Why Haven’t Loan Officers Been Told These Facts?

Underwriting

Consumer mortgage solutions and the associated underwriting methodologies can be classified into three primary categories. Each category encompasses a range of specific requirements and exceptions; however, for clarity, this discussion will focus on the general differences in underwriting practices for Higher-Priced Mortgage Loans (HPML). This article outlines the qualifying payment underwriting mandates established under the Truth in Lending Act (TILA). Lenders retain the discretion to implement risk management strategies as they deem appropriate, thereby establishing what is commonly referred to as credit overlays.

The three broad categories that dictate qualifying payment calculations include:

- Qualified Mortgage (QM)

- Higher-Priced-Mortgage-Loan (HPML)

- Non-QM

HPML loan products can be categorized as either Qualified Mortgage (QM) or Non-Qualified Mortgage (Non-QM). High-Cost loans, defined by HOEPA and Regulation Z, Section 32, are not included in our evaluation due to their extremely limited market. Most lenders do not originate High-Cost loans, and most investors are not willing to purchase them.

HPML is defined in Regulation Z and constitutes a specific threat to consumers and lenders alike. Consequently, Regulation Z raises the bar for mitigating default risk.

Non-QM lending typically includes both HPML and non-HPML loans. MLOs can effectively improve customers’ credit landscape by avoiding unnecessary HPML solutions. Therefore, understanding the boundaries of HPML is essential.

Defining HPML Boundaries

Regulation Z 12 CFR § 1026.35(a)(1) describes an HPML as (1) “Higher-priced mortgage loan” means a closed-end consumer credit transaction secured by the consumer’s principal dwelling with an annual percentage rate that exceeds the average prime offer rate for a comparable transaction as of the date the interest rate is set:

(i) By 1.5 or more percentage points for loans secured by a first lien with a principal obligation at consummation that does not exceed the limit in effect as of the date the transaction’s interest rate is set for the maximum principal obligation eligible for purchase by Freddie Mac;

(ii) By 2.5 or more percentage points for loans secured by a first lien with a principal obligation at consummation that exceeds the limit in effect as of the date the transaction’s interest rate is set for the maximum principal obligation eligible for purchase by Freddie Mac; or

(iii) By 3.5 or more percentage points for loans secured by a subordinate lien.

The “average prime offer rate” (APOR) is an annual percentage rate derived from the average interest rates, points, and other loan pricing terms currently offered to consumers by a representative sample of creditors for mortgage transactions with low-risk pricing characteristics.

When originating a consumer mortgage, lenders must assess the transaction to determine if it qualifies as a Higher-Priced Mortgage Loan (HPML). They are required to compare the subject APR against the Average Prime Offer Rate (APOR) benchmark to accurately identify HPML status.

The APOR (Average Prime Offer Rate) is a benchmark that reflects the best interest rates available for well-qualified non-government borrowers. It serves as a reliable composite benchmark for prime residential mortgage financing. Lenders choose the appropriate APOR based on the specific loan type. For instance, if the mortgage in question is a 5-year hybrid adjustable-rate mortgage (ARM), the lender will select the corresponding APOR for that product. The Consumer Financial Protection Bureau (CFPB) publishes 15 APOR types, including fixed and ARM products, each week.

HPML Balloon

HPML necessitates added consumer protections. For example, HPML financing with a balloon payment. The creditor must determine the consumer’s repayment ability based on the loan’s payment schedule, including any balloon payment. Assume a higher-priced covered transaction with a fixed interest rate of 7 percent. The loan amount is $200,000, and the loan has a 10-year term but the payments are based on a 30 year amortization. The scheduled monthly payment for the first ten years is $1,331, with a resulting balloon payment of $172,955. The creditor must consider the consumer’s ability to repay the loan based on the payment schedule that fully repays the loan amount, including the balloon payment of $172,955. $200,000 amortized over 120 months is $2,322.17 per month. The lender must make a reasonable and good-faith assessment that the applicant has the ability to repay $2,322.17 P&I, in addition to their other obligations, and has sufficient residual income to live on.

Non-HPML Balloon

Contrast the stringent HPML balloon income test against the non-HPML income test. For loans that include a balloon payment and are not classified as “higher-priced covered transactions,” the lender should base calculations on the highest scheduled payment amount within the first five years of the loan, starting on the date the first regular periodic payment is due. As long as the balloon payment falls outside this five-year window, it is not considered in the ATR.

Neither Regulation Z nor the Truth in Lending Act (TILA) specifies an underwriting methodology for calculating the ability-to-repay. However, lenders often set either a maximum debt-to-income (DTI) ratio or a minimum residual income requirement. Mortgage Loan Originators (MLOs) must know how to accurately calculate the mortgage qualifying payment to assess DTI and residual income factors.

Understanding the limits of riskier transactions helps MLOs avoid overly strict underwriting requirements, pricier solutions, and riskier loan features for their customers.

Join us for an in-depth exploration of underwriting non-QM loans at the Loan Officer Schools’ 2026 CE.

