Why Haven’t Loan Officers Been Told These Facts?

Federal Lawsuit, Imprisonment, and Forfeiture of Property Due to Misrepresentation of 1003 Assets

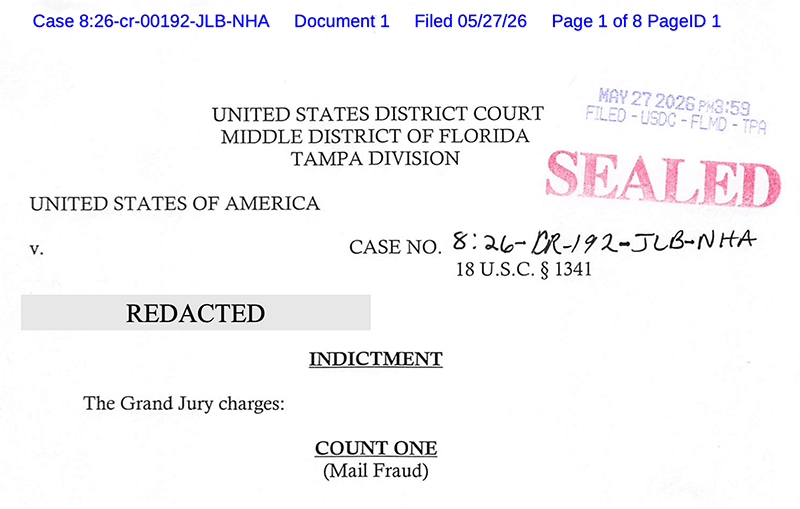

Loan Fraudster Indicted for Defrauding Wholesale Non-QM Lender

Is there a clear distinction between an honest mistake and criminal fraud in financial transactions? The answer is both yes and no. In many instances, the lending industry recognizes the fine line between loan application misrepresentations due to complex or obscure credit policies and deliberate efforts to defraud the lender.

A recent indictment filed by the Department of Justice in Florida alleges that the borrower orchestrated a sophisticated scheme to intentionally mislead the lender about his income. The charges are somewhat brief; however, the crux appears to be that the applicant misrepresented his cash flow to meet the underwriting requirements for a bank-statement loan.

The federal complaint filed in Florida last month is a fascinating prosecution for several reasons. Perhaps most significantly, there are specific allegations of fraud involving a non-QM wholesale lender and the 21st-century version of limited-documentation lending: the bank statement loan. Secondly, the defendant has gained some notoriety in the past year as an internet influencer who has gained the attention of numerous state and federal officials, including the Internal Revenue Service – Criminal Investigation, the Federal Bureau of Investigation, the Florida Office of Financial Regulation – Bureau of Financial Investigations, and the U.S. Department of Labor – Employee Benefits Security Administration.

This case is not the run-of-the-mill phony gift letter, phantom employer, or photo-shopped document complaint. The allegation describes how an applicant, with knowledge and sophistication, gamed the system and deliberately exploited the bank-statement loan manufacturing process. Bank statement loans can be risky to begin with, as lenders focus on a single dimension of an applicant’s cash flow and profitability. If you are unfamiliar with this ATR analysis method, it is quite simple. The applicant demonstrates income for the ATR analysis using business and/or personal bank account statements. The method is a reach for some applicant ATR determinations, as such documentation does not necessarily support essential analysis such as cash flow, profitability, or sustainability. This type of loan manufacture exploits the lack of specificity in the TILA ATR capacity design. Technically, bank statement loans may satisfy the TILA-ATR third-party record requirements, but in many instances, such loans should challenge an underwriter’s sensibilities.

The subject indictment briefly details how the defendant allegedly moved funds around from account to account to create an illusory and misleading appearance of personal cash flow.

From the URLA: Section 6: Acknowledgments and Agreements.

This section tells you about your legal obligations when you sign this application.

“The Lender and Other Loan Participants may rely on the information contained in the application before and after closing of the Loan. Any intentional or negligent misrepresentation of information may result in the imposition of:

(a) civil liability on me, including monetary damages, if a person suffers any loss because the person relied on any misrepresentation that I have made on this application, and/or (b) criminal penalties on me including, but not limited to, fine or imprisonment or both under the provisions of Federal law

(18 U.S.C. §§ 1001 et seq.).

