Why Haven’t Loan Officers Been Told These Facts?

The Hidden Drivers of Homeowners Insurance Costs

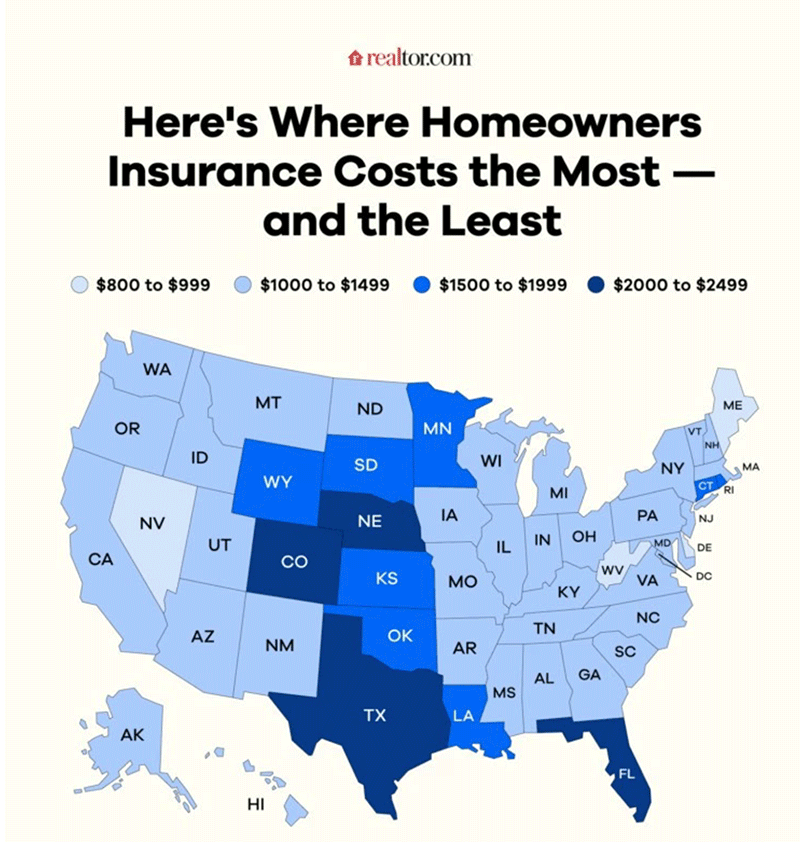

Homeowners insurance costs have recently become a significant concern, and rightly so. While inflation in replacement costs, climate change, and issues like mold often make the headlines, insurance costs are influenced by more factors than just these general circumstances.

Unknown to many homebuyers and their loan officers, a weak credit history or a history of claims can lead to significantly higher homeowners insurance costs.

Consider this: in a NerdWallet analysis, those with good credit typically pay, on average, about $2,490 annually for homeowners’ insurance. However, in many states, someone with poor credit faces an average premium of $4,290 per year—an astonishing difference of over 72%.

Insurance companies, akin to portfolio lenders, exhibit varying degrees of risk tolerance. For those companies that strive to minimize the risks associated with underwriting more precarious transactions, it is common to impose a premium that significantly exceeds that of less risk-averse insurers. It is essential for mortgage professionals to understand this dynamic and to provide appropriate guidance to affected applicants.

In addition to credit impacts on pricing, the applicant’s claims history or even a claims history on the subject property can significantly increase premiums. Insurance companies have a variety of databases available to assist in risk management. Lexis/Nexis, one of the nation’s biggest consumer reporting agencies, provides the “Comprehensive Loss Underwriting Exchange (CLUE)” for insurance underwriters. Lexis/Nexis operates as a national consumer reporting agency and is therefore required to disclose any consumer data it possesses to the affected individuals once annually, similar to the provision of free credit reports. When looking for a house, it can be helpful for buyers to review their CLUE record.

An insurance provider may request a Comprehensive Loss Underwriting Exchange (CLUE) report when an individual applies for coverage or solicits a quote. This report contains the applicant’s claims history and/or the claims history associated with a particular property, which the insurance company utilizes to determine whether to extend coverage and to establish the associated premium rates.

Studies conducted by insurance companies demonstrate a significant correlation between previous claims and the likelihood of future claims submitted by the insured. The database includes information about any applicant claims over the past seven years, as well as claims on the subject property.

Every loan officer requires a team of experts. Forward this LOSJ article to an insurance agent and ask for their comments. Keep in mind that a handful of states limit insurers’ use of credit history in underwriting. Your agent will know this, too. Here are a few questions MLOs might want to consider:

- How can ABC Insurance Brokers help clients lower their insurance costs, particularly for those considered higher risk?

- Can you direct consumers to an insurer that offers competitive coverage for higher-risk applicants?

