Why Haven’t Loan Officers Been Told These Facts?

State Regulators Demand Mortgage Loan Originators (MLOs) Provide Diligent Assistance to Applicants

The company failed to act with reasonable due diligence to complete the application in violation of Regulation B § 1002.2(f).

Don’t let this be you.

Recently, lenders have been facing scrutiny from state regulators regarding a lesser-known type of violation under the Equal Credit Opportunity Act (ECOA). This involves a rule that 99.9% of mortgage originators have probably never heard of.

The examiner stated, “MLOs gathered application information, including credit reports, to assess applicants’ creditworthiness; however, they failed to exercise reasonable diligence in obtaining additional information necessary to complete the application.”

Examiners stated that Licensee records fail to document the actions taken to complete the application.

To complete the complaint, the examiner stated that “the Licensee did not provide evidence of sending a notice of incompleteness or a notification of adverse action regarding incomplete applications.”

One issue is that MLOs often lack a clear understanding of the boundaries defining an application under ECOA. As a result, applications may occur without the MLO’s awareness and, worse, without the sponsoring lender’s knowledge.

Every so often, the states publish their top-10 lists of state-licensed mortgage violations. This year’s list differs from past lists. The top four violations are all ECOA exceptions.

Examiners are like sport fishermen (is it okay to use that word now, or should we stick with fisherperson?). Until the industry cleans up its act, regulators should keep going where the fishing is good. Secondly, for examiners, it’s a bonus if you catch a repeat offender: the licensee violated the same thing you cited them for in the last exam.

Out of this year’s top ten list, the second most frequent violation identified by state examiners concerns serious Regulation B violations currently under scrutiny.

Official Regulation B Commentary On The Diligence Requirement

12 CFR § 1002.2(f)Application means an oral or written request for an extension of credit that is made in accordance with procedures used by a creditor for the type of credit requested. The term application does not include the use of an account or line of credit to obtain an amount of credit that is within a previously established credit limit. A completed application means an application in connection with which a creditor has received all the information that the creditor regularly obtains and considers in evaluating applications for the amount and type of credit requested (including, but not limited to, credit reports, any additional information requested from the applicant, and any approvals or reports by governmental agencies or other persons that are necessary to guarantee, insure, or provide security for the credit or collateral). The creditor shall exercise reasonable diligence in obtaining such information.

Comment 2(f)-6. Completed application – diligence requirement. The regulation defines a completed application in terms that give a creditor the latitude to establish its own information requirements. Nevertheless, the creditor must act with reasonable diligence to collect information needed to complete the application. For example, the creditor should request information from third parties, such as a credit report, promptly after receiving the application. If additional information is needed from the applicant, such as an address or a telephone number to verify employment, the creditor should contact the applicant promptly. (But see comment 9(a)(1)-3, which discusses the creditor’s option to deny an application on the basis of incompleteness.)

Absent a Notice of Incompleteness or Adverse action in the record, if determined that the lender had an application under Regulation B, a covered person a serious issue. Especially when the examiner is responding to a discrimination complaint.

It is the lender’s prerogative to deny the application for incompleteness, provided diligent effort has been made to complete it.

Official Regulation B Commentary On Denial for Incompleteness

Comment 9(a)(1)-3. Incomplete application – denial for incompleteness. When an application is incomplete regarding information that the applicant can provide and the creditor lacks sufficient data for a credit decision, the creditor may deny the application giving as the reason for denial that the application is incomplete. The creditor has the option, alternatively, of providing a notice of incompleteness under § 1002.9(c).

To deny an application for incompleteness, the lender must demonstrate diligence in completing the application. Without a Notice of Incompleteness in the record, lenders denying a loan for incompleteness are relying on often incomplete or immaterial loan notes.

The other path, withdrawn applications, the Official Regulation B commentary states, “Comment 9(_)-2. Expressly withdrawn applications. When an applicant expressly withdraws a credit application, the creditor is not required to comply with the notification requirements under § 1002.9. (The creditor must comply, however, with the record retention requirements of the regulation.”

Ensure you have evidence that the applicant withdrew their application. Again, the best way to accomplish this is with the Notice of Incompleteness.

12 § 1002.9(c)(2) Notice of incompleteness. If additional information is needed from an applicant, the creditor shall send a written notice to the applicant specifying the information needed, designating a reasonable period of time for the applicant to provide the information, and informing the applicant that failure to provide the information requested will result in no further consideration being given to the application. The creditor shall have no further obligation under this section if the applicant fails to respond within the designated time period. If the applicant supplies the requested information within the designated time period, the creditor shall take action on the application and notify the applicant in accordance with paragraph (a) of this section (Notice requirements).

Learn how states are increasing examination and enforcement actions against licensees in light of reduced federal oversight.

Signup here: LOAN OFFICER SCHOOL 2026 CE

Use promo code “newsletter”

For more information, see the LOSJ issue links below:

BEHIND THE SCENES: NMLS CHANGES CREATE GREATER EFFICIENCIES FOR STATE-LICENSED INDIVIDUALS AND COMPANIES

The CSBS recently published a blog post highlighting changes for licensees during licensure renewal. It’s important not to delay your 2027 renewal requirements. To stay ahead, consider enrolling in the Loan Officer School Continuing Education (CE) classes this summer to get a jump on your 2027 license requirements.

