Why Haven’t Loan Officers Been Told These Facts? New Process For LLPA Waiver

Understanding LLPA Waivers For First-Time Buyers

If you are not familiar with the specific pricing enhancements available to first-time buyers and others, now is a great opportunity to learn. To promote sustainable and equitable access to affordable housing, the Federal Housing Finance Agency (FHFA) announced targeted changes to the pricing structures of government-sponsored enterprises (GSEs) on October 24, 2022 (See link below). These changes include eliminating upfront fees for certain borrowers and affordable mortgage products. Additionally, the FHFA announced targeted increases in upfront fees for some cash-out refinance loans.

Loans for first-time homebuyers with income at or below applicable area median income (AMI) limits:

- At least one borrower on the loan must be a first-time homebuyer.

- Total qualifying income is at or below 100% of the applicable AMI for non-high-cost areas, and 120% for high-cost areas.

The Area Median Income

The Area Median Income (AMI) benchmark established by HUD has long been a vital part of credit policies. With the waiver of credit fees due to the implementation of federal law (HERA), it is crucial to understand AMI and its impact on originators’ ability to make competitive credit offers and promote informed loan decisions. Furthermore, it should go without saying that lenders cannot effectively compete in today’s mortgage market without fully leveraging the pricing discounts available to borrowers at, below, or near the AMI.

To determine the Area Median Income (AMI), the most accurate method is to use the Federal Information Processing Standards (FIPS) Code to identify the borrower’s eligibility. However, the Government-Sponsored Enterprises (GSEs) have simplified the process of finding the relevant AMI. Fannie Mae (FNMA) and Freddie Mac (FHLMC) provide comprehensive “Lookup Tools.”

Lenders can search for a property’s AMI using either the FIPS code or the property’s street address. It is important to calculate the applicable AMI based on the location of the property in question, rather than the applicant’s current address. It is essential that originators understand these boundaries, which enable significant pricing enhancements for borrowers.

Identifying AMI by county is straightforward. Lenders can assist real estate professionals in identifying, by property, the parameters that establish special first-time buyer financing and reduced credit terms using the property address or FIPS code.

FIPS codes uniquely identify census tracts, counties, and states. They are standards and guidelines for federal computer systems developed by the National Institute of Standards and Technology (NIST) in accordance with the Federal Information Security Management Act (FISMA) and approved by the Secretary of Commerce. These standards and guidelines are established when no suitable industry standards or solutions exist for a particular government requirement.

For DU submissions, FNMA intends to make minor changes to the calculation of AMI eligibility. See excerpts from the FNMA Announcement below.

From FNMA Announcement

The Area Median Income (AMI) eligibility determination for loan-level price adjustment (LLPA) waivers on HomeReady®, first-time homebuyer, and Duty to Serve loans is being standardized. This change will apply to all DU-underwritten loans sold to Fannie Mae with a Casefile Create Date on or after January 15, 2027.

This Notice provides information about an upcoming change to the Area Median Income (AMI)-based loan-level price adjustment (LLPA) waiver determination for first-time homebuyer and Duty to Serve loans.

To simplify and standardize the criteria for LLPA waivers that Fannie Mae currently offers on HomeReady®, first-time homebuyer,and Duty to Serve loans, we will begin using the Desktop Underwriter® (DU®) Casefile Create Date on all loans underwritten with DU to determine if the loan meets the AMI eligibility for the LLPA waiver.

This change modifies our current process, which uses the application received date to determine AMI eligibility for the LLPA waivers for first-time homebuyer and Duty to Serve loans.

Note: Loans delivered to Fannie Mae that were not underwritten with DU will continue to use the application received date.

This change will not affect the 2026 AMI file update. We are sharing this information now so lenders can review their internal systems and pricing engines.

FHFA 10/24/22 Announcement

FNMA AMI Lookup Tool Help

FNMA AMI Lookup Tool

LLPA Matrix (See page 5)

