Why Haven’t Loan Officers Been Told These Facts?

Uptick in Mortgage Delinquencies Spurs Unlawful Mortgage Assistance Scams

Mortgage loan originators can play a crucial role in protecting homeowners from fraudulent and harmful mortgage assistance scams. It is widely recognized that many homeowners struggle with financial difficulties when they don’t communicate effectively with their loan servicers or other relevant stakeholders. In some states, as long as borrowers are engaging with their servicers, it can be challenging for those servicers to move a loan to the default and foreclosure stages. However, if a borrower chooses to ignore their servicer or avoid communication altogether, this behavior can lead to a faster default and all the attendant difficulties.

Rescue Scam, FTC Enforcement Action

In a recent FTC enforcement action, the allegations describe standard procedures for a textbook default scam. The perpetrators are aware that the victims have limited financial resources, so their first deception is telling victims that they do not need to make any mortgage payments. This tactic allows the victims to free up their finances, which the perpetrators then exploit to collect advance fees. The allegations suggest that the defendants’ average advance fee was $2,000.

In exchange for an advance fee, the perpetrators provide consumers with a “Loan Restructuring Package” to send to their loan servicer. However, when the servicer explains that this is not how the process works, the victims often seek further guidance from the perpetrators, only to discover that the perpetrators are no longer responsive.

You can protect your customers from falling victim to these scams by normalizing discussions about mortgage difficulties. This is particularly important for first-time buyers. It’s essential to address how to handle financial uncertainty. A bit of sensitivity and wisdom will help determine the right timing for this discussion.

Do not abandon your customers at the closing table. Show your customers that you are with them through thick and thin. Many people experience financial hardship. Do not let shame and pride add to your customers’ suffering.

The Talk

“Mr. and Mrs. Borrower, I understand that purchasing a home can sometimes lead to concerns and uncertainties. It’s not uncommon to wonder about the possibility of having difficulty making mortgage payments. I want to acknowledge these concerns and assure you that you’re not alone in having these thoughts. Should you ever find yourself in a situation where paying your mortgage becomes challenging, I encourage you to reach out to me. Together, we can navigate any obstacles you may encounter. There are certain steps you can take, as well as important considerations to keep in mind, to help you manage these circumstances effectively. It is essential to know which actions to take and avoid when difficulties arise to protect your interests. Please know that I am here to support you in any way I can.”

Denial Is the Common Approach

Denial is a powerful psychological coping mechanism. It has its place. However, unbridled denial will lead to potentially ruinous outcomes. Consumers need to get help from qualified, capable sources. When their home, finances, and reputation are at stake, they should not turn to the internet or talk to robots.

FTC Press Release

At the Federal Trade Commission’s request, a U.S. district court in California has temporarily halted an allegedly deceptive mortgage assistance relief operation that claims it can provide mortgage relief assistance under the Coronavirus Aid, Relief and Economic Security (CARES) Act to lure and scam homeowners.

The court granted a temporary restraining order against National Amendment Assistance (also doing business as N.A.A.) after the mortgage assistance relief operator and related entities allegedly misled consumers into paying unlawful upfront fees in exchange for guarantees of lower mortgage rates and monthly payments that never materialized.

“When Americans look for ways to cut costs and lower their monthly bills, they shouldn’t have to worry about being targeted by mortgage scammers,” said Christopher Mufarrige, Director of the FTC’s Bureau of Consumer Protection. “When scammers try to take advantage of ordinary consumers, the FTC will act swiftly and decisively to stop such scams.”

According to the FTC’s complaint, since at least 2022, Southern California-based companies steered by Marinus Pieter Van Zweeden, Martin Howard Rub and Susan Jane Bustamante have mailed letters to homeowners nationwide claiming to offer mortgage relief under the CARES Act. These letters claim that consumers can obtain a reduction in their home mortgage rate due to a special mortgage adjustment program connected to a “CARES-Act Homeowner Assistance Fund or Lender Specific In-house Mortgage Adjustment Program” and urge the consumer to call a phone number to learn more. The complaint notes that the letters provide specific terms for the mortgage modification that the consumer is supposedly eligible to obtain, including a lower mortgage rate and monthly mortgage payment.