Statutes for Everyday Mortgage Fraud

18 USC §1001. Statements or entries generally

(a) Except as otherwise provided in this section, whoever, in any matter within the jurisdiction of the executive, legislative, or judicial branch of the Government of the United States, knowingly and willfully-

(1) falsifies, conceals, or covers up by any trick, scheme, or device a material fact;

(2) makes any materially false, fictitious, or fraudulent statement or representation; or

(3) makes or uses any false writing or document knowing the same to contain any materially false, fictitious, or fraudulent statement or entry;

shall be fined under this title, imprisoned not more than 5 years”

18 USC §1014. Loan and credit applications generally; renewals and discounts; crop insurance

Whoever knowingly makes any false statement or report, or willfully overvalues any land, property or security, for the purpose of influencing in any way the action of the Federal Housing Administration . . . or a Federal Reserve bank, a Federal credit union, an insured State-chartered credit union, any institution the accounts of which are insured by the Federal Deposit Insurance Corporation,, any Federal home loan bank, the Federal Housing Finance Agency, the Federal Deposit Insurance Corporation, the Farm Credit System Insurance Corporation, or the National Credit Union Administration Board, or a mortgage lending business, shall be fined not more than $1,000,000 or imprisoned not more than 30 years, or both.

From the DOJ Complaint

Beginning on an unknown date, but no later than in or around November 2021, and continuing through in or around March 2022, in the Middle District of Florida and elsewhere, the defendant did knowingly and intentionally devise and intend to devise a scheme and artifice to defraud, and for obtaining money and property by means of false and fraudulent pretenses, representations, and promises about a material fact.

It was further a part of the scheme and artifice that in order to induce REDACTED to finance a loan for his personal residence the defendant would and did prepare and submit, and caused to be prepared and submitted, a false and fraudulent mortgage application that included multiple material false and fraudulent representations, and pretenses, such as:

- Overinflating the defendant’s personal income

- Representing that the deposits in the past 24 months of bank statements provided from the operating accounts of (Redacted, the defendant’s business) were the defendant’s personal income because he was the owner of those entities.

It was further a part of the scheme and artifice that the defendant would and did cause READCTED to approve the mortgage application and caused to be transmitted funds to purchase the residence.

Forfeiture of the Home

Upon conviction of a violation of 18 U.S.C. § 1341, the defendant shall forfeit to the United States, pursuant to 18 U.S.C. § 982(a)(l)(C) and 28 U.S.C. § 2461(c), any property, real or personal, which constitutes or is derived from proceeds traceable to the offense.

Mail Fraud 18 USC §1341. Frauds and swindles

Whoever, having devised or intending to devise any scheme or artifice to defraud, or for obtaining money or property by means of false or fraudulent pretenses, representations, places in any post office or authorized depository for mail matter, any matter or thing whatever to be sent or delivered by the Postal Service, or deposits or causes to be deposited any matter or thing whatever to be sent or delivered by any private or commercial interstate carrier, or takes or receives therefrom, any such matter or thing, or knowingly causes to be delivered by mail or such carrier according to the direction thereon, or at the place at which it is directed to be delivered by the person to whom it is addressed, any such matter or thing, shall be fined under this title or imprisoned not more than 20 years, or both.

From the Complaint

It was further a part of the scheme and artifice that the defendant would and did cause Lender 1 to mail closing documents to Title Company 1. It was further a part of the scheme and artifice that the defendant would and did cause Lender 1 to approve the mortgage application and caused to be transmitted funds to purchase the residence.

More Than Meets the Eye

There may be more to this than the DOJ lawsuit describes. In July of 2025, Florida Attorney General James Uthmeier issued subpoenas to the defendant’s business and its subsidiaries, arising out of allegations that the defendant’s business may have violated Florida’s Deceptive and Unfair Trade Practices Act or other laws. Subsequently, the defendant’s involvement in federal bankruptcy filings raised an ominous specter: that of defrauding real estate investors. The defendant was an internet personality who advertised seminars through his business, encouraging Floridians to invest in his real estate investment trust.

BEHIND THE SCENES: IS THE CFPB ERODING CONSUMER PROTECTIONS? THE CFPB RESPONDS: “Social Media Influencers Armed With AI Threaten the Complaint Database”

From The National Consumer Law Center (NCLC)

June 25, 2026 — Press Release

New Actions Targeted at Discouraging People from Challenging the Big Three Credit Reporting Companies

WASHINGTON – Yesterday, the Consumer Financial Protection Bureau (CFPB) launched a new broadside against its own consumer complaint database, making it increasingly difficult for people to seek help from the CFPB and shifting resources to discouraging people from disputing errors on their credit reports.

In its announcement Wednesday, the CFPB said it will require people to establish their identity with both a mobile phone and an email address before they are allowed to report the abusive actions of a large corporation. The CFPB also suggested it would pursue individuals who had “abused” the complaint system. The CFPB did not provide any information as to how it would distinguish “abuse” from legitimate concerns or any evidence to support its allegation of supposed widespread abuse.