Area Median Income-Based Loan-Level Price Adjustment Waiver Determination

BEHIND THE SCENES: OFFICE OF THE COMPTROLLER OF THE CURRENCY ENFORCEMENT ACTION, FTC ACT SECTION 5 UDAP

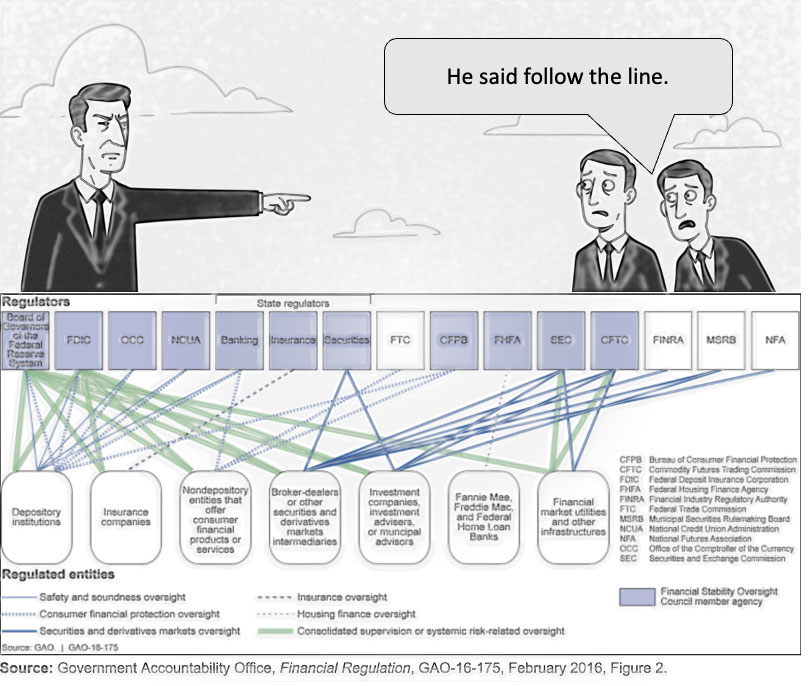

In most industries in the United States, a company is generally not visited by federal examiners who check that, among other things, it is safely profitable, not overly exposed to risks, well-managed, and serving the needs of the community.

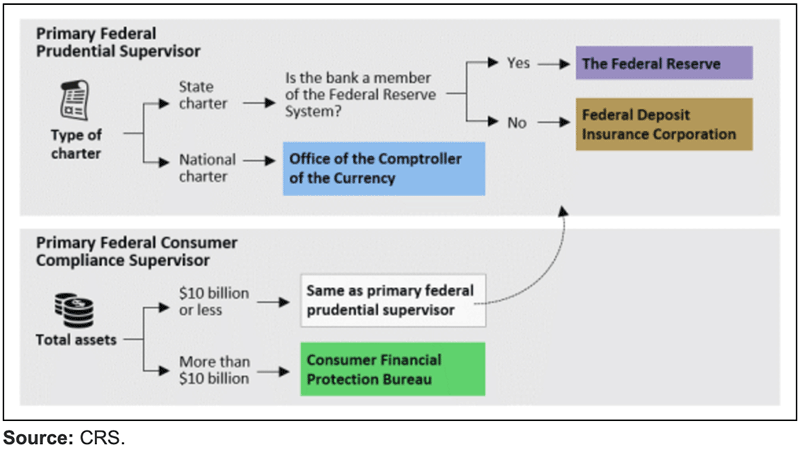

Banks are subject to two types of examinations. The first, a prudential exam, is conducted by the bank’s prudential regulator to determine whether the bank is financially sound. The second examination, sometimes called a functional examination, may or may not be conducted by the prudential regulator, and is to evaluate the bank’s compliance with consumer financial and fair lending laws.

The prudential regulator for a bank’s “safety and soundness” is determined by the bank’s charter type and whether it is a member of the Federal Reserve System. The federal prudential regulators are the Federal Reserve (Fed), the Office of the Comptroller of the Currency (OCC), and the Federal Deposit Insurance Corporation (FDIC). The National Credit Union Administration (NCUA) regulates federally chartered credit unions.

When an examiner identifies noncompliance, the issue may be elevated within the examination agency for resolution. When appropriate, as required by federal law, the examination agency may refer the matter to an appropriate enforcement agent. This referral could be to an internal agency department or an external federal agency, such as the Department of Justice. The subsequent enforcement investigation can take various forms and may be resolved with or without enforcement actions. If the enforcement division determines that violations are ongoing, one of its initial actions should be to issue a cease-and-desist order to halt the harmful practice. This order may be followed by further action such as a federal lawsuit seeking redress and other forms of relief, including financial sanctions.

The Consumer Financial Protection Bureau (CFPB) serves as the functional regulator for consumer and fair lending compliance for banks with assets exceeding $10 billion. For banks with assets below this threshold, their prudential supervisor also acts as the functional regulator. State-chartered banks are supervised by state-level regulatory agencies. Additionally, bank-holding companies, which are organizations that own banks, are regulated by the Federal Reserve. Companies that provide certain contracted services for banks are also subject to oversight by banking regulators.

The CFPB also examines nonbank financial institutions with assets of more than $10 billion for compliance with consumer financial laws and regulations, such as mortgage companies. The National Credit Union Administration (NCUA) is the safety and soundness regulator for all federal credit unions and those state credit unions that elect to be federally insured.

