Gerald R. Ford, 38th President of the United States: 1974 ‐ 1977 President Ford signed the Equal Credit Opportunity Act Amendments, including ECOA Notice requirements, into law on March 23, 1976. Second from the right, a young Joe Biden? (Courtesy of the Gerald R. Ford Presidential Library)

Why Haven’t Loan Officers Been Told These Facts?

Application Informality: A Too Common Mistake

March 23, 1976

Presidential Statement on Signing the ECOA Amendments of 1976

“I HAVE today signed H.R. 6516, which expands the scope of the Equal Credit Opportunity Act.

This administration is committed to the goal of equal opportunity in all aspects of our society. In financial transactions, no person should be denied an equal opportunity to obtain credit for reasons unrelated to his or her creditworthiness.

Last November, I stated my support for legislation to amend the Equal Credit Opportunity Act to bar creditor discrimination on the basis of race, color, religion, or national origin against any credit applicant in any aspect of a credit transaction. The act currently prohibits discrimination on the basis of sex or marital status.

This bill carries out my recommendations. It applies to business as well as consumer credit transactions and, thus, reaches discrimination against Americans in the extension of credit which might arise from foreign boycott practices.

In addition, this bill permits the Attorney General, as well as private citizens, to initiate suits where discrimination in credit transactions has occurred. It also provides that a person to whom credit is denied is entitled to know of the reasons for the denial.

It is with great pleasure that I sign a bill that represents a major step forward in assuring equal opportunity in our country.”

– President Gerald R. Ford

A Word From Congress

The requirement that creditors give reasons for adverse action is … a strong and necessary adjunct to the antidiscrimination purpose of the legislation, for only if creditors know they must explain their decisions will they effectively be discouraged from discriminatory practices. Rejected credit applicants will now be able to learn where and how their credit status is deficient, and this information should have a pervasive and valuable educational benefit. Instead of being told only that they do not meet a particular creditor’s standards, consumers should particularly benefit from knowing, for example, that the reason for the denial is their short residence in the area, or their recent change of employment, or their already over-extended financial situation.

– Legislative History of Equal Credit Opportunity Act Amendments of 1976

Regulation B Compliance Issues

As the federal government pursues aggressive deregulatory efforts, it is critical to highlight that state regulators are able and willing to take a more active enforcement role. Of particular interest this year is ensuring compliance with Regulation B notice requirements. Additionally, stakeholders must appreciate that both the Equal Credit Opportunity Act (ECOA) and the Fair Housing Act (FHA) permit state enforcement and private action (private persons), including class action lawsuits.

The Multistate Mortgage Committee (MMC) is a representative body of state mortgage regulators, appointed by the Conference of State Bank Supervisors (owners of the NMLS) and the

American Association of Residential Mortgage Regulators, to represent the examination interests of the combined states (all 50 plus the territories) under the Nationwide Cooperative Protocol and Agreement for Mortgage Supervision. The MMC’s primary focus is on nationwide lenders operating in 10 or more states. However, the MMC supervisory expertise and data are shared across the membership. Meaning every state agency with mortgage supervision responsibility is well aware of noncompliance patterns detected by the MMC.

In recent years, the MMC has identified a prevalent pattern of noncompliance with Regulation B Notice practices among state-supervised mortgage businesses, to the extent that this issue is the most frequently observed violation on MMC examination. One reason specific noncompliance issues become the “most frequently observed” is “examination focus.” Examiners know where to look for violations.

It’s important to note that while federal law enforcement has moved away from using the legal theory of disparate impact to establish harms or violations of the ECOA and FHA, this shift in federal policy does not affect the federal courts or the ability of states or private individuals (including those pursuing class action lawsuits) to successfully prosecute claims based on disparate impact.

When a lender is unaware of Regulation B-governed actions within its organization (e.g., unreported or unknown adverse actions or informal applications), the consequences can be severe.