The defendants also allegedly misrepresent that consumers have a “grace period,” in which they do not need to pay their mortgage, according to the complaint.

The FTC alleges that these promises are false. Ultimately, the defendants do not obtain any mortgage relief for consumers and simply walk away with consumers’ upfront fees and financial information. Consumers—many of whom are often already in financial distress—have lost the money they paid to the defendants and have fallen behind on their mortgage payments, with some facing foreclosure or default.

The proposed complaint alleges that the defendants violate the law by deceptively:

- Promising mortgage loan modifications that will make consumers’ payments more affordable;

- Claiming their mortgage assistance relief services are associated with a federal government homeowner assistance plan;

- Instructing consumers that they do not have to or should not make monthly payments toward their mortgage;

- Collecting upfront payments before consumers executed a written agreement between the consumer and the loan holder or servicer; and

- Making false statements to induce consumers to provide the defendants with customer information of a financial institution, in violation of the Gramm-Leach-Bliley (GLB) Act.

The complaint alleges that the defendants have violated the FTC Act, Mortgage Assistance Relief Services (MARS) Rule, and the GLB Act, and the FTC seeks redress for affected consumers. The court entered a temporary restraining order against the defendants based on their alleged law violations.

The Commission vote authorizing the staff to file the complaint against the defendants was 2-0. The complaint was filed under seal in the U.S. District Court for the Central District of California, and the seal has now been lifted.

The defendants include Accounting Business Consultants Inc. (CA), Accounting Business Consultants Inc. (NV), Accounting Servicing Providers Inc., Amster Beene Partners Inc., Assertive Loan Advisors Inc., Independent Accounting Consulting Inc., United Administration Counseling Inc., United Bookkeeping Services Inc., and their three officers, Marinus Pieter Van Zweeden, Martin Howard Rub and Susan Jane Bustamante.

The CFPB’s current plan to downsize is noted in court documents from the lawsuit “National Treasury Employees Union v. Russell Vought,” 25-5091, (D.C. Cir.)

BEHIND THE SCENES: CFPB Publishes New “Enforcement Principles”

It’s been an eventful 2026 at the CFPB, marked by ongoing navel-gazing and methodical self-destruction. In the lawsuit filed by the National Treasury Employees Union against the CFPB Acting Director, the CFPB is seeking court permission to implement staff reductions that are only slightly less than originally planned by the Administration.

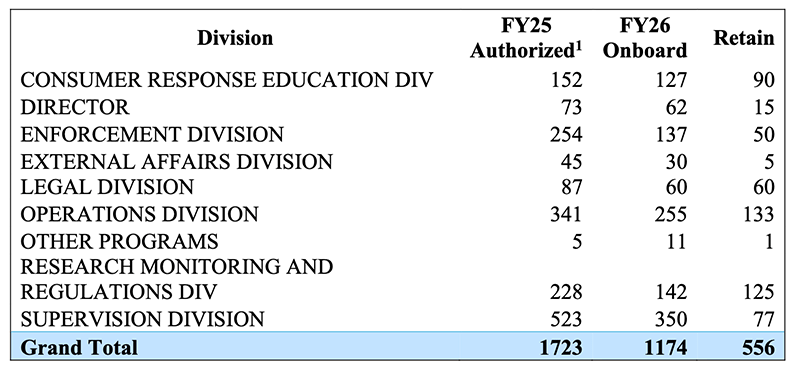

A recent court filing highlights the significant cuts planned for supervision and enforcement roles. The Bureau intends to reduce supervision staff by 85%, leaving just 77 employees to supervise some of the biggest and most dangerous institutions on the planet. With such a drastic reduction in supervision staff, there will be little need for enforcement, which is set to be cut by 80%, down to 50 employees.

One of the many challenges associated with rapid federal deregulation and oversight is the inevitable increase in local supervision and enforcement actions. On its face, this is not a bad thing for those who want less federal law enforcement. However, regulations and other administrative laws are easy come, easy go. It is probable that in the not-too-distant future, we will soon experience another round of federal re-regulation. The entire situation emanates instability and uncertainty, neither of which is helpful in light of the housing crisis.

