Why Haven’t Loan Officers Been Told These Facts?

HUD Issues “Dear Colleague” Letter to Clarify HUD’s Interpretation of the FHA Anti-Steering Rules.

Washington, DC – The U.S. Department of Housing and Urban Development (HUD) sent a “Dear Colleague” letter to real estate professionals clarifying they are not violating the Fair Housing Act when they share information with prospective homebuyers about neighborhood crime rates and school quality data.

“Buying a home is one on the most significant decisions a family will ever make,” said Secretary Scott Turner. “Americans should not be left in the dark about vital facts like neighborhood safety or school quality. HUD is making clear that real estate professionals can openly and lawfully provide this information in an equal and consistent manner to American families.”

In the letter, Assistant Secretary for Fair Housing and Equal Opportunity Craig Trainor explains that unlawful steering under the Fair Housing Act requires intentional discrimination based on protected characteristics. Providing prospective homebuyers with information about school quality and crime data is not a violation when it is shared consistently without discriminatory intent.

Accordingly, Fair Housing Assistance Programs (FHAPs) should not issue discrimination findings solely because real estate professionals provide such information or answer nonracial questions on these topics in a consistent and unbiased manner. Likewise, Fair Housing Initiatives Programs (FHIPs) should not use federal funds to pursue complaints based on these same practices.

Equipped with more information, Americans will be better situated to find affordable, decent, and fair housing that meets their families’ needs.

During the Biden Administration, major real estate brokerages and listing platforms discouraged or restricted the sharing of neighborhood information, citing fair housing concerns. These changes were shaped not by the law’s requirements but out of an effort to implement diversity, equity, and inclusion (DEI) ideology.

Pushed by activists and bureaucrats, this project treated the use of data related to crime statistics and school ratings as inherently discriminatory. This moratorium on sharing crime and school quality information has only resulted in less transparency for potential homebuyers and renters, and it threatened real estate professionals with perceived liability should they offer their clients the critical information they need when evaluating where to live.

Fair housing protections and informed consumer choice go hand in hand, and the Fair Housing Act does not require withholding useful information on school quality and crime statistics. This letter helps deliver on HUD’s commitment to expanding access to safe, decent, affordable, and fair housing by equipping Americans with the knowledge they need to make informed housing decisions.

Neighborhoodscout.com: Subscription Service, Schools and Crime Data

BEHIND THE SCENES: PREDICTIONS: WHAT WILL THE REMAINDER OF 2026 BRING TO HOUSING?

Typically, experts estimate the risk of a recession in the immediate 12 months ahead at about 20%. Recession sentiment shifts with the winds, but there is no doubt that the professionals who closely watch the indicators are growing increasingly bearish.

Warren Buffett, of Berkshire Hathaway, currently sitting on $400 billion in cash, recently commented on the investing environment, saying, “It isn’t our ideal surrounding area — or environment, I should say — in terms of deploying cash for Berkshire,” the former CEO told CNBC’s Becky Quick. He attributed the current unfavorable environment to high stock valuations. However, could he also be bearish about the economic forecast?

While the trending predictions are not guarantees, they indicate an elevated risk. Predictions are difficult to make. If it all came down to known indicators or historic norms, it would be easy. Predictions are like playing dodgeball. The ball you don’t see coming is the one that hits you in the face.

Moody’s Analytics has increased its recession outlook for the next 12 months to 48.6%, while Goldman Sachs has raised its estimate to 30%. The highly regarded wealth advisory firm Wilmington Trust has the odds at 45%, while EY Parthenon, a leading strategic consulting firm, has it at 40%, with the caveat that “those odds could rapidly rise in the event of a more prolonged or severe Middle East conflict.”

