Why Haven’t Loan Officers Been Told These Facts?

Years ago, underwriting the stability of various forms of disability benefits could be a herculean task. Notably, Social Security Disability benefits were near impossible to use as effective income.

Underwriting faced the daunting task of reasonably concluding the income would continue for at least three years from application. Yet the agency’s benefits letter often alluded to the temporary nature of the benefit or that the benefit was subject to future disability findings.

Loan Officers were left to fend for themselves. Lacking training and supervision, ham-handed attempts to secure doctor’s notes, laboratory reports, and surgeons’ assessments would soon follow. What a mess it was. In fact, documenting Social Security Disability income was such an uphill struggle that many MLOs considered the income irrelevant for qualifying.

Between a Rock and Hard Place

Federal law prohibits unlawful discrimination. The ECOA enumerates discrimination against public income as a form of unlawful discrimination.

While ECOA makes it unlawful to discriminate against public assistance income, lenders were sometimes stuck between the stability of income issues and Regulation B discrimination prohibitions.

Regulation B 12 CFR § 1002.6(b)(2) Comment 6(b)(2)-6

Consideration of public assistance. When considering income derived from a public assistance program, a creditor may take into account, for example:

i. The length of time an applicant will likely remain eligible to receive such income.

ii. Whether the applicant will continue to qualify for benefits based on the status of the applicant’s dependents (as in the case of Temporary Aid to Needy Families, or social security payments to a minor).

iii. Whether the creditor can attach or garnish the income to assure payment of the debt in the event of default.

Public Assistance Under ECOA

Regulation B 12 CFR § 1002.2(z), Comment 2(z)-3

Public assistance program. Any Federal, state, or local governmental assistance program that provides a continuing, periodic income supplement, whether premised on entitlement or need, is “public assistance” for purposes of the regulation. The term includes (but is not limited to) Temporary Aid to Needy Families, food stamps, rent and mortgage supplement or assistance programs, social security and supplemental security income, and unemployment compensation. Only physicians, hospitals, and others to whom the benefits are payable need consider Medicare and Medicaid as public assistance.

The CFPB Clears the Air

Enter the CFPB and Regulation Z rule changes due to Dodd-Frank TILA amendments. In the initial QM implementation, the CFPB created Appendix Q, which is no longer in operation, to provide underwriting guidance to lenders. It was in Appendix Q that the CFPB made clear that absent a benefit termination date, it was permissible to consider certain public benefits as stable for purposes of calculating the DTI. Consequently, other changes soon followed, and now all agency loan (FNMA, FHLMC, VA, FHA, and USDA) policies are nearly identical concerning underwriting public benefits income. Additionally, the guidance may also apply to private disability benefits.

However, despite years of policy promulgation governing the underwriting of disability income, lenders still err in the documentary requirements and effective income calculus.

In examining FNMA and FHA’s requirements below, note the similarity in the policies. VA is much the same.

Generally, over-documenting income may not violate the law. However, that may be different for some protected incomes. ECOA prohibits discrimination based on income from public sources, such as social security disability payments. When the credit policies are explicit in the documentary requirements, and the lender asks for more than required, that request is an unnecessary burden on the applicant due to income from a public source and could be considered unlawful discrimination.

For example, the 4000.1 states, “the mortgagee must obtain a copy of the last Notice of Award letter, or an equivalent document that establishes award benefits to the Borrower, and one of the following documents.” The MLO knows the lender asks for everything, and rather than doing the back and forth with the applicant, the MLO asks for all four authenticating source documents rather than just the required one. As a result, the applicant needs help to provide all four and goes through a big hassle attempting to satisfy the requirement. Subsequently, the applicant gets upset with the MLO and, after the closing, files a complaint with Federal Trade Commission, who forwards the complaint to the FHA. The FHA confers with the CFPB, back to the FTC, and its knives out! Finally, someone sees the need for an investigation.

The FHA Single-Family Housing Policy Handbook 4000.1

II. ORIGINATION THROUGH POST-CLOSING/ENDORSEMENT

A. Title II Insured Housing Programs Forward Mortgages

4. Underwriting the Borrower Using the TOTAL Mortgage Scorecard (TOTAL)

Disability Benefits (TOTAL) Definition

Disability Benefits are benefits received from the Social Security Administration (SSA), Department of Veterans Affairs (VA), other public agencies, or a private disability insurance provider.

Required Documentation

The Mortgagee must verify and document the Borrower’s receipt of benefits from the SSA, VA, or private disability insurance provider. The Mortgagee must obtain documentation that establishes award benefits to the Borrower.

- If any disability income is due to expire within three years from the date of mortgage application, that income cannot be used as Effective Income.

- If the Notice of Award or equivalent document does not have a defined expiration date, the Mortgagee may consider the income effective and reasonably likely to continue.

- The Mortgagee may not rely upon a pending or current re-evaluation of medical eligibility for benefit payments as evidence that the benefit payment is not reasonably likely to continue.

