Why Haven’t Loan Officers Been Told These Facts?

Property Tax Relief – Adding Value To Your Services

With home values skyrocketing, property taxes are also increasing at breakneck speed. Rising property taxes exacerbate housing insecurity for the most vulnerable people in our midst. Consequently, besides a terrific opportunity to serve your community, this problem presents an occasion for enterprising loan officers to strengthen and expand their network, provide additional financing solutions, and make a positive difference in the lives of many needy people.

Common and Obscure Forms of Property Tax Relief

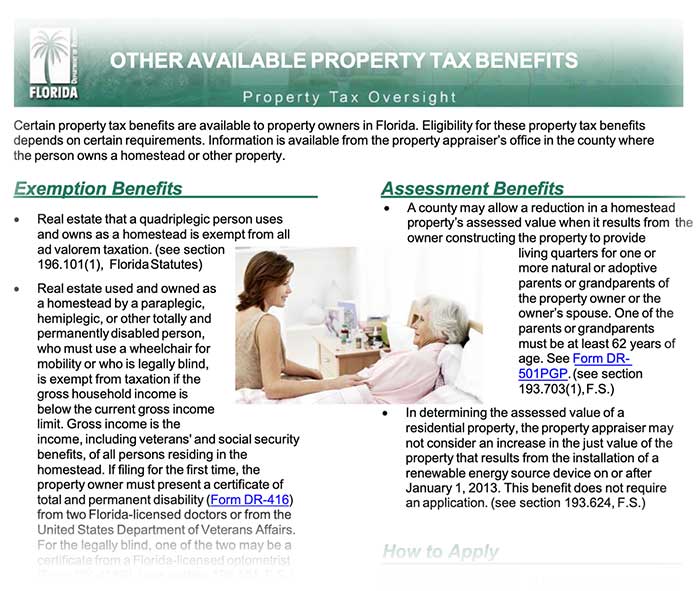

Some taxing authorities have robust forms of property tax relief, such as special homestead exemptions or similar help for active-duty military, veterans, low-income, and disabled homeowners. Abatements are common in almost all jurisdictions. However, there are obscure and, therefore, overlooked tax mitigations that can benefit many American households in need. For example, here are a few less-known Florida property tax abatements.

- Tax reductions for households adding an Alternative Dwelling Unit or similar special-use improvement to provide living space for elderly parents.

- Tax exemptions for permanently disabled low-income homeowners.

- Tax exemptions for the surviving spouse of first responders who died in the line of duty.

When Moving, Take Your Tax Assessment With You

Florida provides for homestead portability under the Save Our Homes (SOH) law. Florida residents moving from a previous Florida homestead to a new homestead may be able to transfer, or “port,” all or part of their homestead assessment difference. If eligible, portability allows most Florida homestead owners to transfer their SOH benefit from their old homestead to a new homestead, lowering the tax assessment and, consequently, the taxes for the new homestead.

To transfer the SOH benefit, homeowners must establish a homestead exemption for the new home within three years of January 1 of the year they abandoned the old homestead (not three years after the sale). Does this sound complicated? That’s why you have a CPA, attorney, and financial planner on your team.

Circuit Breakers

Around the country, numerous property tax abatements permit deferring or freezing real property tax obligations, a process known as a “circuit breaker.” Once the property tax exceeds a specified household income, it caps at a limited amount for that year.

Homeowners Are Leaving Money on the Table, The Kicker

Most of these programs have one thing in common—homeowners must apply for the relief. It is not automatic. Knowledge is power. Understandably, many folks are ignorant of these programs, especially the more obscure or recently available abatements. Therefore, far too many financially struggling households, those least able to neglect available tax mitigations, sometimes unnecessarily forgo essentials like medicine, food, and HVAC to make ends meet because of overly burdensome property taxes.

According to a recent article by The AARP Foundation, more than 9 million Americans qualify for property tax relief, but fewer than 8 percent of that number apply.

An Opportunity To Shine

Would you like like to help? Consider the possible networking opportunities. Why not create a website with your area’s tax abatement information and available property tax assistance? Are there a few cross-selling, listing, and mortgage opportunities here? Consider partnering with other subject matter experts, such as a real estate attorney, CPA, and broker. You may already be into podcasting or creating website content. What about a series, “Making your home more affordable” podcasts? A little loss mitigation, home maintenance, insurance tips, and a dash of property tax relief. Connect with your state Housing Finance Agency. Perhaps they may help promote the project.