From the National Consumer Law Center

WASHINGTON – In its latest attempt to shutter the nation’s top consumer watchdog, the Trump Administration has proposed another round of significant staff reductions at the Consumer Financial Protection Bureau (CFPB). The proposal, filed by CFPB Acting Director Russell Vought in the Court of Appeals for the D.C. Circuit, would eliminate all but about 550 positions – less than one-third of the staff in place when Trump took office.

“This latest attempt to eliminate essential staff at the CFPB would reduce the bureau to an empty shell, unable to fulfill the functions the CFPB is statutorily required to engage in,” said Chi Chi Wu, director of consumer reporting and data advocacy. “People need a strong, independent CFPB that is staffed to address unscrupulous practices by credit reporting companies, Wall Street banks, and big corporations.”

Last year, the CFPB had a staff of 1,750. It currently has 1,174, with many departures spurred by Acting Director Vought’s actions to cut benefits, contracts and services, and orders forbidding staff to work fully. This new proposal would cut existing staff by more than half. It proposes eliminating 85 percent of positions in the Division of Supervision, which oversees banks and other financial companies, and 80 percent of its enforcement staff, which brings proceedings when companies violate the law.

“Cutting consumer protections during an affordability crisis, while people are holding record credit card and student loan debt and facing rising prices for gas, groceries, and utilities, is tone deaf and cruel,” said Wu. “The CFPB was created to protect people from financial fraud and abuse, but these continued cuts are opening the door to fraudsters and cheats.”

From the CFPB

May 29, 2026

The New CFPB Enforcement Principles

Addressing Actual Harm to Consumers: CFPB focuses its enforcement on addressing actual harm to consumers. When an institution violates the law and causes real and meaningful harm to consumers, the CFPB uses its enforcement authority to ensure that violations are remedied and consumers are made whole. CFPB will not take action in cases where it believes consumers simply made unwise decisions, or cases involving theoretical or highly speculative harm.

Due Process: All Americans are entitled to know what the rules are before they are enforced against them, and the CFPB will ensure its enforcement actions comport with this basic tenet of due process. CFPB enforcement actions are rooted in a clear grant of statutory authority or a regulation promulgated through notice and comment. The CFPB does not seek to stretch the bounds of its statutory authority through novel interpretations or advance a policy agenda through its enforcement actions.

Collaboration: The CFPB is charged with taking appropriate enforcement action to address violations of Federal consumer financial law, including filing public enforcement actions when appropriate. But not all situations require an adversarial process and the pursuit of an enforcement action. The CFPB seeks to collaborate with institutions to remedy legal violations voluntarily and make consumers whole for any harm they have suffered. Institutions who self report violations will not be unnecessarily punished for their candor and willingness to proactively address problems. This approach maximizes the benefit to consumers, and ensures any harm can be addressed quickly, instead of waiting years for the resolution of litigation. In any event, the CFPB will take no more time than necessary to arrive at a fair resolution that accounts for the interests of consumers, institutions, and the CFPB.

Efficiency: CFPB is committed to maximizing its resources and operating efficiently. In addition to pursuing a more collaborative approach to addressing issues, the CFPB also refrains from engaging in duplicative enforcement work. CFPB does not pursue an enforcement action where the states or other regulators are better suited to do so. CFPB does not undertake such actions, or engage in joint actions, to run up its number of enforcement actions or in pursuit of good press coverage.

From the CFPB

May 28, 2026

The New CFPB Enforcement Priorities

The Bureau will focus its enforcement and supervision resources on pressing threats to consumers, particularly servicemembers and their families, and veterans. To focus on tangible harms to consumers, the Bureau will shift resources away from enforcement and supervision that can be done by the States. All prior enforcement and supervision priority documents are hereby rescinded.

- To avoid the ever-increasing number of supervisory exams, which are multiplying the cost of running businesses and raising consumer prices, Supervision shall decrease the overall number of “events” by 50%. The focus should be on conciliation, correction, and remediation of harms subject to consumers’ complaints. Supervision should focus on collaborative efforts with the supervised entities to resolve problems so that there are measurable benefits to consumers.

- The Bureau’s focus will shift back to depository institutions, as opposed to nondepository institutions. In 2012, 70% of the Bureau’s supervision focused on banks and depository institutions and 30% on nonbanks. Now that proportion has completely flipped, with over 60% on nonbanks and less than 40% on banks and depository institutions. The Bureau must seek to return to the 2012 proportion and focus on the largest banks and depository institutions.

