Why Haven’t Loan Officers Been Told These Facts?

AUG 17, 2023 CFPB Press Release

CFPB Penalizes Freedom Mortgage and Realty Connect for Illegal Kickbacks

Lender provided incentives to Realty Connect and other brokerages in exchange for mortgage referrals

WASHINGTON, D.C. – Today, the Consumer Financial Protection Bureau (CFPB) took action against Freedom Mortgage Corporation (Freedom) for providing illegal incentives to real estate brokers and agents in exchange for mortgage loan referrals. Freedom provided real estate agents and brokers with numerous incentives — including cash payments, paid subscription services, and catered parties — with the understanding they would refer prospective homebuyers to Freedom for mortgage loans. This conduct violated the Real Estate Settlement Procedures Act and its implementing regulation. The CFPB is ordering Freedom to cease its illegal activities and pay $1.75 million into the CFPB’s victim relief fund. The CFPB separately issued an order against a real estate brokerage firm, Realty Connect USA Long Island (Realty Connect), for accepting numerous illegal kickbacks from Freedom. Realty Connect will pay a $200,000 penalty and cease its unlawful conduct.

“Freedom provided kickbacks to real estate brokers and agents — including those at Realty Connect — in return for mortgage referrals, a clear violation of federal law,” said CFPB Director Rohit Chopra. “The CFPB will be vigilant in rooting out anti-competitive behavior that interferes with consumers’ ability to choose financial products and services.”

Freedom is a privately held nonbank mortgage loan originator and servicer headquartered in Boca Raton, Florida. In August 2021, Freedom transferred its traditional retail mortgage unit to its wholly owned subsidiary, RoundPoint Mortgage Servicing (RoundPoint). Freedom’s RoundPoint subsidiary ceased traditional retail operations on or around August 2022. Realty Connect is a privately held real estate brokerage firm based in Suffolk County, New York.

The Real Estate Settlement Procedures Act helps reduce closing costs for homebuyers and increases competition in the marketplace by prohibiting mortgage loan originators from offering referral incentives and kickbacks to other companies in exchange for referring homebuyers.

The CFPB found Freedom and Realty Connect violated the Real Estate Settlement Procedures Act. The specific violations include:

-

- Paying for referrals through illegal marketing service arrangements: Freedom entered into marketing services agreements with over 40 real estate brokerages where Freedom made monthly payments totaling approximately $90,000 to brokerages in exchange for the brokerages’ marketing services. However, Freedom used these marketing services agreements as a way to pay for mortgage referrals, rather than compensate the brokerages for marketing services they actually performed. Realty Connect received $6,000 per month from Freedom, but failed to perform many of the marketing tasks required under the agreement.

- Offering premium subscription services free of charge: Freedom gave real estate brokers and agents free access to valuable industry subscription services, which provided information concerning property reports, comparable sales, and foreclosure data. Freedom paid thousands of dollars per month for one of the subscription services, and Freedom provided access to over 2,000 agents for no cost. Freedom often required real estate agents and brokers to agree to be paired with a Freedom loan officer before Freedom would give them access to its subscription services. Since 2017, the real estate agents who received free access to these subscription services—including agents at both Realty Connect and other brokerages—made more than 1,000 mortgage referrals to Freedom.

- Hosting and subsidizing company events and providing gifts: Freedom hosted parties and other events for real estate agents and brokers, including events held exclusively for Realty Connect brokers and agents. Freedom paid for the food, beverages, alcohol, and entertainment. Freedom would also sometimes give free tickets to sporting events, charity galas, or other events where the agents and brokers would have otherwise needed to pay their own way. Freedom also denied requests for event sponsorship from real estate brokerages that did not refer mortgage business to Freedom’s loan officers.

Enforcement Action

Under the Consumer Financial Protection Act (CFPA), the CFPB has the authority to take action against institutions violating consumer financial laws, including engaging in unfair, deceptive, or abusive acts or practices. The CFPB found that Freedom and Realty Connect violated the Real Estate Settlement Procedures Act by exchanging items of value in return for mortgage loan referrals.

The orders announced today require Freedom and Realty Connect to:

-

- Cease illegal activities: Freedom is prohibited from providing anything of value to other entities in exchange for mortgage referrals. Realty Connect is prohibited from accepting items of value in exchange for mortgage referrals.

