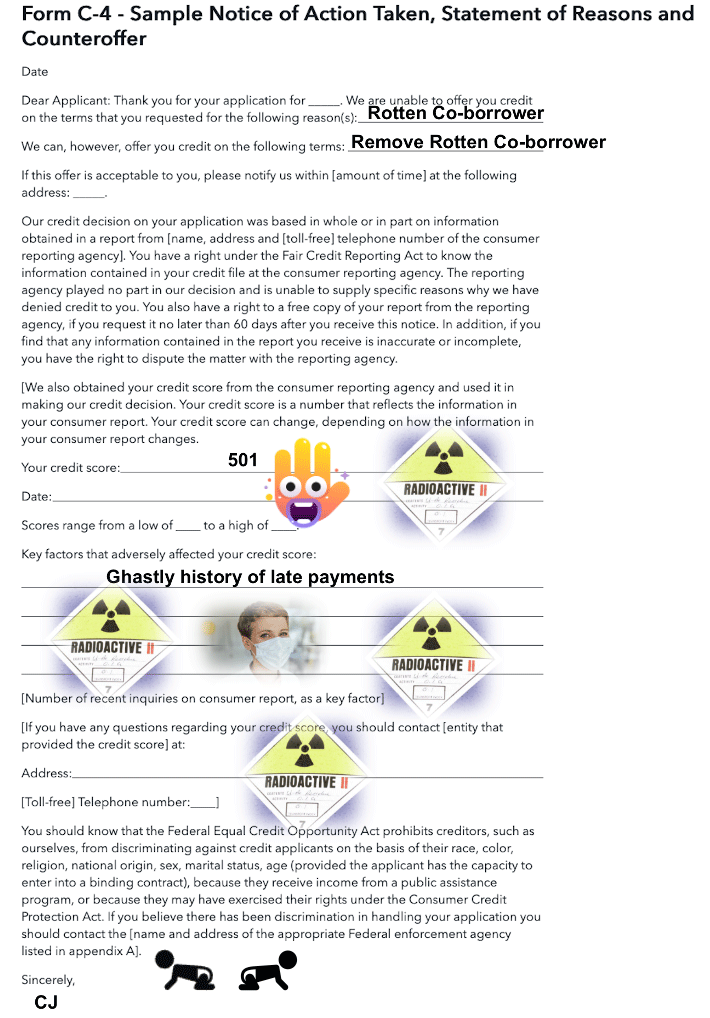

LoanOfficerSchool.com received an inquiry from a 2022 CE customer on the Regulation B Notice requirements. The question involves a common loan manufacture situation.

What the student inquiry describes is an adverse action and proposed counteroffer. A counteroffer combined with an adverse action disclosure might have been her best bet (see the snippet Form C-4 above). Instances such as these are what Congress had in mind when amending ECOA in 1976 to include the Notice requirements.

From the Legislative History of the Equal Credit Opportunity Act Amendments of 1976 – U.S. Code Congressional and Administration News

The requirement that creditors give reasons for adverse action is a strong and necessary adjunct to the antidiscrimination purpose of the legislation, for only if creditors know they must explain their decisions will they effectively be discouraged from discriminatory practices.

Rejected credit applicants will now be able to learn where and how their credit status is deficient and this information should have a pervasive and valuable educational benefit.

Instead of being told only that they do not meet a particular creditor’s standards, consumers particularly should benefit from knowing, for example, that the reason for the denial is their short residence in the area, or their recent change of employment, or their already over-extended financial situation.

Regulation B 12 CFR §1002.9(a)(2)

A notification given to an applicant when adverse action is taken shall be in writing and shall contain a statement of the action taken; the name and address of the creditor; a statement of the provisions of section 701(a) of the Act; the name and address of the Federal agency that administers compliance with respect to the creditor; and either:

(i) A statement of specific reasons for the action taken

OR

(ii) A disclosure of the applicant’s right to a statement of specific reasons within 30 days, if the statement is requested within 60 days of the creditor’s notification

Regulation B addresses the Notice requirements for applications with multiple applicants

Multiple applicants 12 CFR § 1002.9(f)

When an application involves more than one applicant, notification need only be given to one of them but must be given to the primary applicant where one is readily apparent.

Counteroffer combined with adverse action notice. 12 CFR 1002.9 Comment 9(a)(1)-6

A creditor that gives the applicant a combined counteroffer and adverse action notice that complies with § 1002.9(a)(2) need not send a second adverse action notice if the applicant does not accept the counteroffer. A sample of a combined notice is contained in form C-4 of appendix C to the regulation.