“The Trump administration’s CFPB, at the behest of the credit reporting companies, is deliberately creating barriers for people to report illegal and abusive actions by large financial companies,” said Diane Thompson, deputy director and chief advocacy officer of the National Consumer Law Center. “The CFPB was created to protect consumers, not corporations, and should return to that mission.”

Credit reporting complaints are by far the biggest source of complaints to the CFPB, accounting for about 85 percent of all complaints, with consumers often describing problems with incorrect information. The consumer agency received more than 5.8 million complaintsabout credit and consumer reporting companies in 2025, doubling the complaint volume of the previous year.. These errors can drive up costs across every aspect of their financial lives.

In February, the CFPB also took steps to reduce the number of consumer complaints, sending aggressive warnings to people attempting to add a complaint to the database telling them not to submit a credit reporting complaint unless a dispute had already been formally filed with the credit reporting company. The notices, which went live on February 4, also require people to agree to onerous and legally dubious statements about their eligibility to seek help. The notices are not limited to complaints about credit reporting errors and appear before people can submit their requests for help for any financial issue ranging from mortgages to debt collection.

“The CFPB should be doing its job to make it easier for people to get help, not throwing new obstacles in their path,” said Chi Chi Wu, director of consumer reporting and data advocacy and acting co-director of federal advocacy at NCLC. “It should be focusing on the abuses of the credit reporting oligopoly, not acting in cahoots with it.”

NCLC February 9, 2026 — Press Release

Despite new hurdles, consumers should continue to submit complaints

WASHINGTON – Last week, the Trump-Vought Consumer Financial Protection Bureau (CFPB) moved to make it harder for people to seek help with financial problems by filing a complaint with the consumer agency. Consumers who file a complaint with CFPB are now hit with aggressive new warning notices alerting them not to submit a credit reporting complaint to the consumer agency unless a dispute has already been formally filed with the credit reporting agency (CRA).

The notices, which went live on February 4, also require people to agree to onerous and legally dubious statements about their eligibility to seek help. The notices are not limited to complaints about credit reporting errors, but they appear before consumers file complaints for any financial issue ranging from mortgages to debt collection.

The action was taken without any formal notice just days after the CFPB announced a public input process to collect more information on how the consumer complaint system is working. The changes also appear to follow industry requests made last month to reduce the number of consumer complaints about credit reporting errors submitted to the CFPB.

“Consumers are bound to find these warnings intimidating, given that the CFPB is the federal agency that Americans have come to rely on to get some relief from their unresolved disputes with big financial firms,” said Ruth Susswein, director of Consumer Protection at Consumer Action. “We encourage consumers to continue to submit complaints about ongoing credit reporting disputes with both the credit bureau and the CFPB. It is people’s right to report problems, and the agency’s responsibility to insist on a fair financial marketplace.”

“This appears to be an effort to stifle complaints. There’s absolutely nothing in the law that created the CFPB – the Consumer Financial Protection Act – that requires consumers to contact the credit bureaus before complaining to the CFPB,” said Chi Chi Wu, director of consumer reporting and data advocacy at the National Consumer Law Center. “People with complaints about their credit reports can choose to send a dispute first to the credit bureaus, and it triggers certain rights under a different law, the Fair Credit Reporting Act. But it’s their right to choose where to complain first.”

The consumer agency received more than 5.6 million consumer complaints in 2025, doubling the complaint volume of the previous year. Credit reporting complaints accounted for 85 percent of all complaints, with consumers often describing problems with incorrect information. These errors can drive up costs across every aspect of their financial lives. Companies reported more than 2 million people getting relief from filing a credit reporting consumer complaint in 2025.

“The credit bureaus wanted fewer complaints, and the Trump-Vought CFPB delivered,” said Tom Feltner, associate director for consumer policy at Americans for Financial Reform. “But those complaints represent real families facing real financial harm. Making it harder to complain about your mortgage or credit card doesn’t fix the problems—it just hides them from public view while people continue to pay the price.”

“Credit reporting errors and problems can cost families thousands in higher interest rates or even risk access to jobs, mortgages, auto loans, and credit cards and prevent people from becoming homeowners or buying cars,” said Christine Hines, senior policy director at the National Association of Consumer Advocates. “The CFPB’s complaint system exists to help consumers resolve these issues and alleviate some of the harm.”