Signup here:

LOAN OFFICER SCHOOL 2026 CE

Use promo code “newsletter”

BEHIND THE SCENES: CFPB CONSUMER RESPONSE ANNUAL REPORT, January 1 – December 31, 2025

12 U.S.C. 5493(b)(3) Collecting and tracking complaints

The [CFPB] Director shall establish a unit whose functions shall include establishing a single, toll-free telephone number, a website, and a database or utilizing an existing database to facilitate the centralized collection of, monitoring of, and response to consumer complaints regarding consumer financial products or services. The Director shall coordinate with the Federal Trade Commission or other Federal agencies to route complaints to such agencies, where appropriate.

Reports to the Congress

The Director shall present an annual report to Congress not later than March 31 of each year on the complaints received by the Bureau in the prior year regarding consumer financial products and services. Such report shall include information and analysis about complaint numbers, complaint types, and, where applicable, information about resolution of complaints.

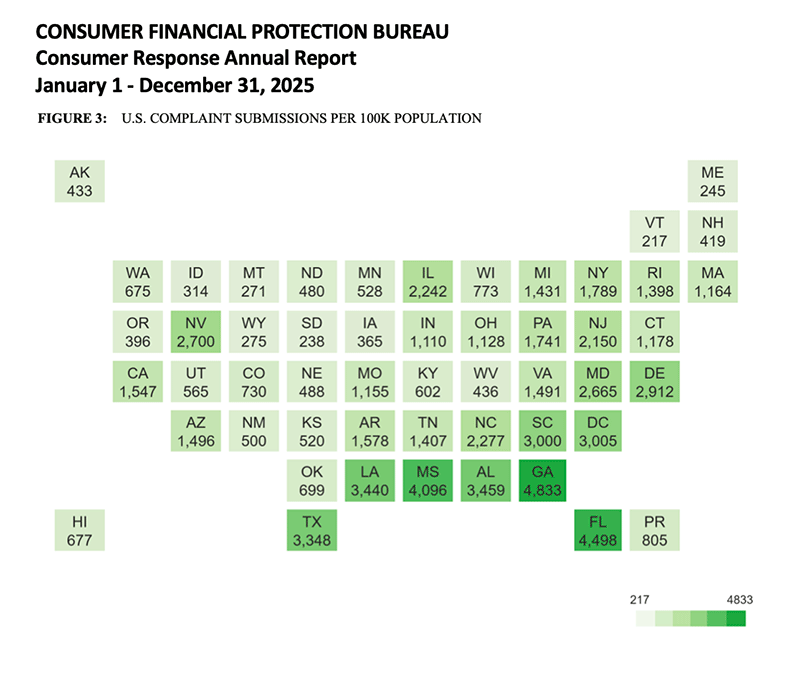

It’s Not All Peachy in Georgia, Highest CFPB Complaints per Capita

Annually, the Consumer Financial Protection Bureau (CFPB) publishes a comprehensive complaint report in accordance with the requirements set forth in Dodd-Frank Title 10. The report draws attention to potential areas of concern within consumer finance that may warrant further investigation.

Complaints have steadily increased since the complaint department began, originating from consumers or their representatives. The CFPB accepts complaints about various consumer issues including:

- Checking and savings accounts

- Credit cards

- Credit reports and other personal consumer reports

- Debt collection

- Debt and credit management

- Money transfers, virtual currency, and money services

- Mortgages

- Payday loans

- Personal loans like installment, advance, and title loans

- Prepaid cards

- Student loans

- Vehicle loans or leases

2025 Complaints Excerpts

The number of consumer complaints to the CFPB has continued its year-over-year increase. In 2019, the CFPB received approximately 352,400 complaints. Two years later, in 2021, that number grew to

994,000 complaints. Two years after that, in 2023, the number reached 1,657,600 complaints.

Since then, the number of complaints have roughly doubled each year: 3,187,900 complaints in 2024 and 6,635,400 complaints the CFPB received in 2025.

Of the approximately 6,635,400 complaints the CFPB received in 2025, it sent approximately 5,984,100 (or 90%) to companies for review and response, referred 3% to other regulatory agencies, and found 7% to be not actionable. As of March 2, 2026, 0.03% of complaints were pending with the consumer and 0.03% were pending with the CFPB.