Adverse Action 12 CFR § 1002.2(c)

(1) The term means:

(i) A refusal to grant credit in substantially the amount or on substantially the terms requested in an application unless the creditor makes a counteroffer (to grant credit in a different amount or on other terms) and the applicant uses or expressly accepts the credit offered.

Comment 2(c)(2)(v)-1 When an applicant applies for credit and the creditor does not offer the credit terms requested by the applicant (for example, the interest rate, length of maturity, collateral, or amount of down payment), a denial of the application for that reason is adverse action (unless the creditor makes a counteroffer that is accepted by the applicant) and the applicant is entitled to notification under Regulation B.

However, no notice is required when a person applies to a mortgage company for a type of credit that the lender does not offer. For example, an unsecured personal loan is an example of a mortgage lender not offering the type of credit requested. Accordingly, no adverse action notice is required. See 12 CFR § 1002.2(c)(2)(v) Adverse action cited below.

2) Adverse action does not include:

(v) A refusal to extend credit because the creditor does not offer the type of credit or credit plan requested.

Glad we could clear that up for you!

The LOSJ does not provide legal advice. Nor should anything in the LOSJ be construed as a legal opinion on specific facts or circumstances. The contents are intended for general informational purposes only. Readers are encouraged to consult with legal counsel concerning legal matters and specific legal questions.

BEHIND THE SCENES

Appraisal Waivers – Risks and Rewards for Lenders

An appraisal waiver is an offer by Fannie Mae or Freddie Mac to a lender and borrower to forgo the requirement of an appraisal.

Instead of a traditional appraisal report, the GSEs accept a valuation using its automated process that draws from the organization’s appraisal database.

Appraisal waivers are becoming more common. As a result, the share of GSE loans underwritten using an appraisal waiver increased from less than 10% in early 2019 to over 30% by mid-2021.

One factor contributing to the growing use of appraisal waivers in 2020 was the COVID-19 pandemic. During the pandemic, Freddie Mac encouraged appraisal waivers for eligible mortgages to reduce physical contact between parties in the mortgage transaction. Additionally, Freddie Mac expanded its eligibility criteria to align with that of Fannie Mae more closely.

A credit score does not determine eligibility for an appraisal waiver. However, it could be correlated with factors that affect eligibility, such as the LTV ratio. While both GSEs have higher appraisal waiver shares for loans with FICO scores above 750, Freddie Mac has a notably higher share for loans with FICO scores below 750.

Excerpts and paraphrases from FHFA Mortgage Appraisal Waivers Paper

Joshua Bosshardt, William M. Doerner, Fan Xu

FEDERAL HOUSING FINANCE AGENCY

Division of Research and Statistics

Office of Research and Analysis

November 2022

From FNMA

Does every loan delivered to Fannie Mae require an appraisal? What if we have a recent appraisal on file? In some cases, we may be willing to waive the appraisal for certain transactions.

Fannie Mae’s appraisal waiver offers are issued through Desktop Underwriter® (DU®) for eligible transactions using Fannie Mae’s database of more than 31 million appraisal reports in combination with proprietary analytics from Collateral Underwriter® (CU®).

The following message will be displayed in the DU Underwriting Findings report when a loan receives an appraisal waiver offer:

“DU accepts the value submitted as the market value for this subject property. This loan is eligible for delivery to Fannie Mae without an appraisal and is eligible for representation and warranty relief on the value, condition and marketability of the subject property if the appraisal waiver is exercised by the lender at the time of loan delivery by including Special Feature Code 801 and the Casefile ID in the loan delivery file. If the waiver is not exercised, an appraisal based on an interior and exterior property inspection is required for this transaction. If an appraisal is obtained for this transaction, or the Selling Guide states that the transaction is not eligible for an appraisal waiver, the appraisal waiver may not be exercised, and the loan cannot be delivered with Special Feature Code 801. Note that DU is not able to identify all transactions that are ineligible for an appraisal waiver, including community land trusts or properties with resale restrictions, and Texas Section 50(a)(6) mortgages.”

Q1. How do lenders get access to appraisal waivers?

A1. Appraisal waivers are available to all lenders who use DU, including through the Desktop Originator® (DO®) interface. No registration is needed.

Q2. Are appraisal waivers available to correspondent lenders?