“People should not have to jump through multiple, legally dubious hoops just to lodge a complaint about an error on their credit report,” said Demand Progress Education Fund Policy Director Emily Peterson-Cassin. “These changes implemented by the Trump administration will scare people away from making complaints, which is probably the point. The big banks and Wall Street hold our everyday financial lives in their hands and we should be able to call them out, at the very least.”

“Not only does the complaint system solve problems faced by millions of households across the country, but it also serves as a critical early warning system for state Attorneys General and other state financial regulators,” said Adam Rust, director of financial services at the Consumer Federation of America. “Obstructing consumers from making use of the complaint database undermines essential law enforcement activity.”

Congress created the complaint system and the CFPB with a mandate to ensure that consumers’ financial complaints would be addressed by banks, credit bureaus, debt collectors, mortgage servicers, and other companies that do business with them.

FROM THE CFPB

June 24, 2026

WASHINGTON, D.C. — The consumer complaint portal has long been plagued by issues that severely limit its effectiveness in addressing consumers’ complaints and practical utility of its information. Recently, CFPB has taken multiple concrete actions to address these issues and is continuing its work, including with Credit Reporting Agencies, to increase effectiveness of the process, while aligning it with the statutory authorities:

- Revising its Portal Manual to ensure that CRAs follow a standardized process in addressing complaints

- Enhancing identity protections

- Aligning the complaint process to statutory obligations

- Focusing resources on complaints that warrant a substantive response

- Educating consumers about how to address errors on their credit reports

- Increasing the efficiency of the complaint process

The consumer complaint portal has long been plagued by issues that severely limit its effectiveness in addressing consumers’ complaints and practical utility of its information. Recently, the CFPB has taken multiple concrete actions, including with Credit Reporting Agencies, to address these issues and is continuing its work to increase effectiveness of the process, while aligning it with the statutory authorities.

First, users abusing the process stress the systems of the Bureau and companies and impede timely processing of legitimate complaints. This harms consumers and wastes resources. Credit reporting complaint volume increased dramatically in recent years. In 2019, the Bureau received more than 150,000 credit or consumer reporting complaints. In 2025, that number grew to more than five million—an increase of more than 3,700%. Amidst this record complaint volume, the nationwide consumer reporting agencies (NCRAs)—Equifax, Experian, and TransUnion—reported making more updates and deletions to inaccurate tradelines than in prior years. In 2024, the NCRAs closed more than 1.3 million complaints with non-monetary relief. In 2025, that number grew to 2.1 million.

The increase is driven by many—sometimes, overlapping—factors: credit repair organizations and credit clinics misusing the Bureau’s complaint process as a tool of their business, social media influencers with questionable expertise encouraging followers to submit complaints, adoption of new technologies (e.g., “AI tools”) that may act as an individual’s agent, and the emergence of new businesses that seek to boost credit scores by disputing accurate information on consumers’ reports.

Second, the NCRAs have not been uniformly reporting how they respond to the growing number of consumer complaints. The Bureau has been collaborating with the NCRAs to better understand their complaint handling practices, and to ensure consumers receive timely, complete, and accurate responses to their credit reporting complaints. Credit reporting complaints represent the largest share of all complaints submitted to the Bureau.

Without addressing these issues, the CFPB cannot rely upon the consumer complaint portal data as a reliable reflection of actual market conditions or actual consumer experiences.

The Bureau is collaborating with NCRAs and other companies to implement the following changes to address these longstanding issues:

Increasing Clarity of Closure Definitions to Promote Consistency

Through its outreach to CRAs and other companies, the Bureau learned that companies operationalized the closure definitions differently with some companies using different definitions to categorize a complaint “Closed with non-monetary relief.”

What actions are we taking? The Bureau issued a new Company Portal Manual that provides clear information on how companies should use the various substantive and administrative response closure categories and answers to frequently asked questions. That will allow for standardization of data on responses across CRAs. Once the data can be standardized, the Bureau will continue to work with CRAs to ensure data are consistent across them and response rates are appropriately high.

Enhancing Identity Protections

Security is top of mind for the Bureau’s complaint system. Likewise, companies need reassurance that they are responding to their customer and safeguarding their privacy.

What actions are we taking? The Bureau launched two-factor authentication, requiring users who create online accounts to verify both their email address and mobile phone number. It also added clarifying text and new relationship categories to emphasize that third parties must disclose their involvement in the complaint process. The CFPB plans to implement address validation at the complaint submission step to ensure companies can act on high-quality information. The Bureau is also working on user support materials so adult children of aging parents, spouses of servicemembers, and other authorized representatives know how to submit complaints.

