Why Haven’t Loan Officers Been Told These Facts?

Updates to VA’s State Fees and Charges Deviations List

1. Purpose. The purpose of this Circular is to announce an update to the Department of

Veterans Affairs (VA) State Fees and Charges Deviations List.

2. Background. VA may authorize, in advance, local fee variances for additional fees and

charges that may be charged to and paid by the Veteran based on the location of the subject

property. VA publishes a list of these deviations on its website at: State Fees and Charges

Deviations List. Lenders should refer to the Circular 26-24-19, Invoice Requirements for Itemized Fees and Charges and Updates to the State Fees & Charges Deviations List, for additional information on how to use the State Fees & Deviations list.

3. Action. Lenders are expected to immediately utilize the new VA State Fees and Charges

Deviations List and continue to comply with the procedures regarding itemized fees and charges

outlined in Circular 26-24-19.

4. Effective Date. This Circular is effective for loans closed on or after the date of this Circular.

5. Questions. For questions or comments, please submit a request through VA’s ServiceNow

Portal, Loan Guaranty Support, or contact VA by phone at 1-877-827-3702, between the hours

of 8:00 AM and 6:00 PM Eastern time.

6. Rescission. This Circular is valid until rescinded.

VA Pamphlet VAP26-7 Chapter 08 Borrower Fees

VA Circular 26-26-1 (VA’s State Fees and Charges Deviations List)