- Pay nearly $2 million in penalties: Freedom will pay a $1.75 million penalty into the CFPB victims relief fund. Realty Connect will also pay a $200,000 civil money penalty.

Section 8 Challenges

Section 8 compliance can be a daunting compliance challenge. Not only must the lender guard against outright violations, but lenders must avoid the appearance of a violation.

Unlike many compliance challenges, Section 8 issues revolve primarily around external stakeholders and internal team members. Consequently, compliance controls for implementing marketing services agreements, gift-giving, and promotions represent a unique challenge.

The counterparty to any MSA can get you into trouble without you doing anything wrong. MSAs can be informal (pattern, practice, or loose oral agreement) or formal (written, the elements of a contract exist) agreements and practices. When receiving referrals, you could be a counterparty to a violation even if the referred consumer has not talked to you. The correct disclosure implementation is an absolute first line of defense with any MSA – formal or otherwise.

Gifts and promotions are another challenge. If any gift giving to persons represents a pattern or nexus of gifts or promotions to referrals – you may have a Section 8 issue.

See several LOSJ articles on the CFPB’s revised Section 8 guidance:

LOSJ Volume 1 Issue 8

LOSJ Volume 1 Issue 9

LOSJ Volume 1 Issue 10

LOSJ Volume 2 Issue 16

LOSJ Volume 2 Issue 17

Do you have a great value proposition you’d like to get in front of thousands of loan officers? Are you looking for talent?

BEHIND THE SCENES –

Fair Lending Dispute Heating Up

The Federal Trade Commission Weighs in on CFPB Fair Lending Defeat

Townstone Attorneys Respond to CFPB Regulation B Appeal

In February, the Journal wrote about a potential watershed event for Fair Lending. Should the recent lower federal court dismissal stand, the Equal Credit Opportunity Act precept against “discouragement” would be severed from Regulation B. The CFPB lost the case because the court differed with the CFPB’s interpretation of its organic authority to build on the intent of the ECOA. The case was the first and only instance of the CFPB suing a mortgage broker for an ECOA violation in the agency’s short history.

Regulation B 12 CFR 1002.4 General rules

“(b) Discouragement. A creditor shall not make any oral or written statement, in advertising or otherwise, to applicants or prospective applicants that would discourage on a prohibited basis a reasonable person from making or pursuing an application.”

“Comment 1. Prospective applicants. Generally, the regulation’s protections apply only to persons who have requested or received an extension of credit. In keeping with the purpose of the Act – to promote the availability of credit on a nondiscriminatory basis – § 1002.4(b) covers acts or practices directed at prospective applicants that could discourage a reasonable person, on a prohibited basis, from applying for credit.”

The case stemmed from CFPB’s allegations about the brokers’ alleged use of racially offensive language on its regular radio mortgage program. The CFPB’s complaint alleged an ECOA violation on the basis of discouragement. The CFPB argued that allegedly racially inappropriate comments would discourage African-American prospects from applying to the broker for a mortgage.

Federal judge Valderrama disagreed with the CFPB’s regulatory interpretation of the ECOA and granted the defendant’s motion for dismissal. The court stated that “the plain text of the ECOA thus clearly and unambiguously prohibits discrimination against applicants, which the ECOA clearly and unambiguously defines as a person who applies to a creditor for credit. . . The Court therefore finds that Congress has directly and unambiguously spoken on the issue at hand and only prohibits discrimination against applicants.”

In April, the CFPB filed a 47-page appeal with the 7th Circuit in May to overturn the lower court ruling that ECOA only applies to applicants.

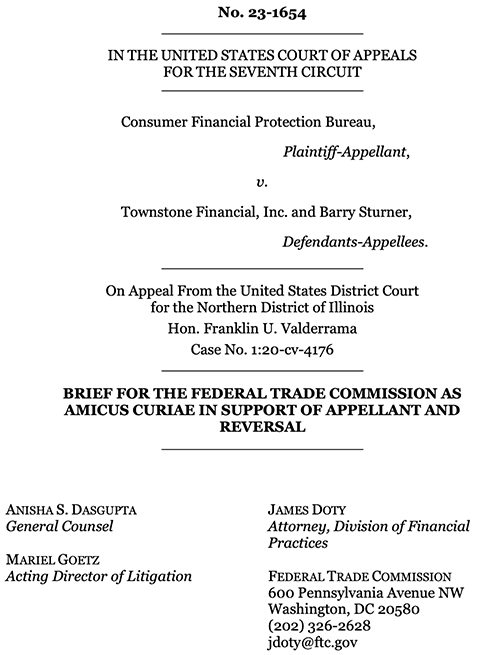

Other stakeholders, including the Federal Trade Commission, are behind the CFPB. In June, the FTC delivered a friend of the court brief supporting the CFPB position.