Aligning the Complaint Process to Statutory Obligations

The Fair Credit Reporting Act (FCRA) creates a framework in which individuals dispute inaccurate or incomplete information with consumer reporting agencies directly. Some credit repair clinics and individuals are using the Bureau’s complaint process to circumvent this statutory process.

What actions are we taking? The Bureau is aligning its complaint process to its statutory obligations. It added a notice, emphasizing that consumers must first exhaust their dispute rights directly with consumer reporting agencies before coming to the Bureau. The Bureau is working with the NCRAs to understand what information can help them more readily identify and review prior disputes. The Bureau is also exploring adding an additional administrative response option so NCRAs can efficiently return complaints where the consumer has not exhausted their FCRA dispute obligations. These changes will help the NCRAs focus their resources on complaints that warrant review as required by FCRA.

Focusing Resources on Complaints That Warrant a Substantive Response

When companies have reason to not respond to a complaint—such as one submitted by an unauthorized third party—the Bureau gives companies the ability to return complaints with an administrative response. Through its outreach, the Bureau learned that companies operationalized use of administrative response options differently.

What actions are we talking? The Bureau is collaborating with NCRAs and other companies to provide greater specificity of when to use existing administrative response categories. The Bureau is also exploring additional administrative response categories, such as when a user appears to be abusing the complaint process. The Bureau is exploring additional steps to support its efforts to monitor and safeguard the complaint system from users who attempt to abuse the complaint process.

Educating Consumers About How to Address Errors on Their Credit Reports

Some credit repair companies make claims that are too good to be true, such as guaranteeing a specific increase in credit scores or removing negative (but accurate) information. Social media financial influencers and new AI tools are also quickly changing the landscape.

What actions are we taking? The Bureau continues its work to develop and provide high-quality educational resources and tools for consumers, including materials highlighting the costs and risks of credit repair and how to spot fraud and scams.

Increasing the Efficiency of the Complaint Process

The Bureau is committed to leveraging technology to deliver faster, more secure services. The complaint process is focused on being a secure, digital-first service for all Americans.

What actions are we taking? The Bureau is building technology, like Application Programming Interfaces (APIs), to more efficiently share complaint information with companies. It will also be using software, like an address validation tool, to provide companies with high-quality information and reassurance that they are responding to their customer.

Defining Operational Categories to Manage Complaints Effectively

While many complaints are sent to companies for response or referred to other agencies automatically, some complaints require manual review. In discussing complaints, those received seconds or minutes ago but not yet sent, referred, or otherwise closed have been viewed the same as those received weeks or months ago. These complaints collectively have been referred to as the complaint “backlog” and have never been distinguished.

What actions are we taking? With record volume, the Bureau took a fresh look at which complaints should constitute a complaint backlog going forward. Most complaints are sent to companies or referred to another agency the same day they are received. For those that require manual review, the Bureau is distinguishing routine work from complaints in the backlog to help ensure that the Bureau can prioritize its work effectively and provide timely responses to consumers. For operational purposes, the backlog will include complaints awaiting action for more than 30 calendar days from the date of submission, whereas the remainder of complaints will be considered routine, work in progress.

Tip of the Week: Sign up for 2026 CE

The LOSJ is celebrating five years of exceptional service to the mortgage industry, offering insights you won’t find anywhere else. To celebrate, enjoy our gift to you! Use the promo code “newsletter” when placing your class order.

Expanding your product offerings is an effective way to enhance your business’s vitality. This year, the Loan Officer School is surveying non-Qualified Mortgage (non-QM) financing options. We will review the various types of underwriting required for non-QM financing, including higher-priced mortgage loans (HPML), balloon-payment features, and interest-only options.

Presenting non-QM solutions to consumers improperly can lead to serious consequences. Understand the essentials of compliant and ethical subprime mortgage origination. Attend the Loan Officer School 2026 continuing education classes.

Please use the promo code “newsletter” when you sign up.

Have a Question About Operations, Sales, Marketing, or Compliance? Email Your Questions to the Loan Officer School Journal.

We invite LOSJ readers to submit questions on any topic to the editor. Topics can include compliance, sales, marketing, implementation, and other areas that may be helpful to our customers. If we use your question, we will include only your first name in our response. Please send your questions to: losjmailbag@gmail.com.

Necessary Mailbag Disclosure: The LOSJ is a periodic publication from LoanOfficerSchool.com designed to educate and inform our readers. Please note that we do not provide legal advice, and nothing in the LOSJ should be construed as a legal opinion on specific facts or circumstances. The content serves strictly for informational purposes. We strongly advise readers to consult legal counsel regarding any legal matters or specific questions.