Why Haven’t Loan Officers Been Told These Facts?

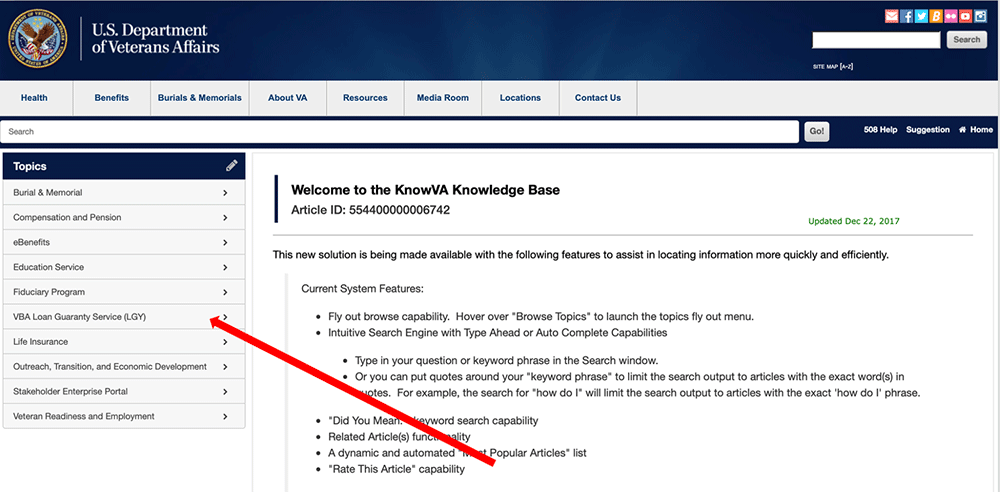

Accessing the VAP26-07 Lender’s Handbook

If you are looking for the VA Lenders Handbook, it is no longer available on the VA Home Loan Lender Page. The VA is currently updating its database, and some LGY documents are now accessible only through the new portal.

To access the VA Lenders Handbook, please follow the steps outlined below.