From the FTC Press Release

“In its brief, the FTC argues that the district court’s ruling was incorrect. The Commission’s brief notes that the anti-discouragement rule—which has stood for nearly 50 years—is authorized by the plain language of ECOA, which mandates that regulators further ECOA’s “purpose” and prevent its “evasion.”

The FTC also argues that the district court’s ruling would have “profoundly negative consequences” for consumers, emboldening discriminatory lenders to openly discourage consumers from applying for loans. For example, the brief points to the possibility that a lender could display a “Whites Only” sign or turn away Black consumers as they walk in the door. The brief notes that the FTC receives thousands of complaints from consumers each year related to discriminatory lending practices.”

In addition to the FTC’s amicus brief, the court has received another amicus brief from attorneys representing a coalition of housing and fair lending proponents supporting the CFPB position.

As the FTC states, the lower court’s decision upends a decades-long interpretation of the ECOA. It’s complicated. Significant issues are at stake, such as the organic authority of administrators to implement the statutes. The CFPB would seem to have such authority under the Consumer Financial Protection Act. However, case law favors a plain text reading of the statute when the Congressional intent is clear. Like many statutes, Congress intends for the regulators to connect the dots here and there.

On August 14, Townstone attorneys made their case to the appeals court. Arguing in essence:

- The anti-discouragement rule is not a permissible construction of ECOA. – Meaning that the CFPB exceeded its authority by misinterpreting core elements of the statute.

- The anti-discouragement rule raises serious constitutional problems. – The CFPB is censoring speech without the authority to do so and violating the Constitution’s First Amendment.

First Amendment

Congress shall make no law respecting an establishment of religion, or prohibiting the free exercise thereof; or abridging the freedom of speech, or of the press; or the right of the people peaceably to assemble, and to petition the Government for a redress of grievances.

The 53-page Townstone brief has much more to say. See the links below. Understand that the defendant’s counsel arguing the First Amendment defense in no way indicates an intent or desire on the part of the defendant to participate in discriminatory oratory, advertising, or conduct. The defendant has vigorously denied the accusations of discriminatory conduct.

See the Townstone brief here: Townstone Brief

See the CFPB brief here: CFPB Brief

See the LOSJ Article here: LOSJ Article

Stay tuned.

Tip of the Week – Know Your Qualifying Payments

For Agency ARMs

Hybrid Government ARMs

- Except for the 1 Year ARM, all FHA and VA hybrid ARMs allow the lender to qualify the borrower using the initial interest rate.

One-Year Government ARMs

- For VA loans, the lender must calculate the qualifying payment for ARMs that adjust after one year at one percentage point above the initial rate.

- For FHA loans, if the Loan-to-Value (LTV) is 95 percent or more, the lender must underwrite the mortgage based on payments calculated using the initial interest rate plus one percent.

- For FHA loans, if the mortgage is less than 95 percent LTV, the lender must underwrite the mortgage based on payments calculated using the initial interest rate.

Conforming ARMs

- FHLMC 3/6mo ARMs require the lender to calculate the qualifying payments at the lifetime rate limit.

- FHLMC 5/6mo ARMs require the lender to calculate the qualifying payments at two percent over the note rate (introductory rate).

- FHLMC 7/6mo and 10/6mo require the lender to calculate the qualifying payment at the greater of the note rate or fully-indexed rate.

- FNMA ARMs with introductory periods of three years or less require the lender to qualify the applicant using the maximum interest rate that could apply during the first five years after the first payment is due.

- FNMA 5/6mo ARMs require the lender to qualify the applicant using the maximum interest rate that could apply during the first five years after the first payment is due (note rate plus first rate change cap of 1%) or the fully indexed rate.

- FNMA 7/6mo and 10/6mo require the lender to calculate the qualifying payment at the note rate.