- Can ABC Insurance collaborate with an applicant to enhance their risk profile if given adequate lead time?

Nerdwallet Insurance Cost Article

Housing Data Courtesy of the FHFA

Chart Courtesy of Realtor.com ®

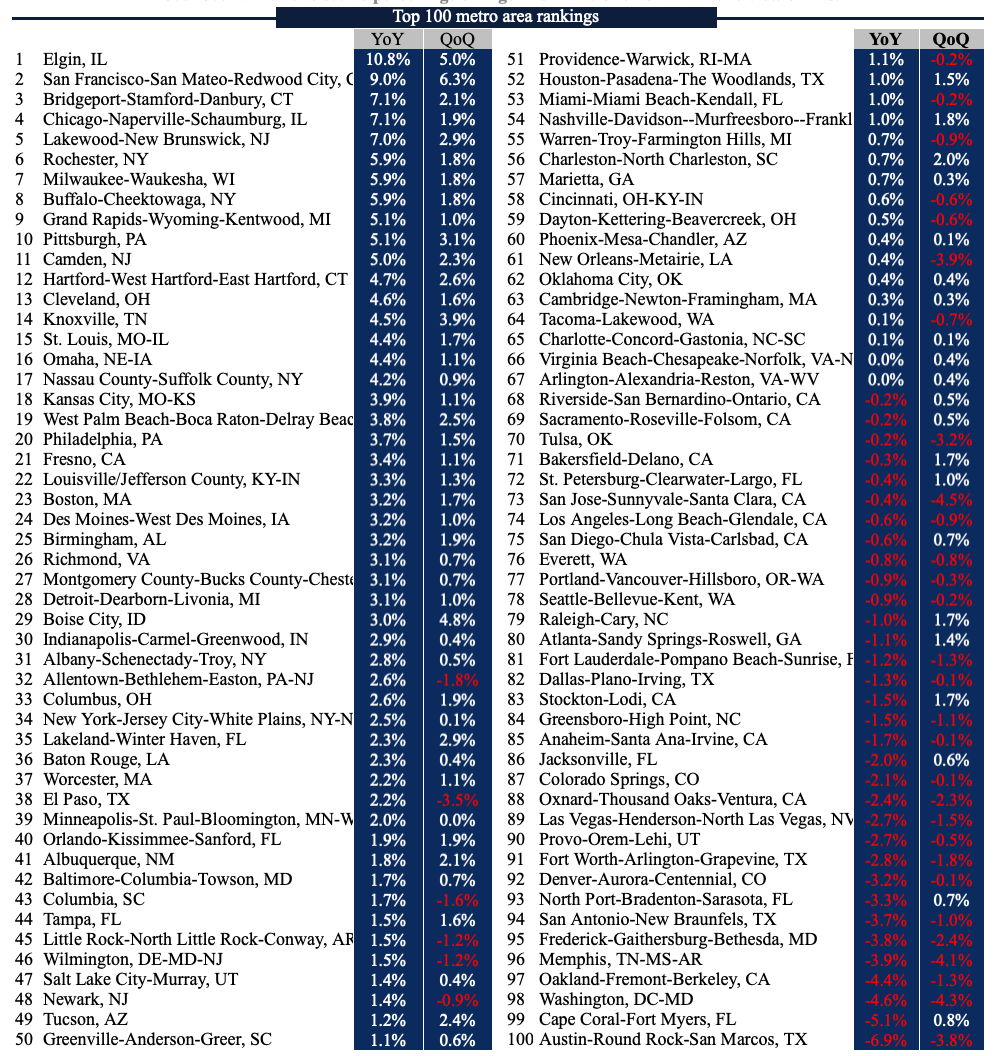

BEHIND THE SCENES: DATA INDICATES CONTINUED BUT UNEVEN MARKET SOFTENING; NEW CONSTRUCTION AND CONDOS LEADING PRICE DROPS

Pricing in the housing market remains highly localized and stratified. The concept of softening markets can no longer be defined solely by geographic location or the distinction between luxury and starter homes. In the same market where condos are experiencing extreme downward pressures, detached single-family homes are still performing well. What does this mean in terms of market price direction? In summary, the housing market operates similarly to any other; pricing is determined by supply and demand. Currently, we are observing changes in demand that may, in turn, lead to an increase in supply. Interest rates are relatively low compared to historical averages. However, new factors continue to affect typical market drivers. The primary factors hindering demand are not solely interest rates, but rather a combination of several challenges that create a storm of price headwinds.

For starters, the price run-up since the pandemic far exceeded any commensurate wage increase in most markets. Stagnant wages, coupled with significantly higher insurance costs and association dues, mean that many markets still provide scant affordable entry-level offerings.

There are increasing wage exceptions. For example, the San Francisco/Silicon Valley area is now seeing wage pressures and pricing resurgence largely due to the explosion in demand for artificial intelligence.