The Federal Trade Commission (FTC) may also act as a functional regulator for institutions not subject to oversight by the three federal prudential regulators. The basic statute enforced by the FTC, Section 5(a) of the FTC Act (UDAP), empowers the agency to investigate and prevent unfair or deceptive acts or practices affecting commerce.

Recent Enforcement Action by the Office of the Comptroller of the Currency (OCC)

Federal regulators possess considerable discretion in determining what specific allegations to bring against a violator. Several factors must be taken into account, including the necessary procedures to establish legal facts, the potential sanctions that may be imposed, and the likelihood of successful prosecution should the case proceed to adjudication.

In a recent mortgage noncompliance action, it’s notable that the OCC chose the FTC Act Section 5(a) (UDAP) complaint over the Dodd-Frank Title X Section 1031 UDAAP. The standards for proving unfair or deceptive acts are the same for both. However, the legal framework for the authority to prosecute differs. UDAAP also affords the agency with the “abuse prohibition” statute that Section 5 lacks. However, Section 5(a) may have less procedural baggage.

The enforcement action is similar to other recent federal prosecutions for FHA and VA program violations, alleging that mortgage lenders misrepresent government-insured loan programs. Another common complaint is that the lender is alleged to have implied a special relationship with the insuring agency. Lastly, and one of the all-time most common lender misrepresentations, the OCC suit specifically mentioned the loan officer taboo, the “you can always refinance” phrase. The implication is that the consumer can leverage a two-step process by refinancing to better financing when rates drop in the future. In reality, the misguided loan officer asserts the foul phrase when they are trying to close a prospect and don’t know what else to do or say. In a nutshell, the MLO wants to close a less-than-ideal transaction without overcoming underlying objections. Poor salesmanship and patently unlawful. Shades of loan churning.

Excerpted From the Consent Order

Between at least 2022 and 2024 (“relevant period”), the Bank made cash-out refinance loans guaranteed by the U.S. Department of Veterans Affairs (“VA”).

During the relevant period, the Bank made multiple false or misleading statements to consumers:

The Bank sent consumers millions of deceptive advertisements that stated the consumer had “available funds” and instructed the consumer to contact the Bank. In reality, the advertisement was a solicitation for a VA cash-out refinance loan and a new loan was required to access the funds.

Certain Bank employees made deceptive statements to consumers indicating that the Bank maintained a special relationship with the VA.

Certain Bank employees made deceptive statements to consumers regarding the terms of the VA cash-out refinance loans that created the impression that the consumer’s interest rate or monthly payment would significantly decrease within a defined time period. However, the cash-out refinance loan was a permanent loan with a fixed interest rate and mortgage payment, and the Bank could not in fact guarantee that the consumers would be able to refinance their loans with the lower interest or monthly payments as stated or implied by Bank employees.

The Bank’s deceptive statements induced consumers to obtain VA cash-out refinance loans, which resulted in certain consumers paying significant origination fees and receiving refinanced mortgage loans with significantly increased interest rates and monthly payments [Remember, federal and state laws require net benefits analysis for limited/no-cash-out only].

(4) The Bank is taking corrective actions to remedy the deficiencies identified in this Order. (5) By reason of the foregoing, the Bank has engaged in deceptive acts or practices in violation of Section 5 of the FTC Act, 15 U.S.C. § 45(a)(1). The Bank was unjustly enriched in connection with its violations of Section 5 of the FTC Act.

(1) Within thirty (30) days of the date of this Order, the Bank shall submit to the Assistant Deputy Comptroller, for review and prior written determination of no supervisory objection, the name, qualifications, and engagement terms of a proposed independent, third-party consultant (“Restitution Consultant”) to plan and oversee the payment of restitution to eligible consumers.

(2) Within sixty (60) days of the date of receipt of the OCC’s written determination of no supervisory objection to a Restitution Consultant, the Bank shall engage the Restitution Consultant and shall submit to the Assistant Deputy Comptroller, for review and prior written determination of no supervisory objection, a written methodology prepared by the Restitution Consultant to identify eligible consumers.

Tip of the Week – Have a Question About Operations, Sales, Marketing, or Compliance? Email Your Questions to the Loan Officer School Journal.

We invite LOSJ readers to submit questions on any topic to the editor. Topics can include compliance, sales, marketing, implementation, and other areas that may be helpful to our customers. If we use your question, we will include only your first name in our response. Please send your questions to: losjmailbag@gmail.com.

Necessary Mailbag Disclosure: The LOSJ is a periodic publication from LoanOfficerSchool.com designed to educate and inform our readers. Please note that we do not provide legal advice, and nothing in the LOSJ should be construed as a legal opinion on specific facts or circumstances. The content serves strictly for informational purposes. We strongly advise readers to consult legal counsel regarding any legal matters or specific questions.