A2. Yes. A correspondent lender may receive an appraisal waiver offer when submitting a loan casefile to DU. Correspondent lenders should contact their aggregators to discuss aggregator interest in delivering loans with an appraisal waiver to Fannie Mae and to ensure the correspondent is obtaining the appropriate fieldwork to meet aggregator guidelines.

Q3. What are the eligibility requirements for appraisal waiver consideration? The appraisal waiver offer will be considered on the transactions below:

A3. Loan casefiles that receive an Approve/Eligible recommendation ▪ One-unit properties,including condominiums

Limited cash-out refinance transactions:

– Principal residences and second homes up to 90% LTV/CLTV

– Investment properties up to 75% LTV/CLTV

Cash-out refinance transactions:

– Principal residences up to 70% LTV/CLTV

– Second homes and investment properties up to 60% LTV/CLTV

Purchase transactions

– Principal residences and second homes up to 80% LTV/CLTV

Q5. Are there prior appraisal requirements for an appraisal waiver to be considered?

A5. For an appraisal waiver to be considered, generally a prior appraisal must be found for the subject property in Fannie Mae’s Collateral Underwriter (CU) data. When required, DU will compare the address for the subject property to the property addresses found in CU. When a property address match is found, DU will use the information from the prior appraisal to determine if the loan casefile is eligible for the appraisal waiver. In some cases, the prior appraisal may not be acceptable. For example, if a CU Overvaluation Flag was issued on the prior appraisal or the appraisal could not be scored, that prior appraisal will not be used, and an appraisal waiver will not be offered on the new loan casefile.

Q7. Are appraisal waivers offered on loan casefiles underwritten through Preliminary Findings?

A7. Yes. When the appraisal waiver offer was enhanced in December 2016, Desktop Originator® (DO®) users would only see the offer on loan casefiles underwritten using a sponsoring lender. Effective with DU Version 10.1, DO loan casefiles underwritten through Preliminary Findings are eligible for the appraisal waiver offer.

What are some of the risks?

The appraisal waiver is the best deal since sliced bread when it works. There is little downside to using the waiver. However, AUs may fail to recognize ineligible transactions and still offer a waiver. Double-check the selling guide for the authoritative waiver requirements and identify eligible and ineligible transactions. Additionally, FNMA waivers come with numerous provisos – know them well.

Q11. If a lender receives an appraisal waiver offer on a loan casefile, are there situations in which the lender would still need to obtain an appraisal?

A11. Yes. There may be certain situations in which a lender needs to obtain an appraisal, even though an appraisal waiver was offered on the loan casefile.

-

- The lender has reason to believe that fieldwork is warranted because the sales contract for a purchase transaction stipulates repairs that are not minor, or that may affect the safety, soundness, or structural integrity of the property.

- The mortgage insurance provider requires an appraisal.

- NOTE: The borrower always has the choice to request an appraisal.

Q14. What should the lender do if a disaster is declared after the loan closes with an appraisal waiver but before the loan has been delivered to Fannie Mae?

A14. The lender makes property-related representations and warranties as of the time it delivers the loan to Fannie Mae. Before delivery of a mortgage loan to Fannie Mae when the property may have been damaged by a disaster, the lender is expected to take prudent and reasonable actions to determine whether the condition of the property may have materially changed. The lender is responsible for determining if an inspection of the property and/or new appraisal is necessary to support its representations.

Q15. What qualifies as “taking prudent and reasonable actions” when a lender needs to determine if a property has been damaged by a disaster? Is an inspection required?

A15. Fannie Mae is not prescriptive as to what method the lender must use to determine the condition of the property. The lender must do whatever it deems necessary to be confident in warranting the condition of the property, and this will vary by circumstance.

Q19. If a lender obtains an appraisal and also receives an appraisal waiver offer from DU, may the lender exercise the appraisal waiver?

A19. No. When a lender obtains an appraisal and also receives an appraisal waiver offer, the appraisal waiver may not be exercised, and the loan cannot be delivered with SFC 801.

Q22. When an appraisal waiver offer is exercised, is the lender responsible for the standard representations and warranties regarding the value of the property?

A22. Fannie Mae accepts the value estimate submitted by the lender as the market value for the subject property when an appraisal waiver offer is exercised. The lender is relieved from Fannie Mae’s enforcement of representations and warranties regarding the value, condition, and marketability of the property. The lender is required to represent and warrant that the data submitted (other than the value estimate) to DU is complete and accurate.

When exercising an appraisal waiver offer, the lender is required to include the casefile ID and SFC 801 in the loan delivery file to Fannie Mae to receive the applicable representation and warranty relief.

