Why Haven’t Loan Officers Been Told These Facts?

Assessing the Impacts of the GSEs’ New Credit Score Policy

From FNMA Selling Guide Announcement SEL-2025-09

- Minimum credit score requirements will no longer apply to loans submitted to DU.

- The Selling Guide has been updated to align with changes previously communicated in the DU Version 12.0 November Update Release Notes.

- Specifically, DU will no longer apply a minimum credit score but will rely on its own comprehensive analysis of risk factors to determine eligibility.

- In addition to these revisions, we have updated DU nontraditional credit documentation and homebuyer education requirements to no longer rely on credit scores.

- Instead, DU will issue a message when lenders must establish a nontraditional credit history and/or complete homebuyer education when no borrower has at least one credit account or installment account reported on their credit report.

- Effective: The minimum representative credit score requirement of 620 for loan casefiles for one borrower and minimum average median credit score requirement of 620 for more than one borrower will be removed for new loan casefiles created on or after Nov. 16, 2025.

- All other changes apply to loan casefiles submitted or resubmitted on or after the weekend of Nov. 15, 2025.

What About Pricing?

The government-sponsored enterprises (GSEs) now accept loans in the Automated Underwriting System (AUS) without needing credit scores. That’s a positive development. You might ask, without credit scores, how are loan-level pricing adjustments for credit scores calculated? According to the latest documentation (LLPA Matrix), the lowest credit score tier must be used when determining the loan’s pricing. That makes for some expensive pricing. Consequently, submitting loans sans credit score to the AUS may not be the first order of business for transactions without LLPA relief.

From the Fannie Mae Loan-Level Price Adjustment Matrix (LLPA © 2024)

- Loans delivered without any credit score will be charged under the lowest credit score range shown in each of the applicable LLPA tables.

- Loans delivered with more than one borrower, when one borrower has a credit score and one or more borrowers do not have credit scores, are charged according to the representative credit score (disregarding the borrower(s) without a credit score).

For Transactions Subject to the LLPA/Credit Fee Waiver, BINGO! That’s a fine fit.

Duty-to-serve transactions and first-time buyers under the Area Median Income (AMI) guidelines may significantly benefit from this initiative.

Taking Advantage of the Minimum Credit Score Change

With FNMA and FHLMC eliminating minimum credit score requirements for loans processed through automated underwriting systems, it is essential to consider the potential impacts, both positive and negative. First, identify the transactions that are immediately enhanced with the change. That would include those applicants without viable scores who will not pay credit fees or LLPAs.

With the recent developments in credit scoring and AUSs, alternative credit has become more critical than ever. Among the various non-traditional credit factors (also known as alternative data), rental history is the most influential factor. With the GSEs (Government-Sponsored Enterprises) removal of the minimum credit score requirement, the agencies are increasing their reliance on AI and the Automated Underwriting System’s (AUS) ability to identify risk.

Given this context, reviewing the risk factors that the AUS assesses may be beneficial to originators (See the hyperlink at the end of the article). Importantly, these systems now have access to a wealth of data for artificial intelligence (AI) modeling. In particular, the agency’s incorporation of trended data in its AUS is noteworthy. FNMA (Fannie Mae) has been utilizing trended data analysis in Desktop Underwriter (DU) since 2016, while FHLMC (Freddie Mac) adopted this same approach in 2024.

Nothing has changed regarding manual underwriting. The minimum credit score requirements for manual underwriting still vary based on the type of transaction. However, loans that go through electronic underwriting have a better chance of approval, especially for applications that might be marginal but are well-processed. While only a few select stakeholders fully understand how these underwriting algorithms function, specific patterns are detectable.

The Best Credit Benchmark For Homebuyers

Years ago, before automated underwriting became widely used and the industry relied so heavily on credit scores, rent ratings were the primary benchmark used in the absence of a strong credit history. Now, after more than 30 years of credit scores and algorithmic underwriting, we are witnessing a resurgence of the rent rating as a key credit benchmark for marginal applications.