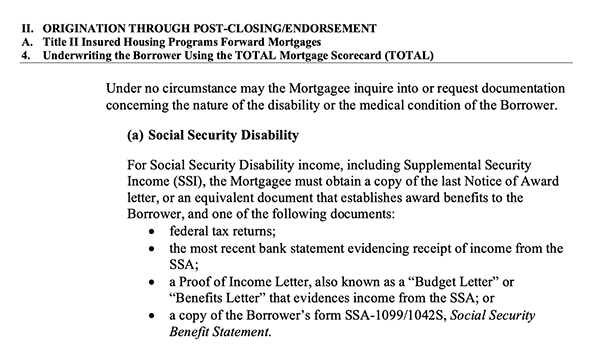

- Under no circumstance may the Mortgagee inquire into or request documentation concerning the nature of the disability or the medical condition of the Borrower.

(a) Social Security Disability

For Social Security Disability income, including Supplemental Security Income (SSI), the Mortgagee must obtain a copy of the last Notice of Award letter, or an equivalent document that establishes award benefits to the Borrower, and one of the following documents:

- Federal tax returns

- The most recent bank statement evidencing receipt of income from the SSA

- A Proof of Income Letter, also known as a “Budget Letter” or “Benefits Letter” that evidences income from the SSA

A copy of the Borrower’s form SSA-1099/1042S, Social Security Benefit Statement.

(b) VA Disability

For VA disability benefits, the Mortgagee must obtain from the Borrower a copy of the veteran’s last Benefits Letter showing the amount of the assistance, and one of the following documents:

- Federal tax returns

- The most recent bank statement evidencing receipt of income from the VA.

- If the Benefits Letter does not have a defined expiration date, the Mortgagee may consider the income effective and reasonably likely to continue for at least three years.

(c) Private Disability

For private disability benefits, the Mortgagee must obtain documentation from the private disability insurance provider showing the amount of the assistance and the expiration date of the benefits, if any, and one of the following documents:

- Federal tax returns

- The most recent bank statement evidencing receipt of income from the insurance provider

- The Mortgagee must use the most recent amount of benefits received to calculate Effective Income.

FNMA B3-3.1-09, Other Sources of Income (12/14/2022)

Disability Income — Long-Term

The below provides the verification requirements for long-term disability income. It does not apply to disability income that is received from the Social Security Administration.

Obtain a copy of the borrower’s disability policy or benefits statement from the benefits payer (insurance company, employer, or other qualified disinterested party) to determine:

- The borrower’s current eligibility for the disability benefits

- The amount and frequency of the disability payments

- If there is a contractually established termination or modification date

Generally, long-term disability will not have a defined expiration date and must be expected to continue. The requirement for re-evaluation of benefits is not considered a defined expiration date.

If a borrower is currently receiving short-term disability payments that will decrease to a lesser amount within the next three years because they are being converted to long-term benefits, the amount of the long-term benefits must be used as income to qualify the borrower.

Do you have a great value proposition you’d like to get in front of thousands of loan officers? Are you looking for talent?

BEHIND THE SCENES – Beguiling Notes From The Nations Housing Leader, A Strangely Familiar Tune

Which Song are They Playing?

Name That #$@!% Tune! (Answers at bottom)

FHFA Requests Input on the Enterprises’ Single-Family Pricing Framework

Baby, baby, I’ll meet you

Same place, same time

Where we can get together

And ease up our mind

Oh, do a little dance, make a little love

Get down tonight, whoo, get down tonight, hey

Do a little dance, make a little love

Get down tonight, get down tonight, baby

___________________________________

I think I did it again

I made you believe we’re more than just friends

Oh baby

It might seem like a crush

But it doesn’t mean that I’m serious

‘Cause to lose all my senses

That is just so typically me

Oh baby, baby

Oops, I did it again

I played with your heart, got lost in the game

Oh baby, baby

Oops, you think I’m in love

That I’m sent from above

I’m not that innocent

___________________________________

Baby you’ll come knocking on my front door

Same old line you used to use before

I said yeah, well, what am I supposed to do?

I didn’t know what I was getting into

So you’ve had a little trouble in town

Now you’re keeping some demons down

Stop draggin’ my

Stop draggin’ my

Stop draggin’ my heart around

___________________________________

You know, I’m not one

Of those high brows

I’m average Joe to you

I came up eating cornbread

Candied yams and chicken stew

Now you take that paper dollar

It’s only that in name

The way that buck has shrunk

It’s a lowdown dirty shame

That’s why I got the blues

Got those inflation blues

Answers Below

Tip of the Week – Deed Fraud, Talk to Your Referral Partners and Customers

Recent News Releases:

Philadelphia

“District Attorney Larry Krasner and the Philadelphia District Attorney’s Office Economic Crimes Unit today announced multiple charges against eight individuals for their role in a wide-ranging conspiracy to fraudulently obtain and transfer deeds involving 17 properties located across Philadelphia. This latest group of prosecutions, following charges against another sizable deed theft ring in March of last year, exemplifies the DAO’s continued commitment to seeking justice on behalf of communities hard-hit by deed fraud schemes.