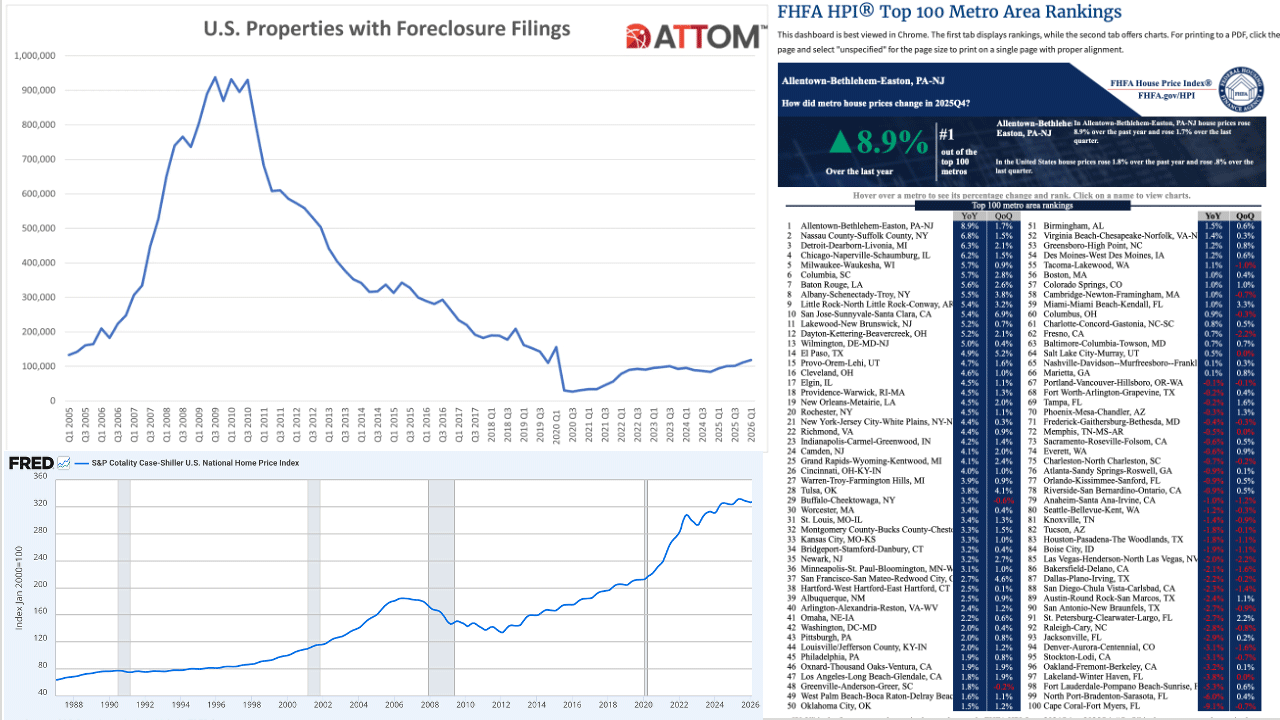

Foreclosure Statistics

From the ATTOM Q1 2026 Foreclosure Report

Those major metros with a population of 200,000 or more that had the greatest number of foreclosures starts in Q1 2026 included New York, NY (3,868 foreclosure starts); Houston, TX (3,614 foreclosure starts); Chicago, IL (3,401 foreclosure starts); Atlanta, GA (2,520 foreclosure starts); and Dallas, TX (2,427 foreclosure starts).

Worst foreclosure rates in Indiana, South Carolina, and Florida

Nationwide one in every 1,211 housing units had a foreclosure filing in Q1 2026. States with the worst foreclosure rates were Indiana (one in every 739 housing units with a foreclosure filing); South Carolina (one in every 743 housing units); Florida (one in every 750 housing units); Delaware (one in every 757 housing units); and Illinois (one in every 833 housing units).

Among 227 metropolitan statistical areas with a population of at least 200,000, those with the worst foreclosure rates in Q1 2026 were Lakeland, Florida (one in every 409 housing units); Punta Gorda, FL (one in 416); Columbia, SC (one in 440); Fayetteville, NC (one in 480); and Macon, GA (one in 492).

Report conclusion

Foreclosure activity continued to trend upward in Q1 2026, with both starts and completions increasing year-over-year. While volumes remain low by historical standards, the sustained growth over recent quarters may point to a market gradually adjusting to broader economic pressures.

Tip of the Week – Have a Question About Operations, Sales, Marketing, or Compliance? Email Your Questions to the Loan Officer School Journal.

We invite LOSJ readers to submit questions on any topic to the editor. Topics can include compliance, sales, marketing, implementation, and other areas that may be helpful to our customers. If we use your question, we will include only your first name in our response. Please send your questions to: losjmailbag@gmail.com.

Necessary Mailbag Disclosure: The LOSJ is a periodic publication from LoanOfficerSchool.com designed to educate and inform our readers. Please note that we do not provide legal advice, and nothing in the LOSJ should be construed as a legal opinion on specific facts or circumstances. The content serves strictly for informational purposes. We strongly advise readers to consult legal counsel regarding any legal matters or specific questions.