As mentioned, property tax relief is not just for disabled or older Americans—to recap, here are a few types of persons who may qualify for significant property tax savings.

- Veterans.

- Surviving spouse of a veteran.

- Low or moderate-income households.

- Disabled household member.

- Households with elderly persons.

Remember that in some cases, the qualifying individual does not need to be the homeowner. For example, Mary is a partner in a law firm. She owns her home and does not qualify for special abatements. But last April, Mary’s elderly, disabled mother moves in with her. They now share Mary’s house. Accordingly, Mary has significantly improved the home to accommodate her mother’s needs.

Hey, guess what? Rich and middle-class people enjoy paying lower property taxes, too. Now, the property is occupied by a disabled and elderly resident, qualifying Mary for special property tax abatements.

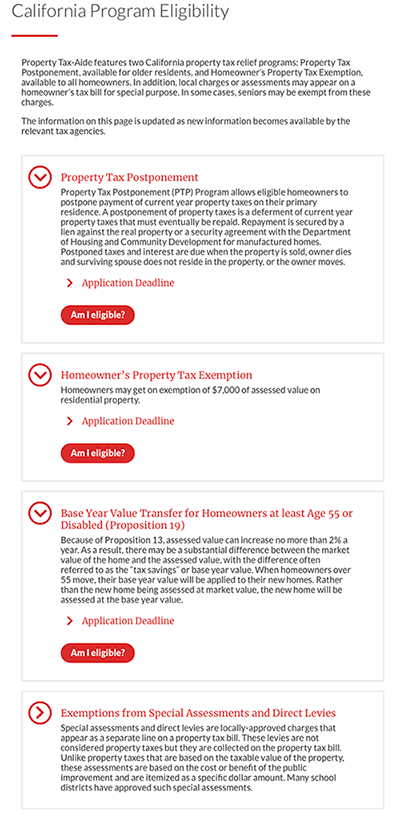

Another consideration is the AARP Foundation Property Tax Aide. The LOSJ has not vetted the AARP service. You might want to try it and see what it’s all about before referring your customers. The AARP Foundation Property Tax-Aide program offers to research available property tax abatements for homeowners and renters. Yes, renters are often eligible, too.

Check with local your local tax pro. See what is possible in your area.

Do you have a great value proposition you’d like to get in front of thousands of loan officers? Are you looking for talent?

BEHIND THE SCENES – CFPB Targets Mortgage Closing Costs

Junk fees are driving up housing costs. The CFPB wants to hear from consumers.

Have you noticed that when the Bureau gets into a scrape with the big banks or suffers a few setbacks, it comes gunning for the 98-pound weakling on the block? Mortgage bankers must have the worst lobbyists on the planet.

According to the CFPB, the price of eggs, chicken wings, and everything else can rise, but not mortgages or closing costs. Once again, the CFPB has the knives out for the mortgage industry.

From the CFPB [Paraphrased, “Time for a win. Let’s kick the hell out of the mortgage industry.”]

March 8, 2024

Families who manage to save up for a down payment and get approved for a mortgage often get an unwelcome surprise: closing costs that all too often are full of junk fees. Closing costs are the fees you pay on the day you finalize the purchase of your home, and they include things like title insurance, credit report and appraisal fees, origination fees, and more. The Consumer Financial Protection Bureau (CFPB) is working to ensure that consumers can navigate the closing process more easily, shop around, and save money.

In the coming months, the CFPB will continue working to analyze mortgage closing costs, seek public input and, as necessary, issue rules and guidance to improve competition, choice, and affordability. We will also continue using our supervision and enforcement tools to make it safer for people to purchase homes and to hold companies accountable when they violate the law. Our research findings and market insights guide our work, as well as information from consumers that helps us better understand how issues like mortgage closing costs affect households and families.

Closing costs have risen, putting pressure on borrowers’ budgets

While home prices and interest rates often command our attention, closing costs also contribute to borrowers’ monthly burdens. One measure of closing costs is total loan costs. Total loan costs include origination fees, appraisal and credit report fees, title insurance, discount points, and other fees. From 2021 to 2022, median total loan costs rose sharply, increasing by 21.8 percent on home purchase loans [Duh! Generally, in large part, the closing costs are directly tied to house prices and loan size. That would be your Uncle Jerome’s hand, not the mortgage industry].