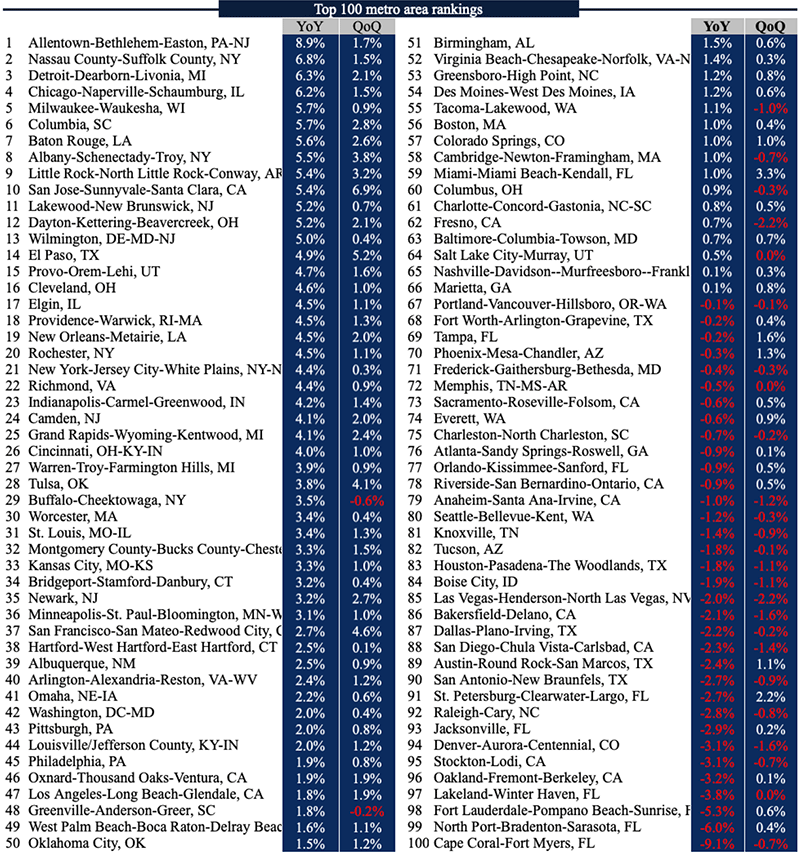

Fig 1. Courtesy of the FHFA

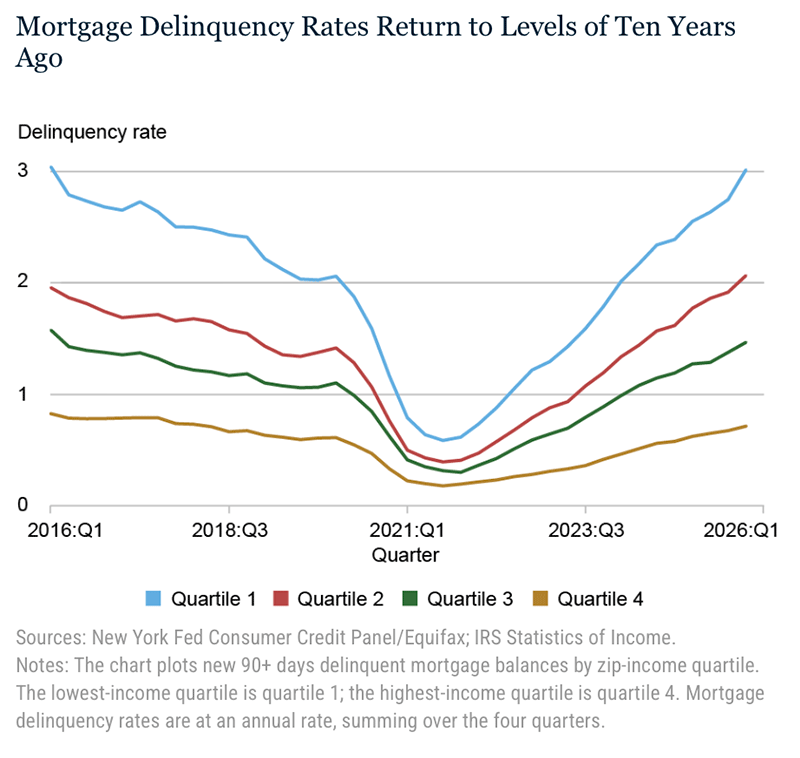

Fig 2. Courtesy of the New York Fed

BEHIND THE SCENES: ROUGH SEAS AHEAD, PREDICTING PROBLEM MARKETS

The Federal Reserve Bank of New York’s Center for Microeconomic Data recently released its Quarterly Report on Household Debt and Credit for the fourth quarter of 2025, showing a continued increase in household debt levels.

The New York Fed chart (Fig. 2) indicates that lower-income households are more susceptible to economic pressures, leading to significant mortgage delinquencies. This is well known to mortgage originators: serious delinquencies are often linked to insufficient cash reserves. Many lower-income households live paycheck to paycheck.

What other factors strongly correlate with serious mortgage delinquency? Data from the New York Fed identifies two significant correlating factors: the area unemployment rate and declining housing values.

In a local market, the presence of two or more of these factors will lead to a significant increase in serious delinquencies, especially in areas with a high concentration of lower-income households. When these three factors combine—lower-income households, higher unemployment, and declining property values— it can create a disastrous combination.

Additional factors significantly influence loan performance. It is widely recognized that higher debt-to-income (DTI) ratios and lower credit scores are associated with higher mortgage delinquency rates.

Which mortgage portfolio aligns more closely with all five factors than other market segments? Government-insured loans.

The Government Thinks Banks Will Save the Day

There has been a push to get the banks back into the mortgage business. Recently, federal regulators proposed easing the capital requirements for banks. Capital requirements are essential, serving as required reserves or a financial moat to insulate originators and servicers from non-performing loans. Increasing or decreasing capital requirements is another lever in the federal government’s monetary policy. Although this seems to be yet another example of “regulatory capture.” See the link below on regulatory capture.

When a loan servicer does not receive timely payments, they are still required to make payments to investors as if everything is normal. However, if a significant number of loans stop making payments, it can strain the servicer’s finances. To prevent banks from running out of money, the government requires them to maintain substantial reserves for nonperforming loans. In a risky lending environment, banks tend to reduce the number of higher-risk loans they originate to mitigate the potential for performance issues and the ensuing capital squeeze.

In light of the current economic challenges, one could argue that easing credit standards could stimulate spending. Conversely, because spending is slowing and due to economic uncertainties, it may be time for stricter regulations. Understand clearly that the regulatory move aims to increase riskier lending.

In the short term, easing monetary policy could encourage increased consumption. However, considering the rising levels of consumer debt, this approach may be a case of “throwing good money after bad.”

Interesting Times

The current economy is often described as a “K-Shaped” economy, where one segment of the population is thriving while another is struggling.

Nevertheless, there’s always the option of McDonald’s $3.00 Value Meal for those looking for affordable choices. What next, Soylent Green?

“It was the best of times, it was the worst of times, it was the age of wisdom, it was the age of foolishness, it was the epoch of belief, it was the epoch of incredulity, it was the season of light, it was the season of darkness, it was the spring of hope, it was the winter of despair.”

― Charles Dickens, A Tale of Two Cities

Tip of the Week – Have a Question About Operations, Sales, Marketing, or Compliance? Email Your Questions to the Loan Officer School Journal.

We invite LOSJ readers to submit questions on any topic to the editor. Topics can include compliance, sales, marketing, implementation, and other areas that may be helpful to our customers. If we use your question, we will include only your first name in our response. Please send your questions to: losjmailbag@gmail.com.

Necessary Mailbag Disclosure: The LOSJ is a periodic publication from LoanOfficerSchool.com designed to educate and inform our readers. Please note that we do not provide legal advice, and nothing in the LOSJ should be construed as a legal opinion on specific facts or circumstances. The content serves strictly for informational purposes. We strongly advise readers to consult legal counsel regarding any legal matters or specific questions.