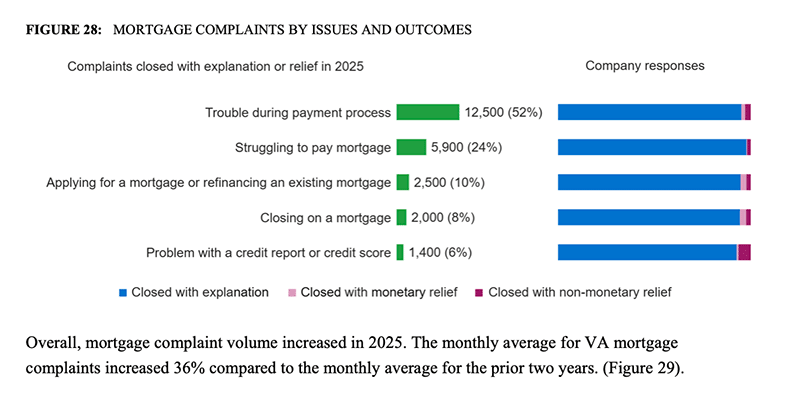

Mortgage Complaint Excerpts

The CFPB received approximately 30,400 mortgage complaints in 2025. It sent 25,300 (83%) of these complaints to companies for review and response, referred 12% to other regulatory agencies, and found 4% to be not actionable. As of March 2, 2026, 0.06% of mortgage complaints were pending with the consumer and 0.6% were pending with the CFPB.

Companies responded to 98% of mortgage complaints sent to them for review and response. In 92% of these complaints, consumers reported first attempting to resolve their issue with the company. Companies closed 91% of complaints with an explanation, 2% with monetary relief, and 3% with non-monetary relief. They provided an administrative response for 3% of complaints and did not provide a timely response for 1% of complaints. As of March 2, 2026, 0.2% of complaints were pending review by the company.

When submitting mortgage complaints, consumers specify the type of mortgage. In 2025, conventional home mortgages were the most complained about mortgage type.

Consumers frequently reported that representatives were unresponsive during purchase, refinance, and assumption processing. Some consumers indicated that lack of communication from companies increased frustration and led to closing delays.

They expressed disappointment about a lack of clarity and transparency throughout the loan application process, along with receiving misleading information from company representatives. Some also expressed dissatisfaction about unwelcome solicitation calls, and practices perceived as deceptive from companies. Companies typically responded that consumer experiences in complaints involved miscommunication. They sometimes refunded fees associated with loan applications. At times, they apologized for the unsatisfactory customer service experience or confusion created by company representatives.

Consumers continued to report lengthy loan application processing times and challenges dealing with unresponsive loan officers, processors, and companies. They also expressed frustration with extensive and repeated document requests, settlement delays, and closings that did not occur.

Company representatives were reportedly difficult to reach for questions and process updates. Companies sometimes acknowledged delayed processing due to loan officer errors and miscommunication. In other complaints, they attributed delays to loan programs or other unanticipated complexities that became evident during loan processing or underwriting. Companies often apologized for processing, closing, and other service delays. Consumers expressed dissatisfaction about unexpected changes to loan terms. They were concerned about receiving multiple closing disclosures with different terms than originally discussed or disclosed in loan estimates. Consumers also said loan originators verbally promised interest rates and then increased them in written disclosures.

Some consumers thought their interest rates were locked and were surprised about rate increases during the loan application process. Companies told consumers that certain charges and fees could change even after locking the interest rate if adjustments were within allowable limits. They sometimes adjusted the interest rate in favor of consumers, or attributed changes to rate lock expirations, or insisted the changes were appropriate.

Consumers also expressed frustration when lenders denied their applications, especially after they provided extensive documentation or paid appraisal fees after having received assurances that they were qualified and when denials occurred late in the process. Many expressed concerns about not being provided with clear denial reasons. Some disputed appraisal valuations or reported not receiving proper adverse action notices. Companies generally responded that loan denials were appropriate based on investor guidelines. Some companies provided the consumer a copy of the adverse action notice. In response to concerns about an initial approval by loan officers followed by a denial, companies responded that final loan approvals were dependent upon underwriter review of documentation to verify income, assets, liabilities, credit history, and other information.

Tip of the Week: Sign up for 2026 CE

This is the 250th issue of the Loan Officer School Journal! Yay. :0) To celebrate, enjoy our gift to you!

Promo Code “newsletter”

Expanding your product offerings is an effective way to enhance your business’s vitality. This year, the Loan Officer School is surveying non-Qualified Mortgage (non-QM) financing options. We will review the various types of underwriting required for non-QM financing, including higher-priced mortgage loans (HPML), balloon-payment features, and interest-only options.

Presenting non-QM solutions to consumers improperly can lead to serious consequences. Understand the essentials of compliant and ethical subprime mortgage origination. Attend the Loan Officer School 2026 continuing education classes.

Please use the promo code “newsletter” when you sign up.

Have a Question About Operations, Sales, Marketing, or Compliance? Email Your Questions to the Loan Officer School Journal.

We invite LOSJ readers to submit questions on any topic to the editor. Topics can include compliance, sales, marketing, implementation, and other areas that may be helpful to our customers. If we use your question, we will include only your first name in our response. Please send your questions to: losjmailbag@gmail.com.

Necessary Mailbag Disclosure: The LOSJ is a periodic publication from LoanOfficerSchool.com designed to educate and inform our readers. Please note that we do not provide legal advice, and nothing in the LOSJ should be construed as a legal opinion on specific facts or circumstances. The content serves strictly for informational purposes. We strongly advise readers to consult legal counsel regarding any legal matters or specific questions.