Select VBA Loan Guaranty Service(LGY) hover menu

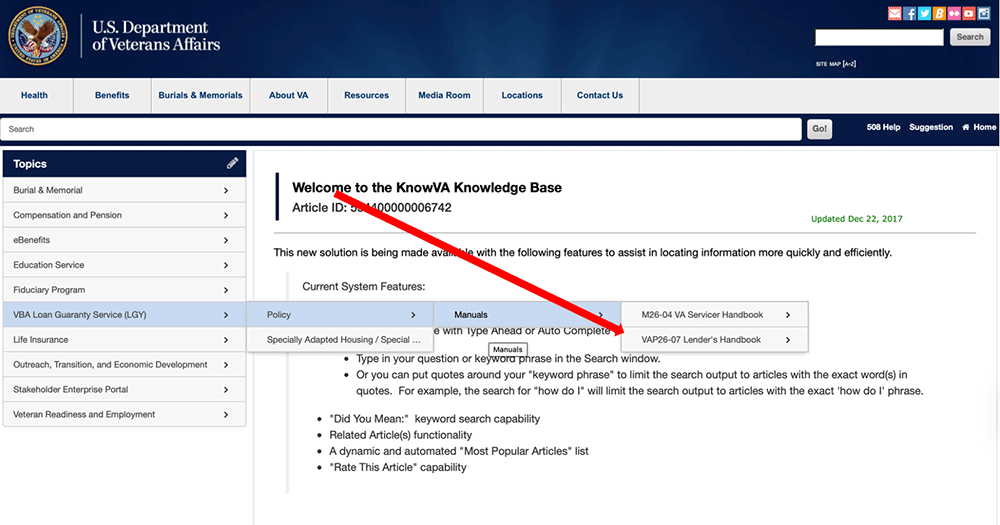

Select Policy hover menu

Select Manuals hover menu

Select VAP26-07 Lenders Handbook hover menu

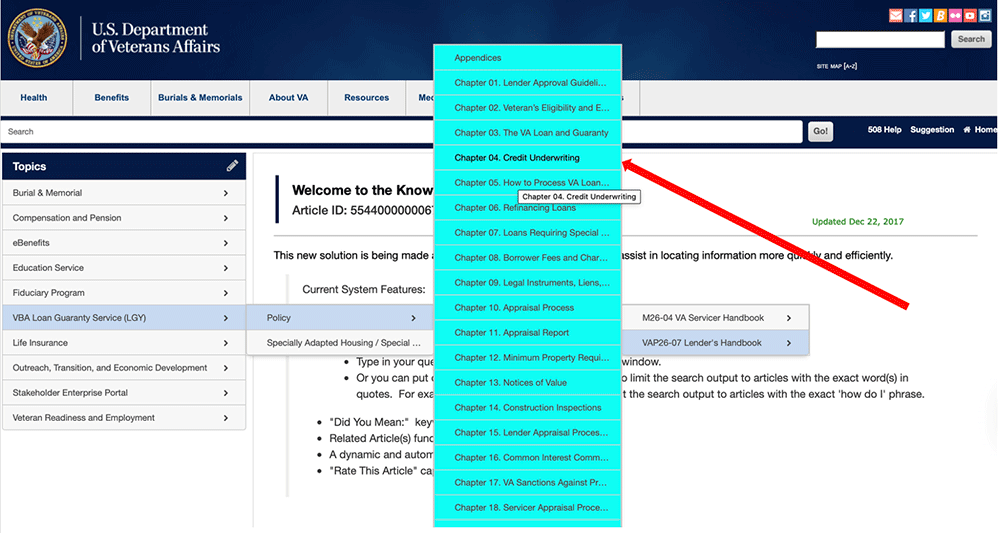

Select Chapter

BEHIND THE SCENES: Court Dismisses Fair Lending Class Action Lawsuit against Mortgage Giant

In summary, the Court dismissed the case on the grounds of insufficient evidence. The inherent complexity of a class action lawsuit tends to elevate the evidentiary requirements. Furthermore, the Court did not consider statistical disparity a sufficient basis for establishing the complaint’s violations.

Excerpted from ClassAction.Org

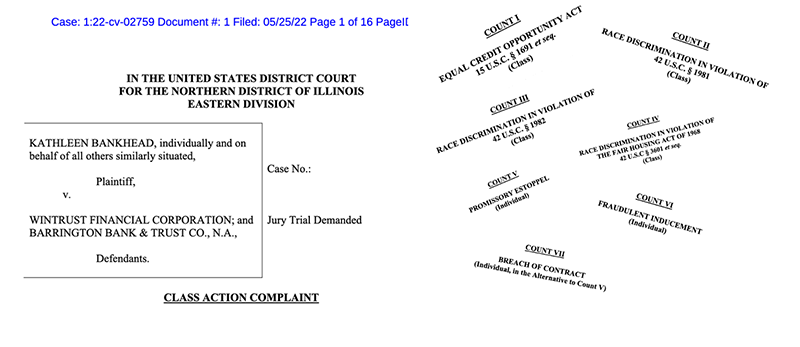

The plaintiff, an African American Illinois resident, alleges in the 16-page complaint that Wintrust, a Chicagoland financial firm, applies residential mortgage policies and practices that “intentionally and disproportionately” discriminate against and harm Black and African American customers. For example, the lawsuit claims Wintrust’s practices for determining customers’ eligibility for home loans, rates, terms and conditions impose high costs and fees on Black and/or African American borrowers, while providing these same consumers with low credits.

The suit charges that Wintrust has “created artificial, arbitrary, and unnecessary barriers to fair housing opportunities” for Black and/or African American consumers.

Per the complaint, these practices result in racial redlining—the denial of mortgages and home-buying options to Black and/or African American consumers—and reverse redlining—the practice of extending “predatory credit” to Black and/or African American borrowers on less favorable terms and with higher interest rates, costs and fees.

“As a result of Wintrust’s uniform, nationwide policies and practices related to mortgage approvals, interest rate determinations, fees, and costs, Wintrust approves white applicants for home purchase mortgage loans at substantially higher rates than Black and/or African American applicants,” the suit alleges.

The complaint says that Wintrust in 2020, according to an analysis of nationwide data published under the Home Mortgage Disclosure Act, originated loans to roughly 73 percent of white borrowers who applied for a home purchase through the firm, compared to a little more than 59 percent of Black and/or African American applicants.

