Why Haven’t Loan Officers Been Told These Facts?

How to Qualify Military Allowances, Overtime, or Short Employment History

The VA loan program gives lenders significant discretion in underwriting. Generally, lenders can effectively utilize the VA’s flexible underwriting enhancements when it is reasonable to do so. However, in cases with additional risk factors, lenders must proceed with caution.

Consider the situation of a homemaker who has recently reentered the workforce. The applicants had two car loans, each with less than 18 months left until they would be paid off. The total monthly payments for these loans amounted to just over $1,600.

Although the co-borrower had less than 2 years of employment history, she had 14 months with her current employer. If there had been additional risk factors, the underwriter would have declined the loan due to insufficient income [failed to meet minimum residual income per VA guidelines]. However, the lender approved the application and funded the loan.

LGY selected the loan for a full-file review. On its face, the problem identified was that when the examiner calculated the residual analysis, the applicants were substantially short of the minimum. However, the lender’s loan analysis was exemplary. The lender correctly excluded the co-borrower’s earnings from the effective income. Yet the lender correctly reasoned that, under VAP 26-7 Chapter 4 Subtitle f, the co-borrower’s income sufficiently offset the two auto loans, permitting exclusion from the residual income calculation.

Additionally, the lender explained that the co-borrower’s lack of employment history stemmed from her being a homemaker until the applicants’ children left for college. The lender provided tax returns and proof of school attendance as evidence. They also highlighted that the co-borrower holds a degree in accounting [transcripts provided] and was employed in the field for which she was trained [see employer letter].

LGY noted no other significant underwriting exceptions or risks and praised the lender for their attention to detail and thorough records.

Offsetting Short-Term Debts (6-24 months)

VA Pamphlet VAP26-7 Chapter 04 Credit Underwriting

Change Date: February 22, 2019

Topic 2: Income – Required Documentation and Analysis

(f) Borrower Employed for Less than 12 Months

Generally, employment less than 12 months is not considered stable and reliable. However, the lender may consider the employment stable and reliable if the facts and documentation warrant such a conclusion.

If the probability of continued employment is good, but not well supported, the lender may utilize the income if the borrower has been employed at 12 months, to partially offset debts of 6 to 24 months duration.

An explanation of why income was used to offset debts must be documented on the VA 26-6393, Loan Analysis.

(h) Income from Overtime Work, Part-Time Jobs, Second Jobs, and Bonuses

Generally, such income cannot be considered stable and reliable unless it has continued and is verified for 2 years.

The lender may use this income, if not eligible for inclusion in income, but verified for at least 12 months, to offset debts of 6 to 24 months duration.

An explanation of why the income was used to offset must be documented on VA Form 26-6393, Loan Analysis.

(k) Active Military Borrower’s Income

Verification and Analysis of Other Military Allowances

If the duration of the military allowance cannot be determined, this source of income may still be used to offset short term obligations of 6 to 24 months duration.

Image Courtesy of the American Land Title Association

BEHIND THE SCENES: Deed Fraud Is For Real

An online search on deed fraud yields varying assessments of its severity and likelihood. While the probability of you or someone within your network, such as a customer, falling victim to this crime remains relatively low, it is important to recognize that if such an event were to occur, it could have significant ramifications on one’s life.

The American Land Title Association is now underwriting added coverage for various forgery and deed fraud risks.

From the American Land Title Association

“With criminals harnessing advanced technology to perpetuate sophisticated seller impersonation schemes against unsuspecting homeowners, new products like the policy endorsements are needed to keep the American Dream of homeownership intact,” said ALTA’s CEO Chris Morton. “These endorsements set the standards for forgery protection before and after closing, and build upon ALTA’s landmark Homeowner’s Policy of Title Insurance.”

With deed fraud on the rise, prospective and current homeowners may want to ensure their property is protected for the long haul. Since 1998, the ALTA Homeowner’s Policy has offered these additional protections, and now the title industry is providing new endorsement options for future and existing homeowners.

Homeowners have two different options: The ALTA Homeowner’s Policy offers enhanced protections, including coverage for fraud or forgery that happens after you purchase the property; consumers also have the option of purchasing a policy endorsement to the Owner’s Policy, providing coverage specifically for future deed or mortgage forgery.

Current homeowners who have a basic Owner’s Policy can request the addition of post-policy

coverage for deed or mortgage forgery by reaching out to their title company.

New ALTA Endorsements (August 2025)

- ALTA 49 Endorsement – Forgery – New Owner’s Policy – Residential (New Endorsement)Purpose: The ALTA 49 Endorsement is designed to address the situation where the homeowner is purchasing an ALTA Owner’s Policy and would like post-policy coverage for deed or mortgage forgery, but where the ALTA Homeowner’s Policy is either not available, or is not offered to the homeowner.

- ALTA 49.1 Endorsement – Forgery – Existing Residential Owner’s Title Policy (New Endorsement)Purpose: The ALTA 49.1 Endorsement is designed to address the situation where the homeowner has previously purchased an ALTA Owner’s Policy and would like future coverage for deed or mortgage forgery.

Press Release U.S. Attorney’s Office, Eastern District of Virginia

Friday, January 30, 2026

ALEXANDRIA, Va. – Two former financial services specialists were sentenced for conspiracy to commit mail and wire fraud affecting financial institutions relating to their unlawful use of client information to obtain loans.