This is important because if the loan is referred or otherwise ineligible for AUS, lenders must rely on manual underwriting, which is increasingly risky. The priority is to process the loan so that AUS can render the approval. Consequently, for thin-file credit score or AUS issues or otherwise marginal applicants, a scoreable rent rating is a must to keep the loan in the AUS. For many transactions, the rent rating is the difference between ‘approval/accept’ and ‘refer’.

For proactive lenders who can leverage rent ratings in AUS by effectively utilizing asset verification reports (AVR) in the loan process, there is an opportunity to close loans that other lenders, who do not use AVRs, cannot.

A Golden Opportunity

Market segmentation offers significant advantages when utilizing market trends to design effective campaigns. Refer to the FNMA case study link at the end of this article for more insights. Technology, not just consumer need, is a key driver of developing market segments.

Lenders who identify specific market segments to target through technology are better positioned to capitalize on industry shifts and establish a presence in underserved markets.

Predictive Power Improves Products and Pricing

Analyzing trended data alongside traditional tradelines enhances predictive power more than conventional FICO® models. Utilizing these data improvements with AI capabilities positions the industry to discover new opportunities for innovative originators. For marginal applications that were previously assigned to manual underwriting because of thin-file issues, the future looks promising, especially for moderate-income households.

Look for more details in next week’s LOSJ regarding market segments associated with alternative data solutions.

From FNMA, Rent Payment History

For certain loan casefiles, DU can consider a borrower’s rent payment history identified on a 12-month third-party asset verification report or a credit report. When DU logic can identify rent payments in the asset verification report or credit report, it will use the rent payment history to positively supplement the credit risk assessment.

The following requirements apply when using rent payment history in DU:

- At least one borrower must have been renting for at least 12 months with a monthly rent payment of $300 or more and one of the following:

- Have no mortgage reported on their credit report,

- Have a limited credit history, or

- Have no credit score.

- When the rent payment history does not appear on the credit report, for DU to be able to identify rent payments using an asset verification report, the lender must:

- Enter the monthly rent paid by the borrower in the online loan application,

- Obtain an asset verification report with 12 months of bank statement data through an authorized DU validation service asset verification report vendor, and

- Confirm the borrower is an account holder and that the account provided in the asset verification report is the one from which the borrower pays rent.

At the time of loan origination, the originating lender must have access to the full asset verification report containing the data covering the period of time provided to DU for assessment.

When an asset verification report is used for both rent history and asset documentation, including asset validation through the DU validation service, only the most recent 60 days of account activity must be reviewed in accordance with the requirements in B3-4.2-02, Depository Accounts and B3-2-02, DU Validation Service, and retained in the loan file.

Understanding Risk Factors in DU

LLPA Lender Letter (LL-2022-05)