- The Bureau will focus on actual fraud against consumers, where there are identifiable victims with material and measurable consumer damages as opposed to matters based on the Bureau’s perception that consumers made “wrong” choices. The areas of priorities are:

- Mortgages (getting the highest priority).

- Fair Credit Reporting Act/Regulation V data furnishing violations.

- Fair Debt Collection Practices Act/Regulation F relating to consumer contracts/debts.

- Various fraudulent overcharges, fees, etc.

- Inadequate controls to protect consumer information resulting in actual loss to consumers.

- The Bureau will focus on redressing tangible harm by getting money back directly to consumers, rather than imposing penalties on companies in order to simply fill the Bureau’s penalty fund.

- The Bureau will focus on providing redress to servicemembers and their families, and veterans.

- The Bureau will respect Federalism:

- The Bureau will deprioritize participation in multi-state exams unless required by statute (rather than merely permitted).

- The Bureau will deprioritize supervision where States have and exercise ample regulatory and supervisory authority, unless required by statute (rather than merely permitted).

- The Bureau will minimize duplicative enforcement, where State regulators or law enforcement authorities are currently engaged in or have concluded an investigation into the same matter.

- The Bureau will respect other federal agencies’ regulatory ambit:

- The Bureau will eliminate duplicative supervision or supervision outside of the Bureau’s authority (e.g., no supervision of M&A, just because regulated entities are involved, or attempt to insert itself into bankruptcy supervision).

- To the extent feasible, the Bureau will coordinate exams’ timing with other/primary federal regulators.

- The Bureau will minimize duplicative enforcement, where another federal regulator is currently engaged in or has concluded enforcement.

- The Bureau will not pursue supervision under novel legal theories, including of the Bureau’s authority. It will focus on areas that are clearly within its statutory authority.

- The Bureau will not engage in or facilitate unconstitutional racial classification or discrimination in its enforcement of fair lending law:

- The Bureau will not engage in redlining or bias assessment supervisions or enforcement based solely on statistical evidence and/or stray remarks that may be susceptible to adverse inferences.

- The Bureau will pursue only matters with proven actual intentional racial discrimination and actual identified victims. Such matters shall be brought to the leadership’s attention and maximum penalties will be sought.

- The Bureau will deprioritize the following:

- Loans or other initiatives for “justice involved” individuals (criminals).

- Medical debt.

- Peer-to-peer platforms and lending.

- Student loans.

- Remittances.

- Consumer data.

- Digital payments.

- The Bureau’s primary consumer enforcement tools are its disclosure statutes. The Bureau shall not engage in attempts to create price controls.

Tip of the Week: Sign up for 2026 CE

The LOSJ is celebrating five years of exceptional service to the mortgage industry, offering insights you won’t find anywhere else. To celebrate, enjoy our gift to you! Use the promo code “newsletter” when placing your class order.

Expanding your product offerings is an effective way to enhance your business’s vitality. This year, the Loan Officer School is surveying non-Qualified Mortgage (non-QM) financing options. We will review the various types of underwriting required for non-QM financing, including higher-priced mortgage loans (HPML), balloon-payment features, and interest-only options.

Presenting non-QM solutions to consumers improperly can lead to serious consequences. Understand the essentials of compliant and ethical subprime mortgage origination. Attend the Loan Officer School 2026 continuing education classes.

Please use the promo code “newsletter” when you sign up.

Have a Question About Operations, Sales, Marketing, or Compliance? Email Your Questions to the Loan Officer School Journal.

We invite LOSJ readers to submit questions on any topic to the editor. Topics can include compliance, sales, marketing, implementation, and other areas that may be helpful to our customers. If we use your question, we will include only your first name in our response. Please send your questions to: losjmailbag@gmail.com.

Necessary Mailbag Disclosure: The LOSJ is a periodic publication from LoanOfficerSchool.com designed to educate and inform our readers. Please note that we do not provide legal advice, and nothing in the LOSJ should be construed as a legal opinion on specific facts or circumstances. The content serves strictly for informational purposes. We strongly advise readers to consult legal counsel regarding any legal matters or specific questions.