Further, the case alleges Wintrust is “substantially more likely” to deny Black and/or African American consumers’ applications for home purchase loans outright. When Wintrust does approve a Black or African American customer’s home purchase loan application, the suit alleges, it does so on “substantially worse terms” than those offered to non-Black and non-African American borrowers.

“In sum, Wintrust disproportionately refuses to lend to Black and/or African Americans,” the lawsuit alleges. “But when it does, it charges Black and/or African American borrowers more costs and fees for less credit on worse terms than non-Black, non-African American borrowers, disproportionately excludes Black and/or African American borrowers from refinancing their higher-interest loans, and even when it allows them to refinance, charges them higher costs and fees.”

The lawsuit looks to represent all Black and/or African American consumers who applied for and/or received credit related to residential real estate from Wintrust or Wintrust Mortgage.

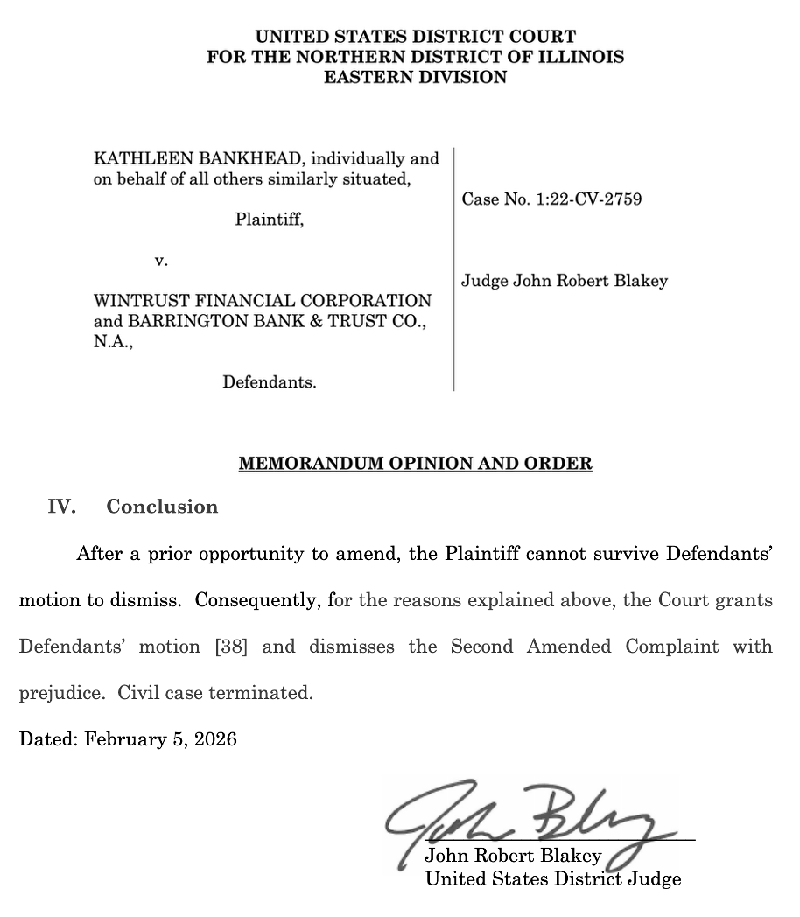

UNITED STATES DISTRICT COURT

FOR THE NORTHERN DISTRICT OF ILLINOIS

EASTERN DIVISION

February 6, 2026

Excerpted from the Court’s Memorandum Opinion and Order

ALLEGATIONS

Plaintiff is an African American woman and well-qualified home borrower. In 2020, she began communicating with a Wintrust loan originator to obtain a mortgage loan “with the lowest rate and most favorable terms in connection with her purchase of residential real estate in Bronzeville, a majority-Black neighborhood in Chicago.” Plaintiff’s loan officer wrote to her in March 2020 that “Wintrust would provide her with the ‘best structure and rates.’” Wintrust also told Plaintiff it would offer her a “float down” at no charge, which would provide Plaintiff a lower interest rate if market rates decreased. Despite those representations, Plaintiff alleges that because of her race and because she was purchasing property in a majority-Black neighborhood, Wintrust “had no intention” of providing her the best rate or a free float down.