Internal Supervision: A Defense Against Harmful Business Practices, Including Noncompliance

Application detection and visibility serve as a critical checkpoint in the loan manufacturing process, indicating when an application has been initiated or is about to be initiated. Part of the problem is the lack of application supervision, as management often has little visibility into loan officer-consumer interactions. Originators habitually allow for perpetual weak links in compliance, not to mention customer and prospect acquisition and retention. In other words, management is overly dependent on loan officers’ voluntary compliance with policy, leaving the business vulnerable to non-compliant practices.

While there is no single solution to eliminate the threat of informal applications and unknown adverse action, several mitigations are not overly difficult to implement. Instead of a single solution, implementing a series of mitigations, including training, workflow structure, technology, and audit, will allow the originator to better manage application supervision.

Twofer Violation

The credit pull is one of the key points in the workflow that provides application visibility. While pulling credit does not guarantee that an application has been submitted, it does indicate a strong likelihood that an application, or something that could be construed as an application, has occurred or soon will. It’s important to remember that any unsupervised application poses significant business risks, including noncompliance.

Keep in mind that if the loan officer informs the prospect that they will not qualify based on information from a credit report, an application, as that term is defined by Regulation B, has occurred, and a Notice of adverse action is required. Furthermore, for a consumer transaction, under the Fair Credit Reporting Act (Regulation V), an adverse action with regard to credit transactions, the term “adverse action” has the same meaning as used in Section 701(d)(6) [15 U.S.C. 1691(d)(6)] of the Equal Credit Opportunity Act (ECOA), Regulation B, and the official CFPB staff commentary. Therefore, if the loan officer reviews the consumer’s credit report and states that the prospect will not qualify, in part, due to information contained in the credit report, the Originator must also meet the FCRA disclosure requirements. Simply put, if the originator pulls credit and the response is an adverse action under Regulation B, it is an adverse action under Regulation V.

Violating the Fair Credit Reporting Act (FCRA) can result in serious penalties. It’s important to diligently avoid any patterns of violations under the ECOA and the FCRA. Regarding the Home Mortgage Disclosure Act (HMDA), it’s crucial to know what actions qualify as loan originations under HMDA. For some third-party originators, the first consideration is whether you have a reporting obligation. If you do, it’s essential to know what data needs to be reported and when.

We’ll address the HMDA implications in more detail in another article.

Regulation C, 12 CFR § 1003.4(a) A financial institution shall collect data regarding applications for covered loans that it receives, covered loans that it originates . . . § 1003.2(g)(2) Nondepository financial institution means a for-profit mortgage-lending institution (other than a bank, savings association, or credit union) that on the preceding December 31, had a home or branch office in an MSA; and in each of the two preceding calendar years, originated at least 25 closed-end mortgage loans that are not excluded from this part.

Wasting Money and Reputation

Secondly, when considering adverse action, it is advisable to seek a second opinion. This recommendation is particularly pertinent given the varying levels of expertise that exist among loan officers. Many loan officers take pride in their ability to successfully close loans that other lenders have denied. In fact, this achievement is often regarded as a significant accomplishment, as it often paves the way for loan officers to forge profitable relationships with builders, leading real estate agents, and financial planners.

In certain situations, loan approval may depend on the lender’s risk tolerance. However, based on my experience, unnecessary adverse actions—whether formal or informal—usually arise from a lack of diligence, experience, or competence. Individually and or collectively. But more often individual incompetence or sloth. It is essential for mortgage professionals to maintain a high standard of diligence and expertise to mitigate such issues. Besides, even the most competent loan officers can make mistakes.

Where to Start: Esprit de corps

“Esprit de corps” refers to the shared spirit among a group working towards a common vision of success. This concept requires a top-down approach. Leadership must commit to loan officers’ success, while loan officers must dedicate themselves to the organization’s success.

Management plays a crucial role in building this positive esprit by providing support and encouragement to loan officers. Since navigating challenging transactions can be taxing, it is essential for loan officers to feel confident in their ability to address uncertainties and challenges. They should feel comfortable escalating issues to leverage the organization’s collective knowledge and strengths when necessary. This approach not only strengthens compliance practices but also reduces unnecessary loan denials. It’s also far less stressful for the loan officer. The loan officer’s poise under pressure is a collective effort.