This joint investigation with the Philadelphia Police Department’s Major Crimes Unit began in June of 2019, when information based on complaints filed with Philadelphia Police were provided to the Philadelphia District Attorney’s Office Economic Crimes Unit (ECU). The properties, ranging from empty lots to houses—including one residence from a woman in a nursing home — are located in Kensington, South and Southwest Philadelphia, and Northwest Philadelphia.”

NYC

NEW YORK – New York Attorney General Letitia James today announced the indictment of five members of a deed theft ring for allegedly stealing three homes worth more than $1 million in total from elderly, vulnerable homeowners in the Queens neighborhoods of Jamaica and St. Albans. The defendants impersonated the real homeowners of these properties by using forged drivers’ licenses and social security cards. They then used that forged information at contract signings and closings on the properties and forged the real owners’ signatures on deeds and real estate contracts.

“Deed Fraud continues to be a priority of our office that victimizes the most vulnerable homeowners of New York City,” said New York City Sheriff Anthony Miranda. “Perpetrators prey upon the elderly, the financially disadvantaged, and the medically infirmed through deception and a variety of nefarious schemes. The Sheriff’s Bureau of Criminal Investigation will continue to coordinate our effort to protect homeowners and investigate these horrific thefts along with all of our law enforcement partners in the city. We commend the actions of the New York Attorney General’s Office Real Estate Enforcement Unit for their investigation which resulted in today’s arrests and thank them for their continued efforts in this area.”

US Attorney’s Office, Southern District of California

SAN DIEGO – Mazen Alzoubi, a longtime Southern California real estate investor, was sentenced today to 75 months in custody by U.S. District Judge Cynthia Bashant for leading a scheme to steal title to homes and then “sell” the properties to unsuspecting buyers – before the buyers realized who the true owners were and before the true owners could put a stop to the sale.

From September 2012 through his arrest in November 2014, Alzoubi fraudulently sold or attempted to sell at least 15 homes worth more than $3.6 million that actually never belonged to him. On at least ten occasions, he was successful—earning illicit proceeds of nearly $2.2 million.

Alzoubi pleaded guilty in January 2016 to fraud, money laundering, and identity theft. As part of this plea, he admitted that he forged deeds that would make it appear the true owners of property had sold the home to a sham “investment” business Alzoubi controlled, when, in reality, the true owners were entirely unaware of Alzoubi’s actions.

Alzoubi would then record the forged deeds at county recorder’s offices, to make them appear legitimate. Once the fraudulent documents were recorded in the chain of title, Alzoubi would pose as the new owner—using a web of aliases and sham businesses (with names like “Land Investments 01”) and immediately try to sell the properties. Alzoubi worked with co-conspirators to set up bank accounts for the sham companies, so that the proceeds could be diverted directly to them. In this way, Alzoubi collected all the proceeds of the sale, and the true owners were left with nothing.

Alzoubi and his co-conspirators assumed the identities of others in order to keep the scheme going, setting up dummy email accounts and obtaining fake driver’s licenses. They also forged the signatures and notary stamps of real notaries to make fake documents look legitimate, and forged the signatures of real lawyers to prepare and file fraudulent court documents. Alzoubi, the ringleader of the scheme, assumed multiple fake identities to keep the fraud going. He also posed as real people, pretending on one occasion that he was the attorney for one of the true owners. (Unbeknownst to Alzoubi at the time, he was talking to an undercover federal agent.) As a result, Alzoubi was charged with, and pled guilty to, aggravated identity theft, which carries a mandatory sentence of 2 years in prison in addition to his sentence for the fraud and money laundering.”

Another Added Value, Post-Closing Subject Worth Discussion

While some misguided sages have downplayed deed theft as a marketing ploy, or much ado about nothing, the growing number of victims suggests otherwise. While deed theft is still a remote possibility for most homeowners, so is a home invasion. Yet given the choice, most folks choose to lock their doors and windows at night.

And while the assertion that your house can’t be stolen is somewhat true, the after-effects of title fraud can be inconvenient at a minimum and potentially significantly damaging.

MLOs should always be on the lookup for ways to bring added value to their customers. A free service that could mitigate incalculable headaches is a no-brainer.

Deed theft generally involves fraud at or by the county recorder’s office, as that is who does the recording making the fraud possible. Thus it is no surprise that initiatives to combat the issue are at the county level. LA County is a pioneer in this area, launching its notification service in 1996. Since then, many other counties have been following suit. Consequently, where available, it makes sense for homeowners to sign-up for these free services that notify homeowners if their name or property deed turns up at the recorder’s office. Like an alert with your credit card or bank account, the service provides timely notification that may enable victims to minimize potential deed-theft impacts.

Check with your city or county and pass along the service information to your valuables customers.

American Bar Association Article