Instead, Wintrust “refused to provide Plaintiff a ‘float down’ option” and offered her a “higher interest rate with less favorable terms and conditions.” Plaintiff claims that Wintrust has “policies and practices” governing home loans and refinancing, and those policies “intentionally and disproportionately discriminate against and harm Black and/or African American customers.” As a result, she alleges that she, and other Black and/or African American borrowers, have been injured by “Wintrust’s racially discriminatory residential mortgage lending policies and practices.”

Plaintiff claims that Wintrust has “policies and practices” governing home loans and refinancing, and those policies “intentionally and disproportionately discriminate against and harm Black and/or African American customers.” As a result, she alleges that she, and other Black and/or African American borrowers, have been injured by “Wintrust’s racially discriminatory residential mortgage lending policies and practices.”

Regarding Wintrust’s “policies or practices,” the SAC alleges that Wintrust employs Fannie Mae’s Desktop Underwriter program “which provides information to lenders on a mortgage loan’s eligibility for future sale to Fannie Mae.” Wintrust also maintains its own “‘proprietary’ policies and practices to set rates,costs, and fees.” Under these policies and practices, “Wintrust alone makes the decision whether to extend credit and on what terms.” Thus, “the fact that an applicant is approved under Desktop Underwriter does not guarantee that Wintrust will approve the loan.”

To support her discrimination claims, Plaintiff again relies upon nationwide data that Wintrust reported pursuant to the Home Mortgage Disclosure Act in 2020. For example, Plaintiff states that in 2020, Wintrust “originated loans to approximately 80% of white borrowers who applied for a home purchase mortgage through Wintrust Mortgage, compared to only 65% of Black and/or African American applicants.” Wintrust’s Black and/or African American borrowers nationwide also spent “approximately 3.3% of their Wintrust Mortgage loan value on costs and fees, versus 2.9% for white borrowers.” As for refinancing, from 2018–2022, Plaintiff alleges a statistically significant racial disparity in Wintrust’s granting of refinance mortgage applications between white and Black borrowers “after controlling for debt-to-income ratio, loan amount, income, property value, loan-to-value ratio, loan term, and year of application.”

Based upon these disparities, Plaintiff brings race discrimination claims under four federal statutes: the Equal Credit Opportunity Act (Count I), 42 U.S.C. § 1981 (Count II), 42 U.S.C. § 1982 (Count III), [Counts II and III are alleged civil rights violations] and the Fair Housing Act (Count IV).

Theories of Liability

Plaintiff asserts two theories of liability premised upon Defendant’s alleged discrimination: disparate treatment (or intentional discrimination), and disparate impact. Plaintiff brings all four counts under a theory of disparate treatment and brings only Counts I and IV under the additional theory of disparate impact.

Disparate Treatment

The Court did not hold in its prior order, that Plaintiff’s disparate treatment claims here require extensive factual pleadings. Rather, this Court merely stated—as Plaintiff concedes, that her

alleged theory is more complicated than, for example, a claim that an individual loan officer or officers discriminated against Plaintiff, an individual, in her mortgage loan application. Here, Plaintiff’s claims involve “class pattern-and-practice” allegations that Wintrust maintains uniform policies and practices governing mortgage loans and refinancing that systemically discriminate against African American and/or Black applicants. Therefore, more factual allegations are required to render Plaintiff’s claims plausible under the Twombly/Iqbal standard [The “degree of specificity” required establishing plausibility “rises with the complexity of the claim”].

Here, Plaintiff does not allege, even in the alternative, a straightforward individual claim based upon an individual loan officer’s animus toward Plaintiff because of her race. Rather, she alleges that Defendants maintained a set of “uniform, discriminatory mortgage loan origination and underwriting practices and engaged in a pattern or practice of systemic race discrimination against Black and/or African American mortgage loan and refinancing applicants and recipients that constitutes illegal intentional discrimination.” Thus, Plaintiff must plead more detailed factual allegations to render her claims of uniform policies of systemic and intentional race discrimination plausible.