The best loan officers are shameless about leveraging the organization to achieve excellence and positive outcomes. Management should also be rightfully shameless in demanding excellence from loan officers. Excellence demands support, including development. Consequently, mistakes must be viewed as learning opportunities, and loan officers and support staff must be confident that it is not only safe to escalate but also what management expects them to do.

Everyone, from the rookie loan officer to the top producer, must have confidence in the organization’s commitment to their success. This shared identity and dedication to excellence must influence everything, from training to workflows to routine interactions. Be the “Three Musketeers” of loan origination: one for all and all for one. An organization, regardless of size, that is committed to excellence, professionalism, and stakeholder satisfaction through a consistently supportive environment will also improve its recruitment and retention effects.

How Might It Work

Before declining a prospect, take the time to thoroughly review the transaction with the originating loan officer and develop options. There is nothing like on-the-job training with an excellent mentor. Seeking a second opinion is beneficial to the originator and the loan officer alike. A confident loan officer should not hesitate to make time when confronted with questions they cannot immediately answer. No off-the-cuff response. Instead, they leverage their resources, take time to gather the right information, check with the right people, and provide the right response. Why choose any other approach?

When a mortgage loan originator (MLO) faces a challenge, they must know in advance what to do. That may be a process, such as guidance from a designated MLO or the branch manager. For instance, the challenged MLO might say, ” Mr. Prospect, I’ll be looking into your options and discussing them with my associates to find the best solution for you. Would it be alright if I touch base with you by the end of the day?” No shooting from the lip.

Few things can damage your reputation and weaken relationships more than having your loan officer turn down an application, only for a competitor to successfully close the deal.

One scenario that could be worse is when law enforcement becomes involved in a transaction due to a complaint under the ECOA or FHA, and the lender is unaware of the applicant or the specifics of the transaction.

Learn more about Regulation B and the notice requirements:

LOSJ V6 I2 Reg B Notice/Diligence/NOI

LOSJ V5 I37 Reg B Notice/Preapproval/FCRA Disclosure

LOSJ V5 I36 Reg B Application Defined, Compared

LOSJ V5 I22 Reg B/Reg Z Understanding the Regs

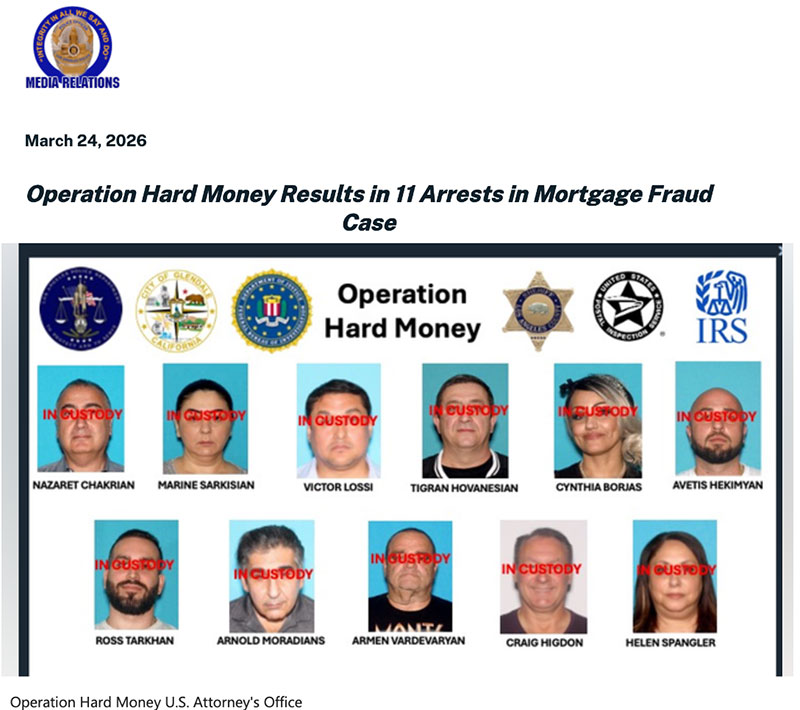

BEHIND THE SCENES: OPERATION HARD MONEY

LAPD, Glendale PD, and Federal Agents Arrest 11 on Charges They Used Stolen Identities to Fraudulently Obtain Loans Backed by Residential Properties