Q23. For properties secured by condos that receive an appraisal waiver offer, do lenders get any relief from project review requirements?

A23. No. All project standards still apply. Lenders are responsible for determining the documentation they need to review to determine that the project meets the requirements for the project review being completed.

Additionally, relying exclusively on the appraisal for any review type is not recommended because not all project eligibility requirements are addressed in the appraisal.

See the Entire FNMA Appraisal Waiver FAQ here: FNMA Appraisal Waiver FAQ

Helpful FNMA Factsheet here: FNMA Appraisal Waiver Fact Sheet

Tip of the Week – Rehumanize Yourself

I work all day at the factory

I’m building a machine that’s not for me

There must be a reason that I can’t see

You’ve got to humanize yourself

-Sting/Stewart Copeland

Asking the right questions at the right time is critical to sound loan origination. For example, one standard question from the URLA is about the applicant’s home-buying or mortgage experiences.

Too often, MLOs often ask this critical question about homeownership and settle for a meager yes or no answer. The MLO needs to continue past the yes and no homeownership answer to effectively lead the transaction.

It is easy to get lost in the interest rate, down payment, or monthly payment, losing sight of the whole person that is the prospect before you—instead, humanize the interaction. People may appear outwardly as though their lack of buy-in is a matter of facts, costs, or some other pragmatic and logical concern. But inside, they are full of emotions that influence their thinking and comprehension of what is said.

The homeownership question can elicit essential information beyond eligibility for first-time home buyer programs. For applicants with a mortgage history, both the MLO and the customer will profit by understanding the applicant’s feelings surrounding past mortgage experiences.

The prospect’s recollections about their mortgage or home-buying experience can provide a wealth of information on the prospect’s expectations and how to manage those expectations. That is leadership, and you must bring it to every loan manufacture. For those prospects with mortgage experience, the question is a grand opportunity for the MLO to ask about their mortgage and home-buying expectations. For example, “Mr. Borrower, could I address some of your concerns about getting a loan? Please tell me, what are a few of your concerns about buying a home or getting a mortgage? Do you have a top three?”

For those prospects without mortgage experience, the question is a grand opportunity for the MLO to ask about their mortgage and home-buying expectations. For example, “Mr. Borrower, could I address some of your concerns about getting a loan? Please tell me, what are a few of your concerns about buying a home or getting a mortgage? Do you have a top three?”

The prism of experience shapes the applicant’s perceptions, likes, and dislikes. Therefore, when building rapport with the prospect, it is good to find out how they feel about any past mortgage and home-buying experiences. This line of questioning also demonstrates a sincere interest in the prospect as a person. Consequently, most prospects will perceive your sincere interest in them as a sign of concern and respect.

The prospect’s cognition and logic process through their emotional prism. This prism can be good or bad for your loan presentation. Be mindful that emotions are contagious—the prospect’s emotions impact you, and your emotions impact theirs.

In the office, always have bottled water on hand. Don’t ask if the prospect would like something to drink. Give them the water, then ask if you can get them a soda or coffee. A simple act of kindness can help melt a frosty heart.

When building rapport over the phone, right up front, ask them if you might send them the “How to Evaluate Your Mortgage Options” brochure or some similar handout. Again, the concept is for you to give them something that might soften their heart towards you and your efforts.

If you are unfamiliar with the power of reciprocity, check out the classic book “Influence – The Psychology of Persuasion” by Robert Cialdini. In the book, he references a well-known experiment by psychologist and Cornell Professor Dennis Regan. See the video link below for the cliff notes version.

What to do when the prospect sounds negative or appears to be having a rough time? First, stop presenting the damn loans! Instead, start focusing on their state of mind. Sometimes, your positive outlook and encouragement can positively shape the conversation. For example, a kind word or demonstration of empathy can help people change emotional gears.

Therefore, if they appear uncooperative or closed off, it might be productive to acknowledge their emotional state. For example, “Mr. Stakeholder, buying a home can be stressful. I get it. Would you rather talk about this at another time? Can I schedule some time that is better for you?” By demonstrating your awareness of the stakeholder’s discomfort, they will often try to change gears and become more open to your encouragement and positive emotions. Furthermore, your expressions of concern and kindness may psychologically obligate the prospect to reciprocate with you.

Generally, people need and want love and acceptance. Showing respect and empathy go a long way in putting stakeholders at ease and in a better place to cooperate with your efforts.