Turning to the sufficiency of the allegations, the [complaint] fell far short in plausibly alleging intentional discrimination because it alleged that Wintrust’s policies “include the potential for loan officers to exercise discretion in setting rates, costs, and fees,” but included no allegations of discriminatory animus in the officers’ exercise of such discretion. Again, it fails to provide any allegations suggesting discriminatory animus in the use of that discretion. The only factual allegation Plaintiff adds this time, to purportedly suggest an intent to discriminate, is a delegation of the discretion to set costs, fees, and rates, that is assigned to “largely non-Black loan personnel.” This addition does nothing to advance the ball; the mere fact that many of Wintrust’s loan officers happen to be non-Black cannot, without more, render plausible Plaintiff’s claims that Wintrust maintains practices and policies that systemically and intentionally discriminate against African American and/or Black loan applicants.

Opposing dismissal, Plaintiff merely recites statistics demonstrating that Wintrust generally approves loans for Black and/or African American borrowers at lower rates and with worse terms than it does for white borrowers. But Plaintiff again fails to connect this disparate outcome to Defendants’ intent. Accordingly, Plaintiff’s allegations remain insufficient to state a claim of intentional discrimination under the ECOA, § 1981, or the FHA [42 USC §1981. Equal rights under the law (a) Statement of equal rights. All persons within the jurisdiction of the United States shall have the same right in every State and Territory to make and enforce contracts, to sue, be parties, give evidence, and to the full and equal benefit of all laws and proceedings for the security of persons and property as is enjoyed by white citizens, and shall be subject to like punishment, pains, penalties, taxes, licenses, and exactions of every kind, and to no other.].

Disparate Impact

The Court next considers Plaintiff’s allegations of disparate impact discrimination alleged in Counts I (ECOA) and IV (FHA). To plead a disparate impact claim under the FHA, Plaintiff must allege: (1) a statistical disparity; (2) that the defendant maintained a specific policy; and (3) such policy caused the disparity.

This Court previously dismissed the disparate impact claims in the [complaint] because Plaintiff failed to plausibly allege any connection between a specific policy of Defendants’ and any identified disparities, let alone facts to satisfy the “robust causality requirement.”

As this Court explained in its prior order, causation may be satisfied at the pleading stage when the complaint’s allegations contain sufficient details about the policy at issue to infer causation, but Plaintiff has not provided any details about Wintrust’s policies or practices, only generally alleged “categories of policies.” This Court did not hold that statistics indicating racial disparities, even after controlling for certain objective criteria, would suffice to state a disparate impact treatment claim. Among other things, such a holding would have directly contravened binding precedent.

The Court recognized the theory of disparate impact liability under the FHA, but stated that such liability is “properly limited in key respects,” including that it should not be “imposed based solely on a showing of a statistical disparity,” and that the challenged policy must also be “artificial, arbitrary, and unnecessary. Therefore, the Court explained, “a disparate-impact claim that relies on a statistical disparity must fail if the plaintiff cannot point to a defendant’s policy or policies causing that disparity.” Here, Plaintiff does just that; she relies exclusively on statistics depicting disparities between white and Black applicants for mortgage and refinancing approvals, controlling for six other factors. These statistics alone, do not give rise to the reasonable inference that any particular practice or policy of Defendants has caused that disparity such that Defendants can be held liable under the statute.

In sum, to survive dismissal, the complaint’s allegations must connect the alleged statistical disparities between Black and non-Black applicants to specific policies or practices of the Defendants that remain “artificial, arbitrary, and unnecessary” under the law. Plaintiff fails to do so, and this failure is fatal. The Court therefore dismisses Counts I and IV.

Tip of the Week – Have a Question About Operations, Sales, Marketing, or Compliance? Email Your Questions to the Loan Officer School Journal.

We invite LOSJ readers to submit questions on any topic to the editor. Topics can include compliance, sales, marketing, implementation, and other areas that may be helpful to our customers. If we use your question, we will include only your first name in our response. Please send your questions to: losjmailbag@gmail.com.

Necessary Mailbag Disclosure: The LOSJ is a periodic publication from LoanOfficerSchool.com designed to educate and inform our readers. Please note that we do not provide legal advice, and nothing in the LOSJ should be construed as a legal opinion on specific facts or circumstances. The content serves strictly for informational purposes. We strongly advise readers to consult legal counsel regarding any legal matters or specific questions.