Los Angeles: On Thursday, March 19, 2026, the Los Angeles Police Department’s Commercial Crimes Division – Real Estate Fraud Unit, in partnership with the Eurasian Organized Crime Task Force—which includes agents from the Federal Bureau of Investigation, Internal Revenue Service Criminal Investigations, and Glendale Police Department—carried out Operation Hard Money, leading to the arrest of 11 suspects involved in a complex mortgage fraud scheme.

From the U.S. Department of Justice

Federal Government Seeks Hard Time for Operation Hard Money Defendants

Eleven defendants – including two foreign nationals – were arrested today on a 15-count federal indictment charging them with executing a scheme in which they stole the identities of elderly victims, used that information to obtain title reports for residential properties, then solicited millions of dollars in hard money loans from private lenders by falsely representing the loans as being secured by the elderly victims’ properties.

The following defendants were arrested this morning and all but two of them are expected to be arraigned this afternoon in United States District Court in downtown Los Angeles:

- Nazaret Chakrian, 65, a.k.a. “Niko,” of Hollywood;

- Arnold Moradians, 57, a.k.a. “Julian,” of Hollywood, an Iranian national who has an outstanding warrant for removal from the United States;

- Avetis Hekimyan, 38, a.k.a. “Chef Avo,” of North Hollywood;

- Ross Tarkhan, 32, of Glendale;

- Tigran Hovanesian, 56, of Glendale;

- Armen Vardevaryan, 55, a.k.a. “Gonch,” of North Hollywood;

- Craig Higdon, 66, of Naples, Florida, who will make his initial appearance in the Middle District of Florida;

- Helen Spangler, 62, of Oakdale, California, who will make her initial appearance in the Eastern District of California;

- Victor Lossi, 43, of Thousand Oaks; and

- Marine Sarkisian, 49, of Hollywood, an Azerbaijani national and green card holder.

The following defendant arrested today is expected to be arraigned tomorrow in Los Angeles federal court:

- Cynthia Borjas, 51, of Koreatown.

All defendants except Hovanesian are charged with one count of conspiracy to commit wire fraud and seven counts of wire fraud. Chakrian, Moradians, Borjas, Hekimyan, Tarkhan, Spangler, Lossi, and Sarkisian are charged with one count of aggravated identity theft. Chakrian, Moradians, Tarkhan, and Hovanesian are charged with one count of conspiracy to commit money laundering. Tarkhan is further charged with five counts of money laundering.

“There is no shortage of massive fraud occurring within California,” said First Assistant United States Attorney Bill Essayli. “Today’s operation represents one of many sophisticated schemes used by criminals – including foreign nationals – to defraud U.S. citizens and taxpayers of their hard-earned property. Those days are over under this U.S. Department of Justice. These defendants will be facing significant prison time for their charged conduct.”

“The growing problem of title fraud victimizes homeowners and lenders, many of whom are elderly and have their identities stolen, in addition to their hard-earned money,” said Akil Davis, the Assistant Director in Charge of the FBI’s Los Angeles Field Office. “An investigation by the FBI Eurasian Organized Crime Task Force, LAPD, and other law enforcement partners led to today’s arrests of multiple perpetrators of this cruel scheme who now face lengthy prison sentences.”