According to court documents, Roberta Leigh Dawson, aka Bird, 63, formerly of Alexandria and current resident of Norlina, North Carolina, was a licensed loan officer with a local mortgage brokerage, and Edward Fitzgerald, 59, of Fairfax, purported to be a financial advisor with an expertise in real estate transactions and investments. Fitzgerald’s clients provided him with access to their money, financial information, and means of identification.

Fitzgerald passed his clients’ information to Dawson to obtain fraudulent real estate loans. In some instances, Fitzgerald and Dawson sold their victims’ homes without their knowledge, including to straw buyers. They would then strip out the equity and use it to pay their own expenses, among other things. They also used their victims’ personal information without their knowledge to obtain loans in their names and submitted to financial institutions loan applications that were replete with misstatements.

Dawson withdrew hundreds of thousands of dollars of victim cash from accounts she controlled after fraudulently diverting the funds into those accounts. Dawson routinely paid Fitzgerald’s credit card, which he used for extravagant travel, luxury items, and daily expenses, with more than $1 million in funds obtained from the fraud scheme.

Dawson pled guilty on Sept. 24, 2025, and was sentenced today to two years and six months in prison. Fitzgerald pled guilty on Sept. 16, 2025, and was sentenced on Jan. 20 to five years in prison.

The FBI Washington Field Office investigated this case. Assistant U.S. Attorneys Russell L. Carlberg and Annie Zanobini and former Assistant U.S. Attorney Christopher J. Hood for the Eastern District of Virginia and Special Assistant U.S. Attorney Kimberly Pedersen, from Federal Housing Finance Agency, Office of Inspector General, prosecuted the case.

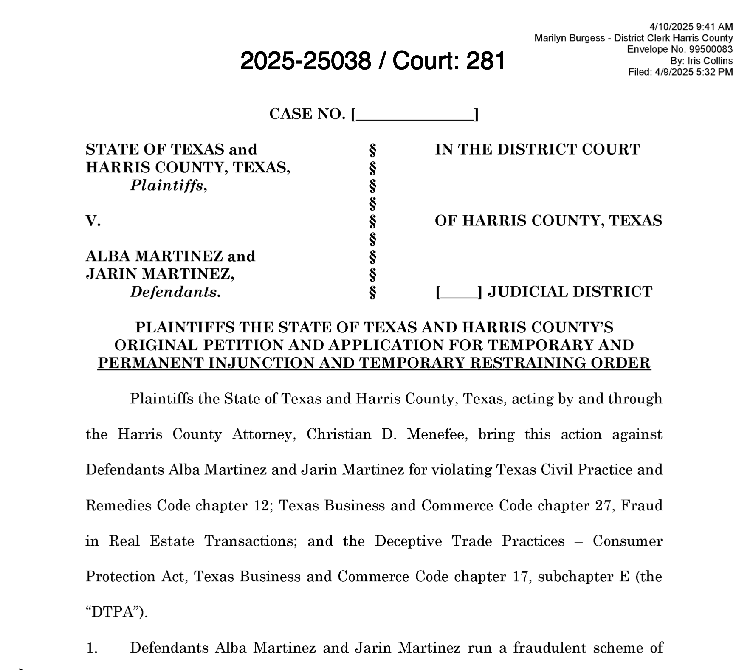

Houston, Texas, September 04, 2025

Harris County Attorney Christian D. Menefee Secures Judgment Returning 40 Properties in Forgery Scheme

[Christian Menefee is no longer the Harris County Attorney; he is the newest Representative sworn into the 119th United States Congress, 02/2026].

Harris County Attorney Christian D. Menefee announced that his office has secured a final default judgment against a Houston couple accused of forging legal documents to falsely claim ownership of dozens of properties across Harris County. The ruling returns 40 homes to their rightful owners, marking a major milestone in the fight against deed fraud and real estate forgery.

The judgment stems from a lawsuit filed in April 2025, which outlined the way the couple carried out a widespread forgery scheme impacting dozens of Houston-area properties. The scheme involved forging paperwork in order to transfer ownership into their names, victimizing homeowners and deceiving unsuspecting buyers out of hundreds of thousands of dollars.

“We are incredibly glad to see these properties being returned to their rightful owners. It’s a scenario that never should have happened, but I am glad that my office was able to advocate for these victims and fight for the best outcome,” said County Attorney Menefee. “When people work their whole lives to buy a home, they should never have to worry that someone will steal it on paper. This ruling restores what was taken and sends a message: we will not let people exploit our neighbors here in Harris County.”

The office launched Scam Free Harris County last fall to educate the public, fight scams, and create stronger protections for consumers. The initiative has already connected dozens of residents with resources and led to various investigations of consumer and deed fraud.

Tip of the Week – Have a Question About Operations, Sales, Marketing, or Compliance? Email Your Questions to the Loan Officer School Journal.

We invite LOSJ readers to submit questions on any topic to the editor. Topics can include compliance, sales, marketing, implementation, and other areas that may be helpful to our customers. If we use your question, we will include only your first name in our response. Please send your questions to: losjmailbag@gmail.com.

Necessary Mailbag Disclosure: The LOSJ is a periodic publication from LoanOfficerSchool.com designed to educate and inform our readers. Please note that we do not provide legal advice, and nothing in the LOSJ should be construed as a legal opinion on specific facts or circumstances. The content serves strictly for informational purposes. We strongly advise readers to consult legal counsel regarding any legal matters or specific questions.