Yet, on balance, we are witnessing a return to more typical market forces. There is no federal consumer stimulus anticipated in the near future, and the last of the COVID loan-servicing bailouts has largely ended. What about these more novel market factors? No doubt that several new factors are contributing to the ongoing supply-side issues. The lock-in effect continues to suppress normal selling activity, and entrenched remote workers present another unique dimension. The impact of these two factors on the transition to a more balanced market is still uncertain. One could view the new factors as having a “braking effect” on the market’s recovery.

Report Highlights Excerpted From Recent Realtor.com Report

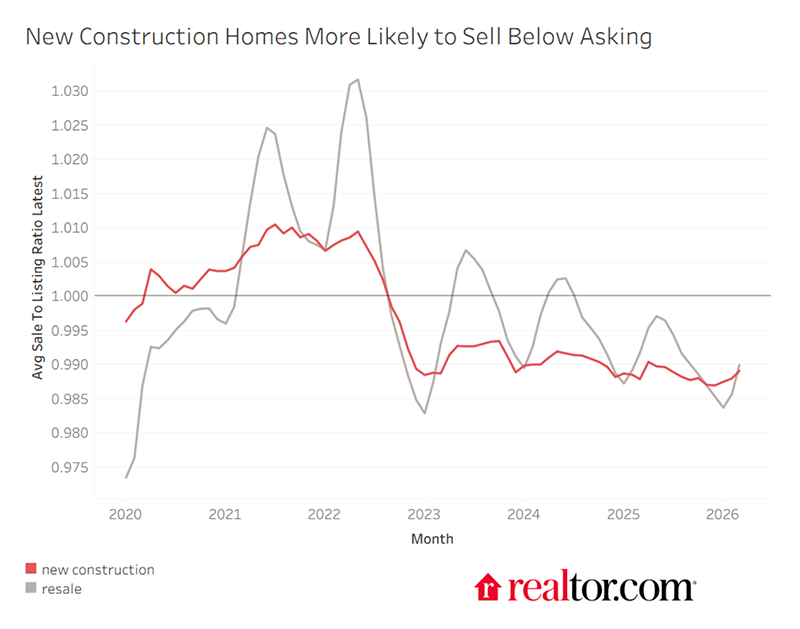

- During the post-pandemic buying frenzy, homes sold for well above asking price on average. In the years since, they are selling for less than asking price on average as buyers consolidate more negotiating power.

- New construction is more likely to sell for below asking price than existing homes, and condos and townhomes are more likely to sell for below asking price than single-family homes.

- Four weeks into a listing being on the market (measured from initial listing to close) is when it has the highest sale-to-listing price ratio, on average. Four weeks into a listing being on the market is also when it is most likely to offer a price reduction. Initial pricing is the difference between a bidding war and a price cut four weeks later.

Spec homes and condo market collapses. That is hardly novel and is reminiscent of the savings-and-loan debacle of the 1980s. The federal government has been implementing measures to relax prudential risk management regulations for depository institutions. This adjustment allows lenders to sustain their working capital while contending with an increase in loan performance issues. The underlying objective of this initiative is to stimulate lending and enhance consumer spending. However, a potential risk of this approach is that it may lead to more lenders experiencing loan performance difficulties.

See the full report on the housing market at the link below:

Tip of the Week: Sign up for 2026 CE

The LOSJ is celebrating five years of exceptional service to the mortgage industry, offering insights you won’t find anywhere else. To celebrate, enjoy our gift to you! Use the promo code “newsletter” when placing your class order.

Expanding your product offerings is an effective way to enhance your business’s vitality. This year, the Loan Officer School is surveying non-Qualified Mortgage (non-QM) financing options. We will review the various types of underwriting required for non-QM financing, including higher-priced mortgage loans (HPML), balloon-payment features, and interest-only options.

Presenting non-QM solutions to consumers improperly can lead to serious consequences. Understand the essentials of compliant and ethical subprime mortgage origination. Attend the Loan Officer School 2026 continuing education classes.

Please use the promo code “newsletter” when you sign up.

Have a Question About Operations, Sales, Marketing, or Compliance? Email Your Questions to the Loan Officer School Journal.

We invite LOSJ readers to submit questions on any topic to the editor. Topics can include compliance, sales, marketing, implementation, and other areas that may be helpful to our customers. If we use your question, we will include only your first name in our response. Please send your questions to: losjmailbag@gmail.com.

Necessary Mailbag Disclosure: The LOSJ is a periodic publication from LoanOfficerSchool.com designed to educate and inform our readers. Please note that we do not provide legal advice, and nothing in the LOSJ should be construed as a legal opinion on specific facts or circumstances. The content serves strictly for informational purposes. We strongly advise readers to consult legal counsel regarding any legal matters or specific questions.