Please note that the changes affect individual licensees, companies, and control persons. MU1, MU2, MU3 and MU4 filings impacted.

Signup here: LOAN OFFICER SCHOOL 2026 CE

Use promo code “newsletter”

Excerpted From CSBS May 6, 2026 Blog

NMLS remains vital for nearly 600,000 industry users across the financial services sector. For mortgage loan originators (MLOs) and mortgage companies, obtaining an NMLS ID and becoming licensed is a symbol of trust and professional integrity for existing and prospective customers. So, when key system updates occur it is important that NMLS users comply.

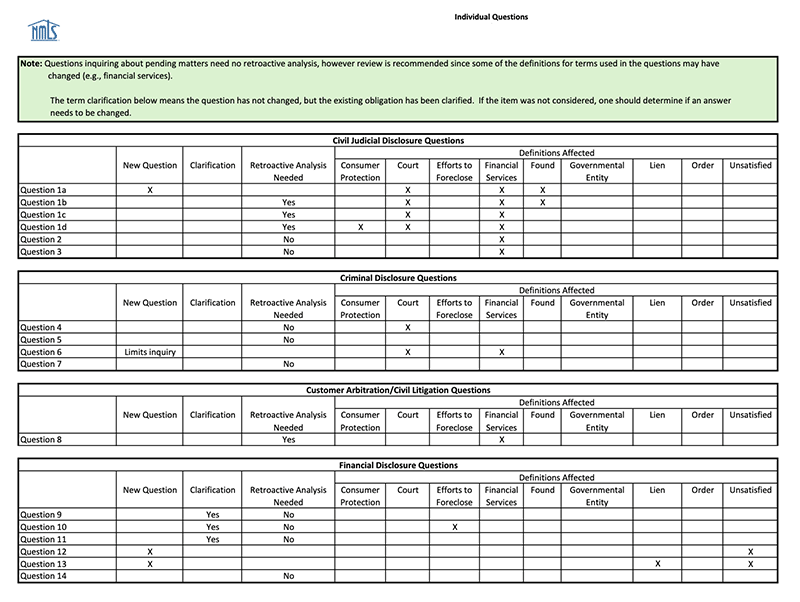

On April 18, NMLS was enhanced to reflect a policy change for disclosure questions and a better way to manage employment relationships in the system. These system changes align with ongoing efforts to improve the NMLS user experience and are in response to user feedback over time.

Here is an overview of the NMLS changes and how they impact MLOs, mortgage companies, and other state-licensed financial services professionals:

Disclosure Questions

This change requires all individuals, including MLOs, who file the MU4 or MU2 Forms as part of the licensing process to update their form in NMLS by completing the updated disclosure questions.

It is important that individuals impacted by this change review and complete updates by Aug. 31 to prepare for the 2027 NMLS annual renewal period. Failure to do so may delay filings or result in compliance issues during renewal.

Key Changes:

- Clearer and updated questions.

- Reorganized structure to make it easier for you to provide responses.

- Updated requirements for criminal, regulatory, and financial disclosures.

Visit the Disclosure Questions Update page of the NMLS Resource Center for more information.

Employment Reporting History

Prior to April 18, individuals filled out their own employment history in NMLS when completing individual forms (MU4, MU2 and MU4R). However, as of April 18 an MLO’s relationship with a company in NMLS will automatically populate the Employment History section of all individual forms (MU4, MU2 and MU4R) in the system. This means individuals will no longer complete this information themselves.

This change:

- Allows employment information to be captured once and reused, rather than being re-entered and maintained separately by individuals and companies.

- Addresses long-standing pain points including duplicate data entry, conflicting employment records, and confusion about who is responsible for updating employment information.

As a result of the employment reporting history enhancement in NMLS, company users will be required to enter the following information when completing Company Relationship information for individuals:

- Position/Title

- Work Phone

- Work Email

Helpful NAMB/NMLS Video (FF to 6:45 to past intros)

Tip of the Week: Sign up for 2026 CE

The LOSJ is celebrating five years of exceptional service to the mortgage industry, offering insights you won’t find anywhere else. To celebrate, enjoy our gift to you! Use the promo code “newsletter” when placing your class order.

Expanding your product offerings is an effective way to enhance your business’s vitality. This year, the Loan Officer School is surveying non-Qualified Mortgage (non-QM) financing options. We will review the various types of underwriting required for non-QM financing, including higher-priced mortgage loans (HPML), balloon-payment features, and interest-only options.

Presenting non-QM solutions to consumers improperly can lead to serious consequences. Understand the essentials of compliant and ethical subprime mortgage origination. Attend the Loan Officer School 2026 continuing education classes.

Please use the promo code “newsletter” when you sign up.

Have a Question About Operations, Sales, Marketing, or Compliance? Email Your Questions to the Loan Officer School Journal.

We invite LOSJ readers to submit questions on any topic to the editor. Topics can include compliance, sales, marketing, implementation, and other areas that may be helpful to our customers. If we use your question, we will include only your first name in our response. Please send your questions to: losjmailbag@gmail.com.

Necessary Mailbag Disclosure: The LOSJ is a periodic publication from LoanOfficerSchool.com designed to educate and inform our readers. Please note that we do not provide legal advice, and nothing in the LOSJ should be construed as a legal opinion on specific facts or circumstances. The content serves strictly for informational purposes. We strongly advise readers to consult legal counsel regarding any legal matters or specific questions.