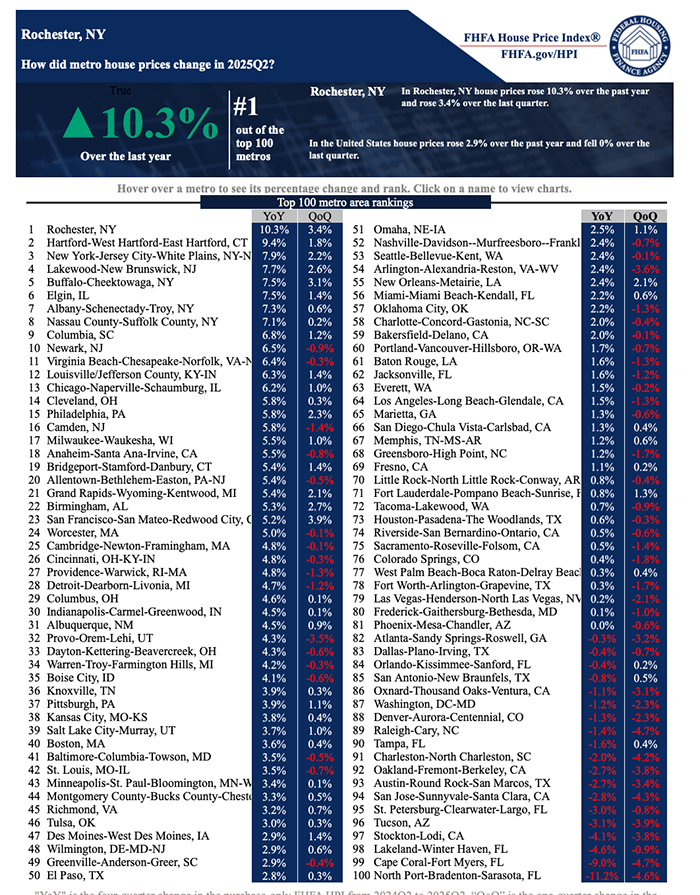

BEHIND THE SCENES: Market Analysts Seeing Red

All Real Estate is Local

The maxim that all real estate is local is valid until it is not. Real estate trends that originate as local manifestations often tend to migrate or spread into other markets. The health of the job and stock markets are a topic of hot debate these days. Some widely used labor benchmarks are outdated and misleading, which could exacerbate the shock that occurs when these indicators catch up with reality.

Something Brewing

Recent reports suggest that the job market is not as robust as the unemployment numbers alone might suggest. Challenger, Gray & Christmas reported over 153,000 job cuts announced in October, the worst for that month since 2003. The firm cited cost-cutting, AI adoption, and pandemic-era overhiring as major reasons behind the spike.

Companies have announced over 1.1 million layoffs this year, representing a 44% increase compared to the total number of layoffs in 2024. The tech and retail sectors have been the most severely affected, with significant job cuts announced by companies such as Amazon, Target, and UPS.

These reports indicate that the job market is stable but far less dynamic than it was a year ago. Workers are tending to stay in their positions, companies are being cautious, and overall confidence in the economy is quietly declining. Which means a shift from purchase money to refinancing is in store. The realization that the job market is more challenging than previously thought, coupled with another shock, such as a steep sell-off on the stock market, may mark the beginning of a new economic era.

Recent Comments from Fed Governor and FFIEC Chair Michelle W. Bowman

“Declines in housing activity, including single-family home construction and sales, have been accompanied by higher inventories of homes for sale and falling house prices, suggesting that housing demand has also weakened. Elevated mortgage rates may be exerting a more persistent drag as income growth expectations have declined while house prices remain high relative to rents. Given very low housing affordability, existing home sales have remained depressed since 2023 and at levels only comparable with the early 2010s following the financial crisis. I am concerned that, in the current environment, declines in house prices could accelerate, posing downside risks to housing valuations, construction, and inflation.”

Board Of Governors, Federal Reserve System

Vice Chair for Supervision, Michelle W. Bowman

2025 Kentucky Bankers Association Annual Convention, Asheville, North Carolina

Tip of the Week – Sign Up for 2025 CE

Expanding your product offerings is an effective way to enhance your business’s vitality. This year, the Loan Officer School is surveying non-government financing options for construction and renovation projects.

The shortage of affordable housing is unlikely to be resolved anytime soon. As affordable, move-in-ready housing solutions remain hard to find, the demand for construction and renovation loans is expected to increase. According to the JCHS, Harvard University, the US remodeling market soared above $600 billion in the wake of the pandemic and, despite recent softening, remains 50 percent above pre-pandemic levels.

Discover how to enhance borrower advantages through construction and renovation financing.

- Enhanced housing affordability.

- Housing options for aging or disabled borrowers.

- Housing solutions for borrowers caring for aging or disabled family members.

- Multi-generational housing solutions.

For any questions or inquiries regarding state education needs, please feel free to call.

Call Us Today! (866) 314-7586

Online self-study classes are available.

Sign up for 2025 Online self-study CE