“The defendants didn’t just steal identities, they used those stolen identities to secure high value real estate loans, fabricate financial documents, and move millions of dollars through a maze of fraudulent businesses and funnel accounts,” said Tyler Hatcher, Special Agent in Charge, IRS-CI Los Angeles Field Office. “Our agents traced every wire, every transfer, and every shell account to expose the financial backbone of this conspiracy. This indictment sends a clear message, IRS CI will dismantle the money pipelines that allow complex fraud schemes to flourish, and we will hold accountable those who profit from exploiting our financial system.”

According to the indictment that a federal grand jury returned on February 5, from January 2021 to May 2023, Chakrian and Moradians fraudulently obtained the personal identifying information (PII) of elderly victims. The victims owned properties in Santa Monica and in the following Los Angeles neighborhoods: Hollywood, Hollywood Hills, Westwood, and Chinatown.

Chakrian and Higdon then used the victims’ PII to create counterfeit identification documents. Borjas and Hekimyan created email accounts in the victims’ names to impersonate them.

Using the victims’ PII, the fraudulent ID documents, and the fraudulent email addresses, Chakrian, Moradians, Hekimyan, Vardevaryan, and Spangler misrepresented themselves as the victims’ agents, brokers, representatives or relatives, and submitted fraudulent applications to private money lenders for hard money loans secured by the victims’ properties.

Chakrian, Hekimyan, Higdon, and Spangler created false and fabricated documents – including bank statements, rental agreements, doctors’ notes, and death certificates – to the lenders. These documents contained lies about the victims’ identities, assets, finances, and health as well as the loan proceeds’ intended purpose, and the types of properties being used to secure the loans.

Upon receiving closing documents from the lenders, Chakrian, Hekimyan, Lossi, and Sarkisian caused the documents to be fraudulently notarized and signed by individuals representing the victims.

Tarkhan used stolen PII to create synthetic identities – profiles or ID documents combining fictitious profile information with real victim PII. Using these synthetic identities, Tarkhan caused bank accounts to be opened under false names. These accounts were used to funnel proceeds derived from the scheme.

Private money lenders relied on the false statements, misrepresentations, and certifications to cause funds to be disbursed via check and wire to mailboxes and bank accounts controlled by Chakrian, Tarkhan, and others.

The total intended loss in this case is approximately $17.4 million, and the total actual loss is approximately $6 million.

“This case reflects the relentless work of our investigators and the strong collaboration with our federal partners to unravel a complex and calculated criminal scheme,” said Interim Glendale Police Chief Robert William. “Their focus and determination ensured those responsible are held accountable and that justice is delivered.”

An indictment contains allegations that a defendant has committed a crime. Every defendant is presumed to be innocent until and unless proven guilty in court.

If convicted, the defendants would face a statutory maximum sentence of 20 years in federal prison for each fraud- and money laundering-related count, and a mandatory consecutive sentence of two years in federal prison for the aggravated identity theft count.

This case is being investigated by the Eurasian Organized Crime Task Force (EOCTF) and the Los Angeles Police Department – Commercial Crimes Division. The EOCTF includes agents and task force officers from the FBI, IRS Criminal Investigation, the United States Postal Inspection Service, the Los Angeles County Sheriff’s Department, and the Glendale Police Department.

Assistant United States Attorneys Claire E. Kelly of the General Crimes Section and Hava Mirell of the Criminal Appeals Section are prosecuting this case.

Tip of the Week – Have a Question About Operations, Sales, Marketing, or Compliance? Email Your Questions to the Loan Officer School Journal.

We invite LOSJ readers to submit questions on any topic to the editor. Topics can include compliance, sales, marketing, implementation, and other areas that may be helpful to our customers. If we use your question, we will include only your first name in our response. Please send your questions to: losjmailbag@gmail.com.

Necessary Mailbag Disclosure: The LOSJ is a periodic publication from LoanOfficerSchool.com designed to educate and inform our readers. Please note that we do not provide legal advice, and nothing in the LOSJ should be construed as a legal opinion on specific facts or circumstances. The content serves strictly for informational purposes. We strongly advise readers to consult legal counsel regarding any legal matters or specific questions.