In 2022, the median amount paid by borrowers was nearly $6,000 in these costs and fees. That’s a substantial upfront cost on what is already a major financial undertaking. Homeowners can choose to pay closing costs out of pocket, but that can reduce their down payment amount. Lenders sometimes give borrowers a “credit” to cover closing costs, but then charge the borrower a higher interest rate on the mortgage [Hey kids, don’t try this at home! Notice the CFPB’s negative slant in describing pricing or financing options]. Sometimes sellers pay closing costs but increase the sale price on the home. Often, closing costs are simply rolled into the total loan amount, racking up interest for the life of the loan. Borrowers who can’t bring cash to the table often have to pay more through higher interest rates or mortgage insurance payments.

Many of these costs are fixed and do not fluctuate with interest rates or change based on the size of the loan. As a result, they have an outsized impact on borrowers with smaller mortgages, such as lower income borrowers, first-time homebuyers, and borrowers living in Black and Hispanic communities. A 2021 study found that nearly 15 percent of lower income homebuyers had closing costs that exceeded the amount of their down payment.

We are paying particular attention to the recent rise in discount points. A higher percentage of borrowers reported paying discount points in 2022 than any other years since this data point was first reported in 2018 [The rise in discounts is due to the capital market’s apprehension surrounding the Federal Government’s monetary policies. No one wants to get caught with a ton of prepaid loans when rates drop]. In 2022 about 50.2 percent of home purchase borrowers paid some discount points, up from 32.1 in 2021. Borrowers are also paying more in discount points. The median discount points paid for home purchase loans in 2022 was $2,370 in 2022, up from $1,225 in 2021. Lenders sell discount points to borrowers to reduce interest rates. These points may not always save borrowers money, however, and may indeed add to borrowers’ costs. The CFPB is continuing to monitor market trends in this area.

Lack of competition and choice may add to already rising housing costs

It appears that some closing costs are high and increasing because there is little competition. Borrowers are required to pay for many of the costs associated with closing a home loan but cannot pick the provider and do not benefit from the service. In many cases, the lender simply picks from a very small universe of providers, and the costs are then passed on to the borrower.

Lender’s title insurance is one example of a fee borrowers face at closing where the borrower has no control over cost. Title insurance is meant to protect against someone else laying claim to a borrower’s property. A lender’s title insurance policy protects only the lender against these possible claims, not the borrower. Instead of paying this fee themselves, lenders make borrowers pay the cost. The amount that borrowers pay for lender’s title insurance is often much greater than the risk.

Fees for credit reports are another example. The credit reporting industry is highly concentrated, with just a handful of dominant players dictating the price of credit reports and scores. Borrowers pay the fee for lenders to pull credit reports for each loan applicant from three nationwide credit reporting companies. Mortgage lenders have recently reported steep increases in the price of the scores and reports used for mortgage underwriting. The CFPB has heard reports of recent costs spiking 25 percent to as much as 400 percent. At the same time, we estimate that nationwide credit reporting companies made over $1.3 billion annually. These steep increases in a market that lacks competition and choice warrant further scrutiny.

$8 maximum late fee for mortgages? What next.

See the announcement here: CFPB Blog: Junk fees are driving up housing costs

Tip of the Week – Help Your Referral Partners With Their Business

See our lead article about real property tax abatements and consider how this information might be useful for professionals such as real estate brokers, CPAs, insurance agents, and financial planners. What else can you do to help your referral partners grow their business and improve their value propositions?

Are you putting the cart before the horse? To grow your business, first, consider how to help referral prospects grow their business and overcome their challenges.

Business analysis is the art of understanding your customers’ objectives and articulating those objectives to facilitate the means to help them attain or inch closer to their goals.

Often, business analysis seeks to comprehend and overcome obstacles to the customer’s goals. However, for many customers, setting more strategic goals is a necessary first step in making positive changes.

In the past, the LOSJ has written about effective strategic goal-setting. See the V2 I51 issue below.

Help your referral partners powerfully envision and reach their goals.